Stablecoins are cryptocurrencies designed to hold a steadier value by tracking a reference asset such as the US dollar. They give crypto users something closer to digital cash: easier to price, move, and hold than highly volatile tokens. In simple terms, if Bitcoin is like a stock that moves every day, a stablecoin is meant to behave more like the money in your wallet.

They are now used for trading pairs, payments, DeFi, savings, and cross-border transfers. Most stablecoins are dollar-pegged, and USDT remains the largest stablecoin by market size.

Editor's Note (May 8, 2026): We fully updated this article in May 2026 to reflect how stablecoins have evolved beyond simple trading pairs. The refreshed guide adds clearer explanations of stablecoin types, peg mechanisms, minting and burning, reserve transparency, DeFi-native models, yield-bearing stablecoins, CBDCs, MiCA, the US GENIUS Act, and the practical risks users should understand before buying or storing stablecoins.

Stablecoin Snapshot | Quick Answer |

|---|---|

Most common peg | US dollar |

Biggest stablecoin | |

Common examples | USDT, USDC, DAI, USDe, PYUSD |

Main use cases | Trading, payments, DeFi, savings, cross-border transfers |

Biggest risks | Reserve risk, de-pegging, regulation, smart contracts, issuer control |

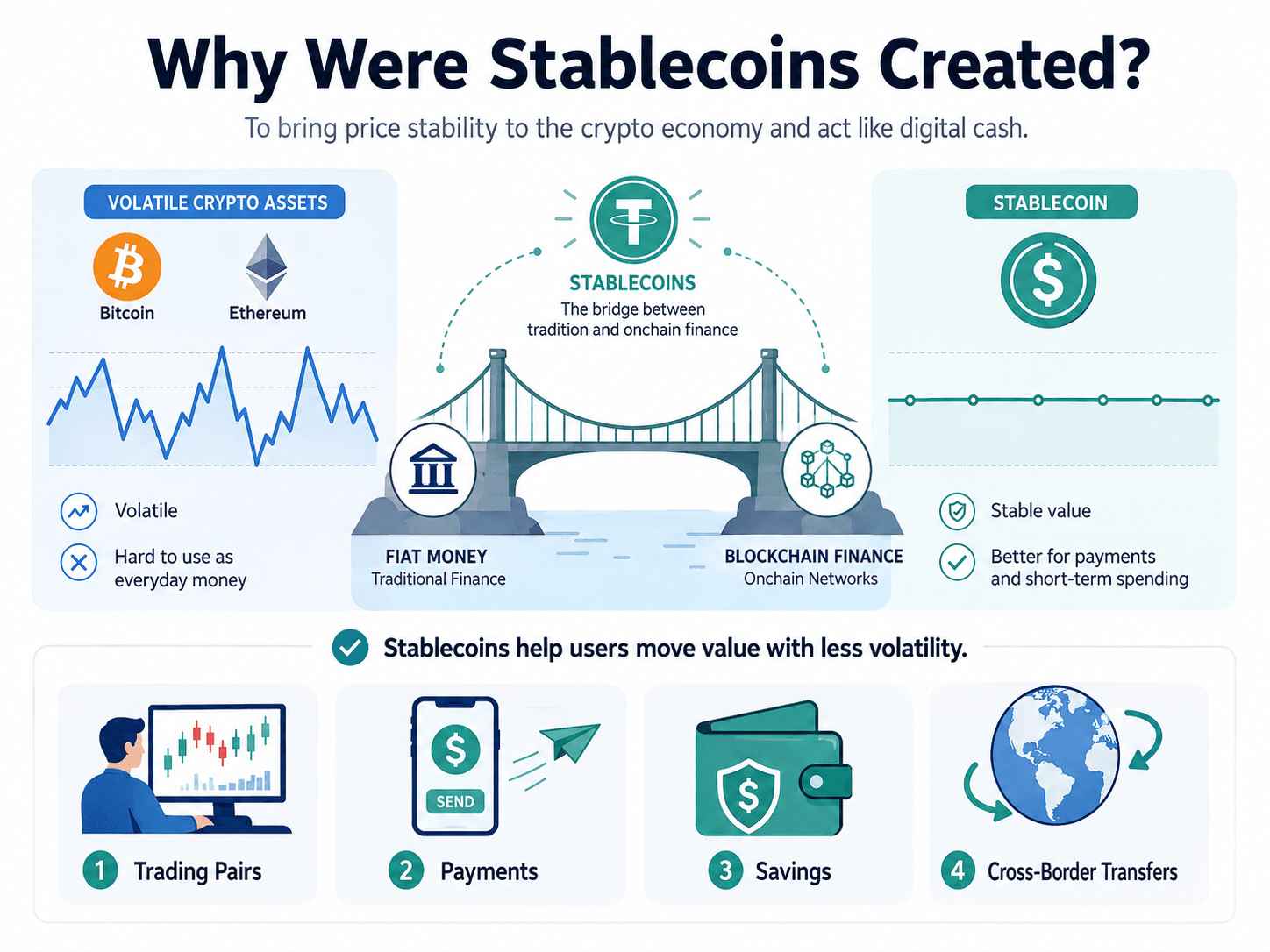

Why Were Stablecoins Created?

Early crypto showed that value could move online without a bank, but it also revealed a practical weakness: assets like Bitcoin and Ethereum can rise or fall too quickly to work well as everyday money. When the value of an asset changes sharply from one day to the next, it becomes difficult to price goods, preserve purchasing power in the short term, or use it confidently for routine transactions.

Stablecoins became the Bridge between Fiat Money and Blockchain-based Finance

Stablecoins became the Bridge between Fiat Money and Blockchain-based FinanceStablecoins were created to solve that problem by giving the crypto economy something closer to digital cash. Today, stablecoins can be used to make payments, and they are also widely used for buying and selling other cryptoassets. In practice, they became the bridge between fiat money and blockchain-based finance, especially as stablecoin infrastructure is linking traditional finance with onchain networks.

Common use cases of stablecoins include:

- Trading pairs, giving traders a stable asset to move into during market swings.

- Payments, especially where blockchain transfers can settle quickly.

- Savings, for users seeking digital dollar exposure rather than volatile cryptoassets.

- Cross-border transfers, where stablecoins can move value across networks more easily than many traditional rails.

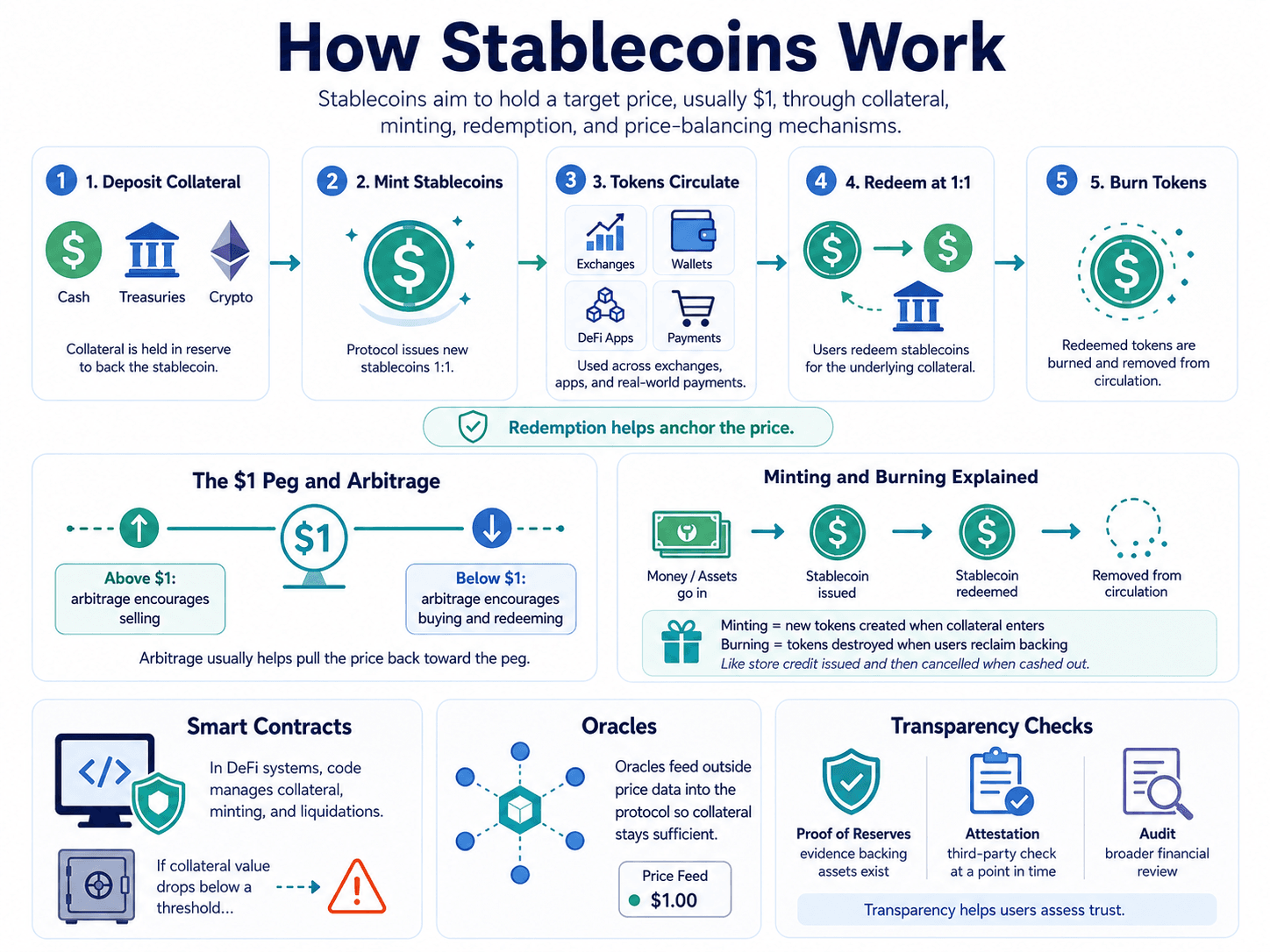

How Stablecoins Work

At a high level, stablecoins try to keep a target price, usually $1, by tying the token to backing assets, collateral rules, or both. In the simplest model, the system works because the token is redeemable for the asset it is meant to track. That redemption link is what gives many stablecoins their price anchor.

Stablecoins Try to keep a Target Price, usually $1, by Tying the Token to Backing Assets, Collateral Rules, or Both

Stablecoins Try to keep a Target Price, usually $1, by Tying the Token to Backing Assets, Collateral Rules, or BothHow the Peg Is Maintained

- A user or institution deposits collateral, such as dollars, Treasuries, crypto, or another approved asset.

- The issuer or protocol mints stablecoins onchain.

- The tokens circulate across exchanges, wallets, DeFi apps, and payment networks.

- In fiat-backed systems, eligible users can usually redeem the stablecoin for the underlying asset, often at 1:1, while issuer terms still matter.

- When stablecoins are redeemed, the tokens are burned or removed from circulation.

- If the market price moves above or below $1, arbitrage traders usually step in to profit from the gap, which helps pull the price back toward the peg.

Minting and Burning Explained

Minting simply means creating new tokens when fresh collateral enters the system. Burning means destroying tokens when users exit and reclaim the backing asset. A useful everyday analogy is a gift card: money goes in, store credit is issued, and that credit disappears once it is spent or cashed out.

The Role of Smart Contracts

In DeFi-native stablecoins, more of the system runs through code rather than a centralized issuer. The Maker Protocol’s docs show that users can generate Dai against crypto collateral, while its liquidation system is designed to sell collateral if a vault falls below required thresholds. That is how crypto-backed stablecoins try to stay solvent even when the collateral itself is volatile.

The Role of Oracles in Stablecoin Pricing

Smart contracts cannot check outside prices on their own, so they rely on oracles. These feed real-world data, such as asset prices or reserve balances, into blockchain applications. For crypto-backed stablecoins, oracle data helps the protocol monitor whether collateral is still worth enough to support the stablecoin supply.

Proof of Reserves, Attestations, and Audits

These terms are related, but they are not interchangeable:

- Proof of reserves refers to evidence that backing assets exist. Chainlink’s Proof of Reserve feeds are one example of reserve-status reporting for tokenized assets.

- Attestation is a third-party check on reported figures at a point in time. For example, Circle says its reserves are disclosed weekly and supported by monthly third-party assurance.

- Full audit is broader and more comprehensive, with the PCAOB outlining the standards auditors follow when expressing an opinion on financial statements.

For issuer transparency, UDST issue Tether says its reports are published quarterly.

Types of Stablecoins

Not all stablecoins stay stable in the same way. The biggest difference is the mechanism behind the peg: some rely on cash-like reserves, some on crypto collateral, some on commodities, and others on automated market incentives.

The table below gives a simple map of the main categories. The risk labels are broad guides, not guarantees, because any stablecoin’s actual risk depends on reserves, redemption rights, smart contracts, and market conditions.

Type | Backing / Mechanism | Examples | Risk Level | Best For |

|---|---|---|---|---|

Fiat-backed | Cash, T-bills, bank deposits, cash equivalents | USDT, USDC, PYUSD, FDUSD | Lower | Trading, payments |

Crypto-backed | Overcollateralised crypto and onchain liquidation rules | DAI, USDS | Medium | DeFi |

Commodity-backed | Physical gold or other real-world assets | PAXG, XAUT | Medium | Onchain gold exposure |

Algorithmic | Supply-demand incentives and market design | UST, earlier Frax model | High | Experimental use |

Yield-bearing | Treasury products, DeFi yield, or hedged funding strategies | sDAI, USDe, USDY | Medium to high | Stablecoin yield |

The examples and backing models above reflect official issuer and protocol materials for USDT, USDC, PYUSD, FDUSD, Dai, PAXG, XAUT, USDe, USDY, plus official material on UST and earlier Frax.

Fiat-Backed Stablecoins: USDT, USDC, PYUSD, and FDUSD

This is the simplest model to understand. A fiat-backed stablecoin aims to hold $1 by keeping reserve assets offchain and offering redemption at or near par. That is the model used by USDT, USDC, PYUSD, and FDUSD. These tokens are usually the easiest for beginners to grasp because they work a lot like digital claim checks for dollar-based reserves.

Crypto-Backed Stablecoins: DAI, USDS, and Overcollateralisation

Crypto-backed stablecoins try to remove more of the centralized issuer layer by locking crypto onchain and issuing a smaller amount of stablecoins against it. The classic example is Dai, which the Maker Protocol lets users generate against crypto collateral. In the same ecosystem, USDS now sits alongside savings products such as sUSDS, but the core idea remains similar: because the collateral can move in price, the system usually needs overcollateralization and liquidation rules to stay solvent.

Commodity-Backed Stablecoins: PAXG and XAUT

Commodity-backed stablecoins are designed to track assets such as gold rather than the US dollar. PAXG gives holders exposure to one fine troy ounce of gold per token, while XAUT represents ownership rights in specific gold bars. They can appeal to users who want blockchain portability with precious-metals exposure, though the peg is to the commodity, not to cash.

Algorithmic Stablecoins and the Terra Luna Collapse

Algorithmic stablecoins rely less on hard reserves and more on incentives, supply adjustments, and related tokens to defend the peg. That design has proven fragile in stress conditions. Official CFTC and SEC material on TerraUSD shows how badly this model can fail when confidence breaks and the market no longer believes the mechanism will restore $1. Earlier Frax models also used a fractional-algorithmic design, though the protocol later moved toward higher collateralization.

Yield-Bearing Stablecoins: sDAI, USDe, and USDY

Yield-bearing stablecoins add another layer: they aim for stability, but they also try to produce returns. sDAI passes through savings-rate yield from the Sky ecosystem, USDe uses a delta-neutral crypto structure, and USDY is a tokenized note secured by short-term US Treasuries and bank demand deposits. This category can be useful, but it is also more complex because the source of the yield becomes part of the risk.

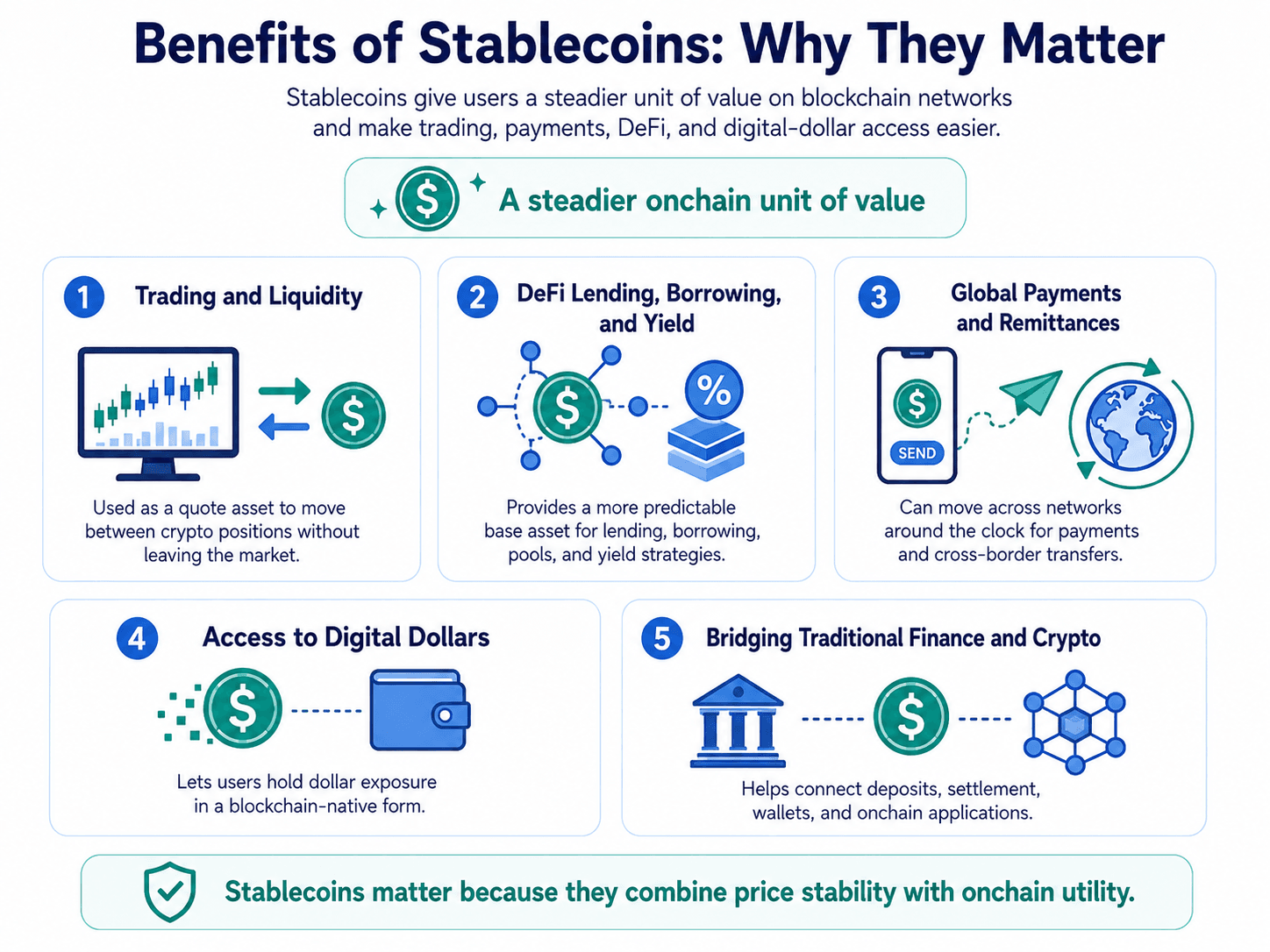

Benefits of Stablecoins: Why They Matter

Stablecoins give crypto users a steadier unit of value inside blockchain networks. Instead of moving in and out of bank accounts every time markets turn volatile, users can hold an onchain asset that is built to stay closer to a known reference point, usually the US dollar. Let's see some of the benefits stablecoins carry.

Stablecoins Sit between Bank Money and Blockchain Infrastructure

Stablecoins Sit between Bank Money and Blockchain InfrastructureTrading and Liquidity

Stablecoins are used for trading because they act as quote assets on exchanges, making it easier to move between volatile tokens without leaving the crypto market. They are also widely used for buying and selling other cryptoassets.

DeFi Lending, Borrowing, and Yield

Stablecoins are used across DeFi because they provide a more predictable base asset for lending, borrowing, liquidity pools, and yield strategies. That makes them easier to build around than highly volatile tokens.

Global Payments and Remittances

Stablecoins are used for payments because they can settle around the clock and move across networks without depending on traditional banking hours. They are also used for cross-border transfers, though speed and fees still depend on the chain being used.

Access to Digital Dollars

Stablecoins are used as digital dollars by users who want dollar exposure in a blockchain-native form, especially where access to physical dollars or dollar banking is limited.

Bridging Traditional Finance and Crypto

Stablecoins sit between bank money and blockchain infrastructure, helping connect deposits, settlement, wallets, and onchain applications into one usable system.

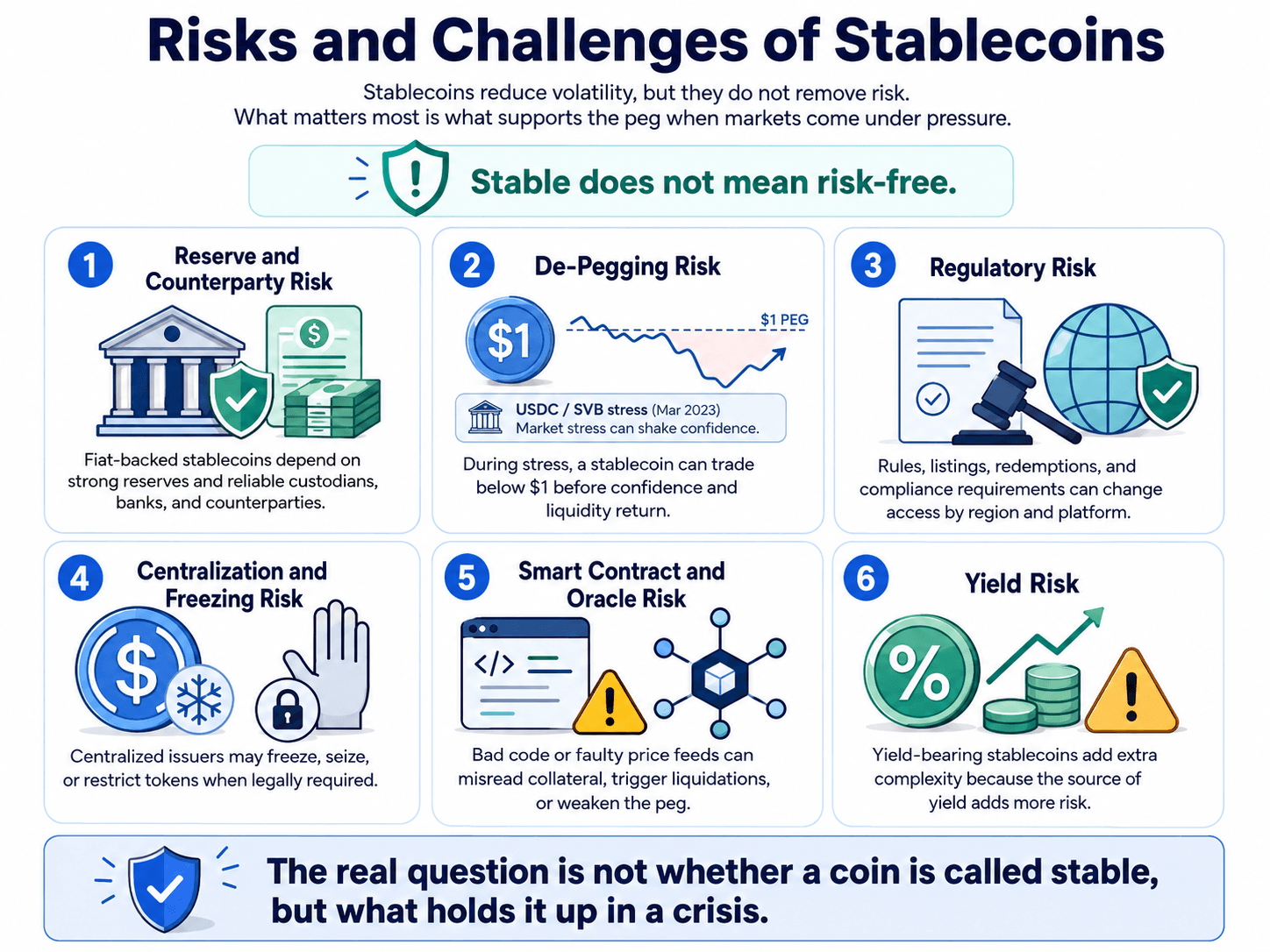

Risks and Challenges of Stablecoins

Stablecoins reduce price volatility, but they do not remove risk. The main question is not whether a token is called “stable,” but what is holding it up when markets come under pressure.

Stablecoins Reduce Price Volatility, but they do not Remove Risk

Stablecoins Reduce Price Volatility, but they do not Remove RiskReserve and Counterparty Risk

Fiat-backed stablecoins depend on the quality of their reserves and the institutions holding them. If the backing assets are weaker than expected, become less liquid, or get tied up at a custodian or bank, redemptions can become harder just when users need them most.

De-Pegging Risk

A stablecoin can still trade below $1 on the secondary market during stress. That happened in March 2023, when reserve exposure to Silicon Valley Bank briefly shook confidence in USDC before the peg recovered.

Regulatory Risk

Stablecoin access can change by region, exchange, and issuer. Rules around listings, redemptions, disclosures, and compliance can all affect whether a stablecoin remains available to ordinary users.

Centralization and Freezing Risk

Centralized issuers can restrict transfers or freeze tokens when legally required. Under the GENIUS Act, payment stablecoin issuers must have the technical ability to seize, freeze, or burn tokens when required by law.

Smart Contract and Oracle Risk

DeFi-based stablecoins add code risk. If a contract fails or oracles deliver bad pricing data, the system can misread collateral, trigger liquidations, or weaken the peg.

Yield Risk

Yield-bearing stablecoins add another layer of complexity. The return may come from duration exposure, protocol design, or derivatives funding, which is why official risks disclosures often include liquidation, custodial, exchange, and backing-asset risk.

Are Stablecoins Safe?

Stablecoins are not risk-free. Their safety depends on the quality of their reserves, whether they are redeemable, their regulatory status, and, in DeFi models, how collateral and liquidations are handled. In broad terms, fiat-backed coins are usually simpler to assess, while yield-bearing and algorithmic models introduce more moving parts.

Stablecoin Type | Relative Risk | Why |

|---|---|---|

Regulated fiat-backed | Lower | Backed by cash or T-bills, but still issuer-dependent |

Crypto-backed | Medium | Overcollateralized, but exposed to collateral volatility |

Commodity-backed | Medium | Depends on custody, redemption, and the underlying asset |

Yield-bearing | Medium to high | The yield source adds extra layers of risk |

Algorithmic | High | Historically more fragile during market stress |

Questions to Ask Before Using a Stablecoin

Before using any stablecoin, it helps to ask a few basic questions. These do not guarantee safety, but they can quickly reveal whether a stablecoin is simple and transparent or more complex than it first appears.

- Who issues it? A regulated company, a protocol, or a DAO all come with different levels of accountability.

- What backs it? Cash, Treasuries, crypto collateral, or a more complex strategy can lead to very different risk profiles.

- Can it be redeemed? A clear redemption process is often one of the strongest supports for a stable peg.

- Are reserves disclosed? Regular disclosures make it easier to judge whether the backing looks credible.

- Is it regulated in your region? Availability and protections can differ depending on local rules.

- Has it de-pegged before? Past stress events can reveal how a stablecoin behaves when confidence weakens.

- Is the yield source easy to understand? If the return sounds vague or overly complex, the risks may be harder to judge too.

Stablecoins vs CBDCs: Key Differences

Stablecoins and CBDCs may both look like digital money, but they come from very different systems. A CBDC is public money issued by a central bank, while stablecoins are private digital tokens issued by companies or protocols. That difference shapes how each one is backed, who controls it, and where it is mainly used.

Feature | Stablecoins | CBDCs |

|---|---|---|

Issuer | Private company, protocol, or DAO | Central bank or government |

Examples | USDT, USDC, DAI, PYUSD | |

Backing | Reserves, collateral, or peg mechanisms | Central bank liability |

Access | Often global and crypto-native | Usually tied to a jurisdiction |

Privacy | Often pseudonymous on public chains, but traceable | Depends on design and law |

Main use today | Trading, DeFi, payments | Mostly pilot or design-stage public payments |

Will CBDCs Replace Stablecoins?

Probably not. The Federal Reserve said different forms of money can be complementary, while the Bank of England says no decision has been made on whether to introduce a digital pound. In practice, the two may coexist because they serve different legal, institutional, and user needs.

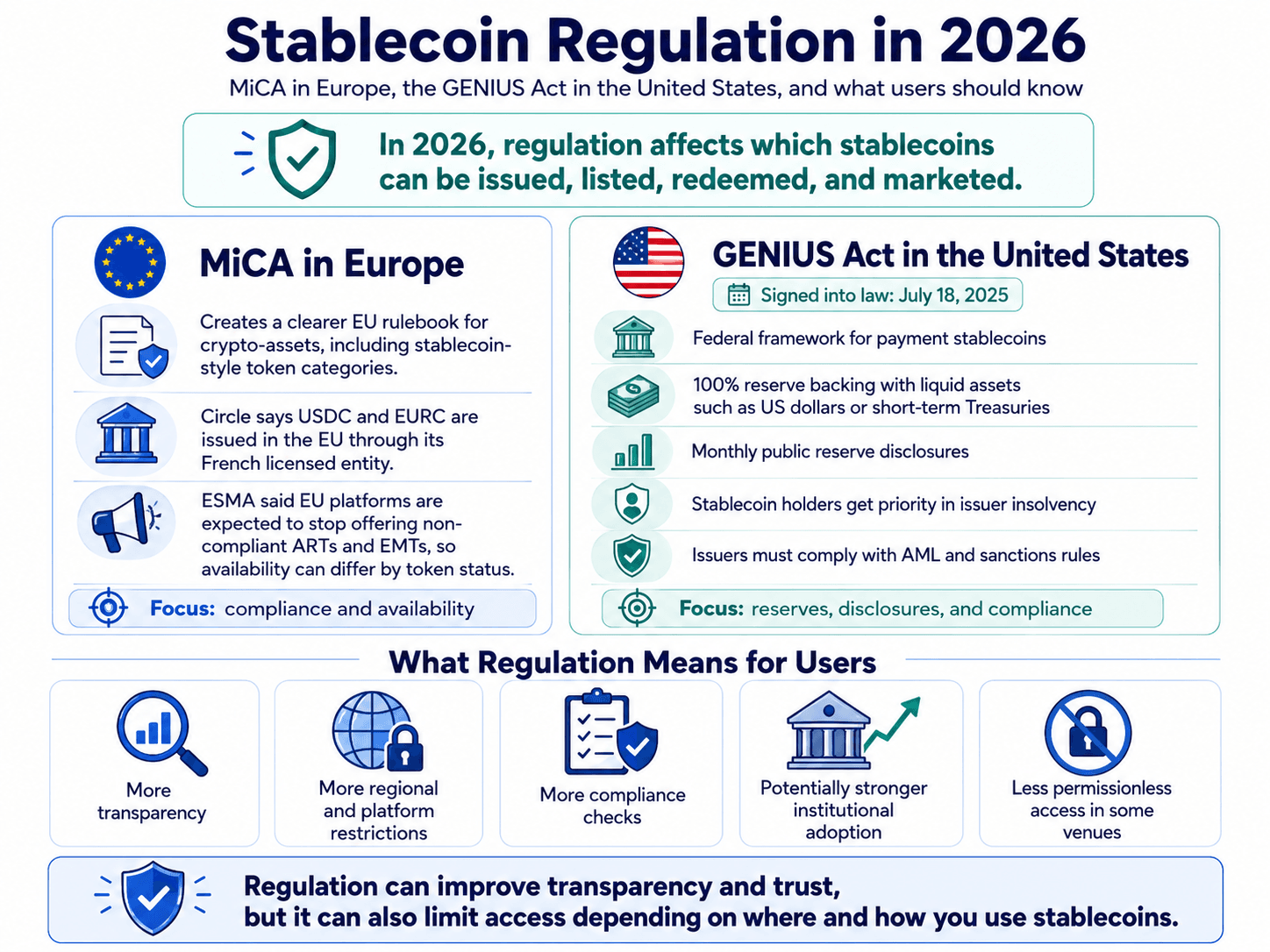

Stablecoin Regulation in 2026: MiCA, the GENIUS Act, and What Users Should Know

Stablecoin rules are no longer just a future issue. In 2026, they already shape which tokens can be issued, listed, redeemed, and marketed in major regions. For users, regulation affects not only safety and transparency, but also simple things like which stablecoins are available on a given platform.

Today, Stablecoins Shape which Tokens can be Issued, Listed, Redeemed, and Marketed in Major Regions

Today, Stablecoins Shape which Tokens can be Issued, Listed, Redeemed, and Marketed in Major RegionsMiCA in Europe

The EU’s MiCA framework created a clearer rulebook for crypto-assets, including stablecoin-style e-money tokens and other regulated token categories. Circle says USDC and EURC are issued in the EU in compliance with MiCA through its French licensed entity. At the same time, ESMA has said platforms in the EU are expected to stop offering non-compliant ARTs and EMTs, which means availability can differ depending on a token’s status.

The GENIUS Act in the United States

The GENIUS Act was signed into law on July 18, 2025. According to the White House, it creates a federal framework for payment stablecoins, requires 100% reserve backing with liquid assets such as US dollars or short-term Treasuries, mandates monthly public reserve disclosures, gives stablecoin holders priority in issuer insolvency, and subjects issuers to AML and sanctions obligations.

What Regulation Means for Users

- More transparency around reserves and disclosures.

- More restrictions based on region or platform.

- More compliance checks during onboarding and use.

- Potentially stronger institutional adoption.

- Less permissionless access in some venues.

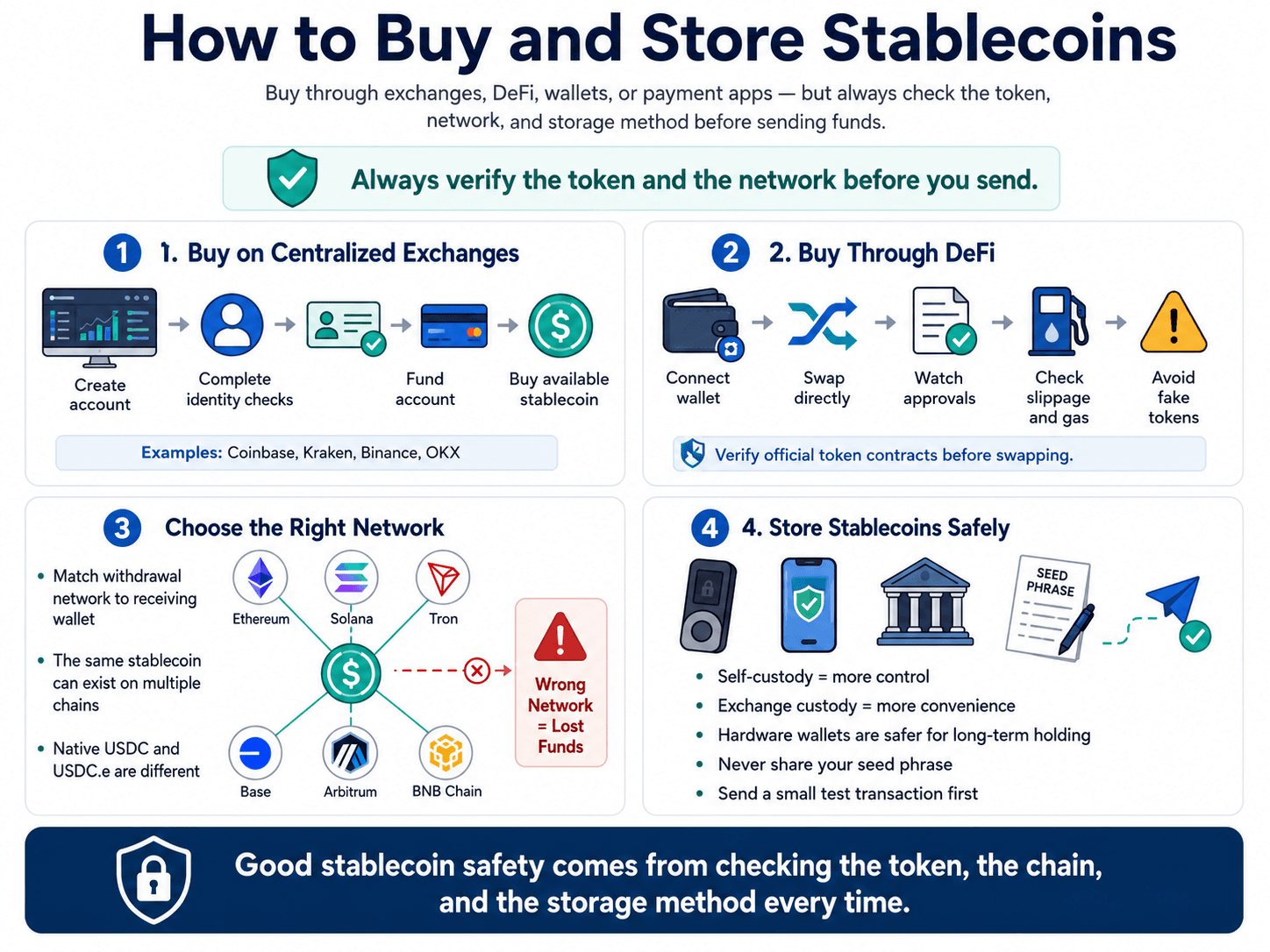

How to Buy and Store Stablecoins

You can buy stablecoins through a centralized exchange, a decentralized exchange, a wallet app, or, in some regions, payment-linked apps. The main thing is to check both the token and the network before you send anything, because the same stablecoin can exist in more than one version across different chains.

You can Buy Stablecoins through a Centralized Exchange, a Decentralized Exchange, a Wallet App, or Payment-Linked Apps

You can Buy Stablecoins through a Centralized Exchange, a Decentralized Exchange, a Wallet App, or Payment-Linked AppsBuying Stablecoins on Centralized Exchanges

On Coinbase, Kraken, Binance, or OKX, the basic flow is usually the same: create an account, complete identity checks where required, fund it, and buy the stablecoin available in your region.

Buying Stablecoins Through DeFi

On DEXs and aggregators, you connect a wallet and swap directly, but you still need to watch approvals, fake tokens, slippage and gas. 1inch notes that swaps may require both an approval and the swap itself, while Coinbase warns users to verify official token contracts when checking for fake stablecoins.

Choosing the Right Network

Stablecoins commonly move on Ethereum, Solana, Tron, Base, Arbitrum, and BNB Chain. Always match the withdrawal network to the receiving wallet, because on Arbitrum, for example, native USDC and bridged USDC.e are treated differently.

Storing Stablecoins Safely

For storage, self-custody gives you more control, while exchange custody is simpler but depends on the platform. Hardware wallets are generally safer for long-term holding, your seed phrase should never be shared, and a small test transaction is smart before sending a large amount.

Closing Thoughts

Stablecoins are no longer just tools for crypto trading. They now sit at the intersection of payments, DeFi, digital dollar access, treasury-backed products, and regulation. That is a big shift from the early view of stablecoins as simple parking spots between trades.

The next phase will likely be shaped by better transparency, clearer rules under MiCA, and the US GENIUS Act, all of which make stablecoins easier for institutions to evaluate and harder for issuers to treat casually.

That said, stablecoins only reduce exposure to crypto volatility. They do not remove financial risk. Users still need to understand reserves, redemption, regulation, and how each stablecoin actually works before treating it as safe.