The Aptos ecosystem is having a moment. It’s posting real traction where it matters for finance: this year’s fastest-growing stablecoin base, DeFi TVL up ~2.5x to $1B since last year, and between April–June 2025, DEX volumes climbed 4x, to ~$200M. That’s not “ just another Move chain” story; that’s a market signaling it wants trading-grade rails.

Why the shift? Aptos has been recasting itself as a “Global Trading Engine,” a stack that rethinks everything from consensus to application features so intent turns into settlement with minimal friction. The aim is simple: make on-chain finance feel instant, cheap, and reliable enough for everyday use.

Aptos's Ongoing Rebranding | Image via X

Aptos's Ongoing Rebranding | Image via XRipple, for its part, has re-entered the spotlight after resolving its legal overhang, doubling down on payments, stablecoins, and real-world assets. As of August 2025, major managers made at least 10 spot XRP ETF filings, underscoring renewed institutional interest.

Both networks are pushing finance-first narratives from different angles. Aptos toward a consumer trading and payments OS, and Ripple as the long-standing institutional rails. This piece compares their directions. The goal is to understand how these strategies could deepen the connection between on-chain infrastructure and global finance.

TL;DR — Comparing Aptos and Ripple

- Aptos and Ripple are converging on finance from opposite ends: Aptos is positioning itself as a high-performance trading engine for consumer finance, while Ripple remains the institutional standard for global payments and settlement.

- Aptos emphasizes speed and trading UX with sub-second finality, 11k+ TPS, and features like re-orderable transactions, scheduled triggers, and X-Chain Accounts for seamless onboarding.

- Ripple optimizes for predictable, low-cost payments with 3–5s ledger closes, negligible fees, and corridor liquidity, now extended with an EVM sidechain and the RLUSD stablecoin.

- Institutionally, Ripple dominates with ~$1.3T ODL flows in Q2 2025 and multiple spot XRP ETF filings, while Aptos is gaining traction through tokenized funds, custody integration, and exchange-listed ETPs.

- Tokenomics differ: APT uses adaptive issuance and lower staking rewards to drive DeFi participation, whereas XRP relies on its fixed supply, escrow releases, and demand from payment rails and ETFs.

- Bottom line: Ripple modernizes bank-grade payment rails, Aptos builds consumer-grade trading rails. Together, they show how on-chain infrastructure is bridging into global finance from different directions.

👉 Ripple is the benchmark for institutional payments; Aptos is emerging as the most credible trading-first consumer finance chain in 2025.

Shared Origins, Different Arcs

Ripple and Aptos start from the same place: use blockchains to move value more broadly and cheaply. Ripple did it by wiring banks and remittance corridors together; Aptos did it by pushing speed, safety, and predictable execution so that everyday transactions can clear fast on a general-purpose chain.

Ripple’s origins and early focus

Ripple traces back to RipplePay (2004), then to the XRPL effort in 2011 and a Ripple Labs rebrand in 2012. The XRPL launched in 2012 as an open-source payments ledger with a pre-mined XRP supply, designed to avoid Proof-of-Work while keeping fees minimal. Ripple’s first major push was bridging banks to blockchain for cross-border settlements: think Santander in 2015, followed by RippleNet in 2016, a liquidity service designed to beat the limitations of SWIFT.

Santander was the First Bank to Implement Ripple's Payment System | Image via Cointelegraph

Santander was the First Bank to Implement Ripple's Payment System | Image via CointelegraphAptos’s origins and core technology

Aptos emerged from Meta’s Diem/Novi work and launched its mainnet in October 2022, carrying forward a design bias for safety and throughput. Its core stack is purpose-built for finance:

- AptosBFT v4 (consensus): a modern BFT protocol that finalizes quickly and keeps the network responsive under stress.

- Quorum Store (mempool): batches and disseminates transactions efficiently so blocks stay full without clogging the network.

- Block-STM (execution): a parallel execution engine that runs many independent transactions at once: think fewer bottlenecks and faster clears.

- Move / Aptos Move (language): resource-oriented programming that encodes asset safety rules directly in code, reducing common foot-guns in financial apps.

- Pipeline upgrades (Raptr, Zaptos, Tiered Storage, Execution Pool): Overhaul how consensus, execution, and storage interact, reducing user-perceived latency while maintaining stable performance at high loads.

Both target value transfer but from different directions. Ripple built bank-grade rails and corridor liquidity; Aptos is assembling a trading-grade consumer economy where payments, swaps, and savings can be instantaneous and inexpensive at scale.

Aptos vs. Ripple: Core Infra & Performance

TL;DR: Ripple builds payment rails: predictable settlement, minimal fees, and pragmatic programmability. Aptos builds a trading engine: deterministic order handling, cross-chain onboarding, and latency work that makes on-chain markets feel CEX-grade.

Ripple: Payments-First Ledger Built for Settlement

Ripple’s XRPL optimizes the basics that banks and PSPs (payment service providers) care about: finality, cost, and reliability.

- Consensus & performance. XRPL uses a federated BFT consensus approach (often called RPCA). Ledgers typically close in ~3–5 seconds, fast enough for remittances and treasury movements but intentionally not built for high-frequency trading. Throughput targets are ~1,500 TPS on commodity hardware. In practice, international payouts are batched quickly and predictably without waiting minutes.

- Minimal, predictable fees. Minimum network fee is 0.00001 XRP, dynamically scaled under load, so retail transfers often cost fractions of a cent, and spam is discouraged. For users, this means you can move $50 or $50,000 and barely notice the network fee.

- Lightweight by design. XRPL keeps core logic lean:

- Code extended with Hooks (small WebAssembly snippets) for account-level rules like escrow checks.

- XLS-20 standard for NFTs

- Native AMM (XLS-30) alongside the long-standing order-book DEX, useful for corridor liquidity and FX-like swaps. Practically, a remittance app can auto-route via order book or AMM without shipping a whole EVM stack.

- EVM sidechain (2025). For heavy DApp logic, XRPL now features an EVM sidechain on the mainnet, allowing teams to deploy Solidity contracts while bridging value back to the base ledger. For users, this unlocks familiar EVM UX (MetaMask, Hardhat) with XRP settlement on-ramps.

Ripple Built an EVM-compatible Sidechain | Image via X

Ripple Built an EVM-compatible Sidechain | Image via XUser takeaway: Ripple’s “rails” give you bank-grade settlement, fast closes, negligible fees, and just-enough programmability for payments, with a path to richer logic via the EVM sidechain. It’s the SWIFT/ACH upgrade path on a public chain.

Aptos: Exchange-Grade Trading Baked Into L1

Aptos treats trading as a top priority, improving sequencing, triggers, and onboarding, and then backs it with in-depth pipeline work, ensuring the UX doesn’t crumble under load.

- Order handling you can trust: Reordered transactions let protocols guarantee critical ops (e.g., cancel_order before place_order) so makers can quote tighter spreads without fearing stuck cancels. Scheduled transactions enable time/price-conditioned actions, think stop-losses or TWAPs, without frantic manual signing. Net effect: on-chain CLOBs feel more like pro venues.

- Frictionless capital inflow: X-Chain Accounts let you trade on Aptos using a non-Aptos wallet (e.g., Phantom). Behind the scenes: Derived Account Abstraction + Circle CCTP + session keys. For a user, it’s “connect wallet → approve once → trade,” skipping new-wallet setup, bridges, and repeated signatures.

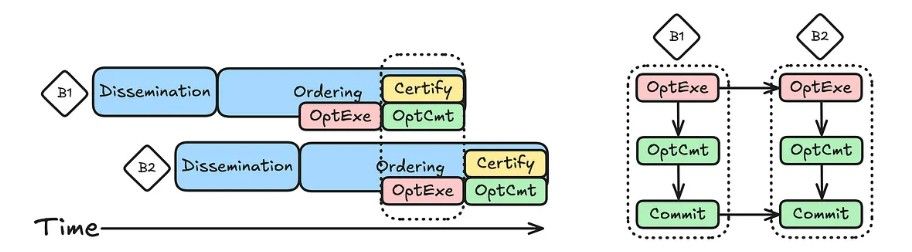

- Latency, not just throughput: Raptr targets ultra-low-latency consensus with resilience under stress; Zaptos overlaps consensus, execution, and storage to shave ~160–500ms off end-to-end latency and sustain sub-second UX at ~20k TPS in mainnet-like tests. Translation: when markets move, your orders still land on time.

- Scale without cliff-edges: Execution Pool, Block-STM v2, and Tiered Storage keep parallelism high and performance predictable even under load, so perps/spot venues don’t stall during volatility spikes. For traders, books stay responsive; for market makers, inventory bots don’t desync.

- Safer, automated UX:

- Account Abstraction enables custom auth (multi-sig, time-locks, session keys)

- Permissioned Signer adds condition-based auto-signing (e.g., rebalance only within risk limits)

- Stateless Accounts make cheap per-app sub-accounts for isolated positions and mass onboarding. You get CEX-like convenience with on-chain control.

An Illustration Explaining Zaptos Pipelining Capability | Image via Medium

An Illustration Explaining Zaptos Pipelining Capability | Image via MediumUnder the hood, Aptos already reports ~650ms user latency, sub-cent fees, and 11k+ TPS sustained, numbers that matter when every millisecond can change a fill.

| Metric | Aptos | Ripple / XRPL |

|---|---|---|

| Consensus | BFT-based (AptosBFT pipeline with latency-optimized upgrades incl. Zaptos/Raptr) | RPCA (federated BFT via validator UNLs) |

| Typical block time | < 130 ms | N/A (XRPL closes entire ledgers rather than producing frequent sub-second blocks) |

| Finality / ledger close | ~650 ms user latency (instant finality even at high load in reported tests) | ~3–5 seconds per validated ledger |

| Throughput (reported) | 11,000+ TPS with instant finality; Zaptos demos ~20,000 TPS with sub-second latency | Up to ~1,500 TPS on commodity hardware |

| Typical fees | < $0.0001 per tx (under one-hundredth of a cent) | 0.00001 XRP (10 drops) minimum base fee (scales under load) |

| Notable perf. notes | Zaptos reduces end-to-end latency by ~160–500 ms vs. baseline, keeps sub-second UX at load | 10+ years in production with predictable 3–5s ledger closes and trivial fees |

Bottom line:

- Aptos aims for on-chain trading to be equivalent (and potentially superior) to NASDAQ/LSE-style venues, featuring fair sequencing, triggerable orders, and instant feedback loops.

- Ripple aims for on-chain payments to be equivalent (and potentially superior) to bank transfers/SWIFT, global settlement rails with negligible friction.

In short, Ripple standardizes how money settles; Aptos standardizes how markets trade.

Institutional Rails: Ripple’s Home Turf vs Aptos’ Inroads

Ripple remains the category leader for institutional payments. The bank corridors, compliance surface, and recent M&A and ETF momentum reinforce this positioning. Aptos’ institutional pitch is newer but real: tokenized funds, qualified custody, and exchange-listed APT exposure, plus capital programs to deepen liquidity. It’s not a like-for-like competitor to Ripple’s corridors; it’s an emerging institutional on-ramp for a trading-centric consumer finance stack.

Ripple: Institutional Payments Stack

Ripple’s pitch to banks and payment firms remains unchanged: predictable settlement, negligible fees, and compliance-grade tooling, but now with a broader surface area for tokenization and DeFi.

- Rails vs. SWIFT: Ripple’s ODL model eliminates the need for pre-funded nostro accounts by sourcing liquidity in XRP at the time of sending, thereby tightening working-capital loops for PSPs and banks. In plain terms: fewer idle balances, faster closes.

- Security & compliance: Ripple highlights third-party certifications and attestations, positioning RippleNet as “secure by design” for financial institutions.

- Programmability for finance: XRPL added an EVM sidechain on June 30, 2025 to run Ethereum-style apps while settling through XRP rails—useful for regulated DeFi, tokenization, and bespoke treasury logic.

- Stablecoin & banking ops: Ripple launched the RLUSD stablecoin, with BNY Mellon as the primary reserve custodian and transaction-banking partner, providing credibility points for treasurers evaluating on-chain settlement.

- M&A to deepen liquidity: The announced acquisition of Hidden Road (prime brokerage, multi-asset credit network) extends institutional connectivity; the Rail deal targets stablecoin payments that plug into ACH/Fedwire/SWIFT. Both moves broaden Ripple’s stack from messaging and payout to liquidity, clearing, and credit.

- Market structure tailwinds: After the legal resolution, a cluster of spot-XRP ETF filings was amended by seven issuers, with decisions queued for late October—an institutional signal that complements Ripple’s bank-facing products.

What it means for institutions: cheaper cross-border payouts without parking idle cash, clearer audit/compliance posture, and optionality to build on-chain finance on the EVM sidechain while settling through XRPL’s low-latency ledger.

Aptos: Credible Inroads with Tokenized Assets & Listed ETPs

Aptos isn’t competing with Ripple’s bank corridors today, but it’s earning institutional mindshare where capital actually sits: tokenized funds, custody, and exchange-listed products.

- Tokenized fund pipes:

- BlackRock’s BUIDL expanded to Aptos in late 2024

- Franklin Templeton has added Aptos support for its on-chain money-market fund, which is a marquee RWA issuer bringing regulated assets onto the network.

- Exchange-listed exposure: Bitwise launched an Aptos Staking ETP, offering regulated access and turning staking yield into a wrapper institutions can hold.

- Custody & infrastructure: Anchorage Digital extended custody to Aptos-native RWAs, including BUIDL and USDY, providing institutions with a qualified custodian path for on-chain treasuries. Anchorage

- Ecosystem capital & grants: Aptos highlights a growing base of stablecoins/RWAs and a $200M foundation program to seed DeFi/RWA primitives, which is useful for issuers, market-makers, and wallet partners piloting retail-grade finance.

What it means for institutions: a performant L1 where tokenized cash and treasuries can live, with regulated wrappers (ETPs) and custody rails already in place, and a roadmap geared toward trading-native UX that can service consumer finance at scale.

Aptos & Ripple: Ecosystem Stats

Aptos shows broader DeFi depth (TVL, DEX volumes, stablecoin base) and consumer-app composability on ultra-low-latency rails, while Ripple leads institutional payouts and corridors, with growing but early programmable finance via its AMM and EVM sidechain: two strong ecosystems, each compounding in its lane.

Aptos ecosystem (via Messari)

- Liquidity & usage:

- Aptos’ stablecoin base expanded ~86% in H1 2025, from $648.9M → $1.2B, led by native USDT, USDC and USDe. DeFi TVL held ~$1B through H1 (up ~88% in APT terms)

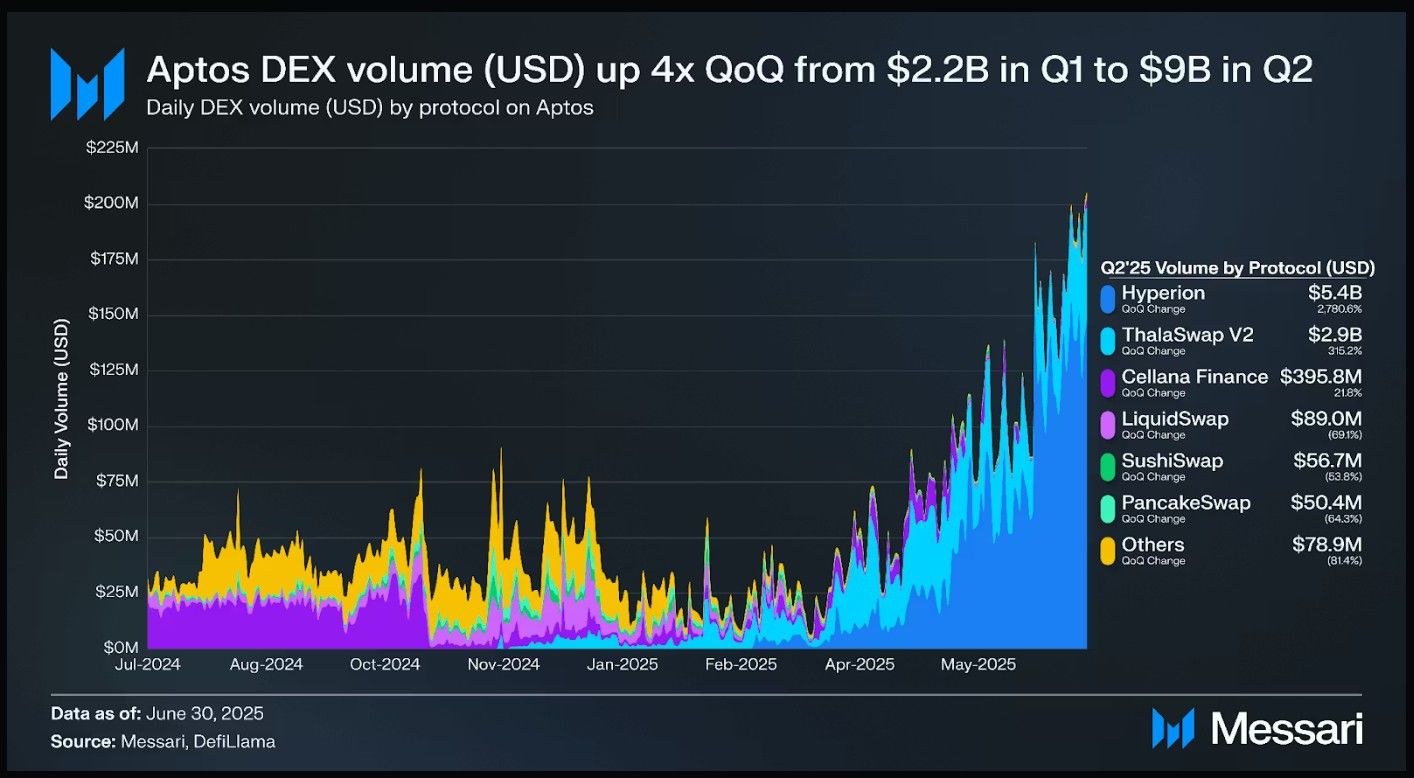

- DEX activity accelerated: Q2 volume hit $9.0B (+310% QoQ) and June alone reached $4.4B. Two venues drove the jump: Hyperion (29× QoQ to $5.4B) and ThalaSwap V2 (4× to $2.9B).

- Where capital sits:

- Aries Markets $288M

- Echo Protocol $285M (BTC-backed liquidity)

- Echelon $131M

- Hyperion $126M

- Thala Labs $96M.

- Amnis Finance leads liquid staking with ~59% share (34.4M APT).

- RWAs & market structure: RWA market cap closed Q2 at $537.4M, third after Ethereum and zkSync Era. The network also cleared the path for blue-chip money markets: Aave V3 won approval (June 27) for its first non-EVM deployment on Aptos.

- Adoption signals: Monthly active users stayed above 10M throughout H1 2025 (up from ~2.5M in mid-2024). Q2 averaged ~3.2M daily transactions and ~905k active addresses.

- Security & participation: ~878M APT staked (≈76% of eligible supply) placed Aptos 9th by staked market cap; 152 active validators and a Nakamoto coefficient of 18 round out the set.

Aptos DeFi Volume Jumped Dramatically in Q3 2025 | Image via Messari

Aptos DeFi Volume Jumped Dramatically in Q3 2025 | Image via MessariBottom line: Liquidity is deepening, volumes are scaling, and RWAs are taking root. Aptos appears well-positioned for consumer-grade finance to compound from here.

Ripple Ecosystem

- Payments & adoption: With regulatory clarity in place, Ripple’s rails scaled hard in 2025.

- On-Demand Liquidity (ODL) hit ~$1.3T in Q2 with ~90% FX coverage.

- Custody now supports 1M+ wallets, reinforcing enterprise readiness.

- Network profile:

- XRPL settles in ~3–5s with negligible fees (~$0.0002 or less) and ~1,500 TPS, fit for retail payouts and bank-grade flows.

- Activity expanded: daily active addresses 100k+ (10× YoY), 3k+ new wallets/day, and 93M+ ledgers closed.

- Capital markets & liquidity: Following the SEC resolution (Aug 2024–25), 11+ spot ETF filings were unlocked, with approximately $1.2B in YTD inflows.

- DeFi & tokenization: ~$306M RWA volume in 2025 (+2,260% YoY). The XRPL EVM sidechain (mainnet July 2025) is live but early.

Bottom line: Ripple’s ecosystem is payments-led, boasts huge corridors, regulatory on-ramps, and progress in tokenization, while on-chain DeFi depth is still catching up.

APT & XRP: Tokenomics Analysis

APT favors adaptive issuance to balance security, dilution, and ecosystem growth; the recent reward cuts are a clear step toward sustainability and deeper capital use in DeFi. XRP offers a fixed supply with escrow smoothing and utility-driven demand through payment corridors and ETFs.

Both models push beyond speculation: APT by making staked capital work across on-chain markets; XRP by converting payment volume into persistent asset demand.

APT: Adaptive Issuance, Staking-Led Security

- Supply model: Inflationary with no hard cap; circulating supply is now >1.1B APT.

- Staking participation: Roughly 70–80% of the eligible supply is staked, indicating strong validator alignment and a high security budget.

- Policy shift (AIP-119): Implemented over three months in 2025, it reduced the base staking APR from ~7% to ~3.79% via ~1% monthly cuts. The aim is to slow monetary expansion, reduce dilution for non-stakers, and bring yields closer to those of competing L1s.

- Behavioral effect: Lower baseline yield nudges holders toward active use of capital (restaking, lending, LP, structured vaults) rather than passive staking alone, supporting DeFi depth without overpaying for idle security.

APT’s issuance is tunable: the network can dial security cost vs. dilution as conditions change. The trade-off is policy discretion, good for responsiveness, but it requires continued governance discipline.

XRP: Fixed Supply, Escrow Cadence, Fee Burn

- Supply model. 100B XRP pre-mined, with no new issuance; a per-tx fee burn creates mild deflationary pressure over time.

- Escrow mechanics. Roughly 36–42B XRP remains in escrow with ~1B/month released; unused portions are commonly re-escrowed, smoothing circulating growth (~59.5B circulating in 2025). This cadence stabilizes supply, akin to inventory management in commodities.

XRP’s design is predictable: it has a fixed stock, a managed flow, and real-world economy usage via ODL. Price discovery is more heavily influenced by utility and liquidity cycles than by monetary surprises.

Closing Thoughts

Aptos and Ripple are closing the gap between on-chain infrastructure and the systems people already use for money. They just approach the job from opposite directions.

Ripple’s edge is institutional reach. The stack is built for predictable settlement, low fees, and compliance workflows that banks and payment firms expect. ODL reduces pre-funding, corridors are live at scale, and the toolset now includes tokenization, a native AMM, and an EVM sidechain for regulated DeFi. If you need global payouts, treasury movement, or bank-grade rails today, Ripple is the reference.

Aptos’ edge is consumer finance at speed. Sub-second UX, sub-cent fees, and trading-native primitives make on-chain activity feel like a modern app. Reordered and scheduled transactions support pro-grade order handling. X-Chain Accounts compress onboarding. Account Abstraction, Permissioned Signer, and Stateless Accounts enable safe automation. With stablecoin depth and growing DeFi volume, Aptos looks and feels like a place to save, pay, and trade in one flow.

Verdict: Ripple remains the benchmark for institutional payments. Aptos is shaping into a low-latency consumer finance engine with trading-grade primitives and a UX that hides crypto friction. If Ripple modernized bank rails, Aptos is modernizing everyday money movement and trading for everyone.