Compound has recently become the largest lending protocol in Decentralized Finance (DeFi).

The introduction of its COMP token on June 17th sent the crypto world into a frenzy as users rushed to deposit their assets and earn unholy amounts of interest along with daily rewards paid in COMP for participating in the ecosystem as a lender and/or borrower.

Hype is still on the horizon with Binance listing the COMP token on June 25th, causing a 25% spike in price on Poloniex. The sudden drop in crypto markets during the same period has not phased Compound users, who still have over 600 million USD worth of crypto locked on the platform.

By the end of this article you will understand why people are so excited about Compound as well as its significance in the world of DeFi.

What is DeFi?

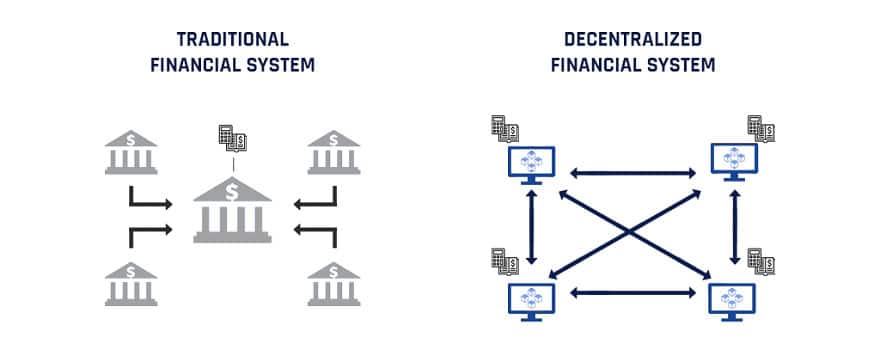

If you want to wrap your head around Compound Finance, you first need to fill it with the knowledge of DeFi. In a sentence, DeFi allows anyone on the internet to access financial services in a secure, decentralized, and private manner without the use of a middleman. This includes saving, trading, lending, and just about anything else you would usually do with money that involves centralized third parties such as banks.

Decentralized finance vs. traditional finance: Image Source

Decentralized finance vs. traditional finance: Image SourceAs you might have guessed, this ecosystem involves cryptocurrencies and not fiat currencies (although stablecoin cryptos which are “pegged” to the price of a fiat currency such as USDT or USDC are commonly used in DeFi). The overwhelming majority of popular DeFi decentralized applications (Dapps) and the assets used within them are built on the Ethereum blockchain.

Decentralized exchanges in cryptocurrency: Image Source

Decentralized exchanges in cryptocurrency: Image SourceDeFi has been a hot topic in cryptocurrency for quite some time, well before Compound took centre stage. Up until recently, the spotlight in recent months had actually been on DeFi protocols such as Kyber Network, Uniswap, and Bancor which provide decentralized exchange (DEX) services. The ‘endgame’ of DeFi is effectively the total elimination of third parties in all value transactions (yes, even Binance).

What is Compound?

Compound is a decentralized lending platform that was created by Californian company Compound Labs Inc. in September of 2018. Like many other protocols in DeFi, Compound is built on the Ethereum blockchain. Although Compound was initially centralized, the recent release of its governance token, COMP, marks the first step in turning Compound into a community-driven decentralized autonomous organization (DAO).

While Compound’s goal has been stated in many different ways in many different places, the underlying idea is this: put your idle cryptocurrency to use. The Compound protocol lets users to lend and borrow 9 Ethereum-based assets including Basic Attention Token (BAT), 0x (ZRX) and Wrapped BTC (wBTC).

The Compound finance protocol: Image via Compound Finance

The Compound finance protocol: Image via Compound FinanceAt the time of writing, you can earn annual interest (also known as APY) of over 25% when lending BAT. No Know Your Customer (KYC), Anti Money Laundering (AML) or credit record is required to use Compound.

Users of the platform do not just have the potential to earn crazy interest rates but are also rewarded in COMP tokens for borrowing or lending cryptocurrency. Given the high price of the COMP token, this has opened the door to some brain-teaser level of DeFi gymnastics that has allowed users to increase their APY to over 100%.

This is a large part of why people are crazy about compound. We will explain how such insane interest rates are possible later in a moment. First, we need to cover how Compound works.

How Does Compound Work?

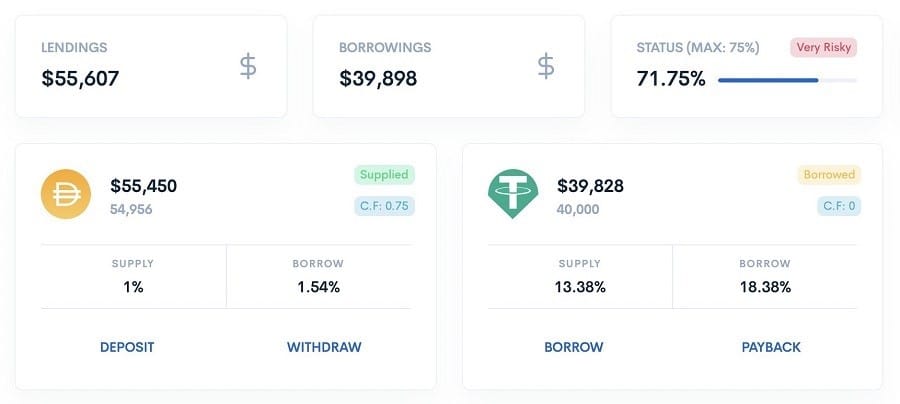

As mentioned, in the Compound protocol users can deposit cryptocurrency as lenders and/or withdraw cryptocurrency as borrowers. Instead of lending directly to borrowers, lenders combine their assets into asset pools from which users can borrow.

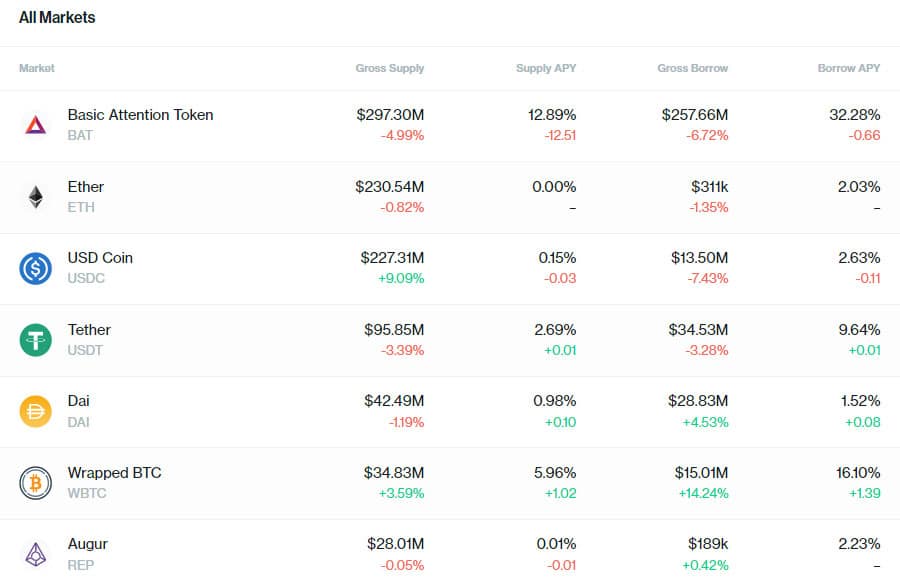

Compound lending pools: Image via Compound Finance

Compound lending pools: Image via Compound FinanceThere is a pool for every asset (Basic Attention pool, 0x pool, USDC pool, etc.). Users can only borrow a USD value in crypto that is below the collateral they have supplied (e.g. 60% of the collateral). The amount they can borrow depends on the liquidity and market cap of the collateral.

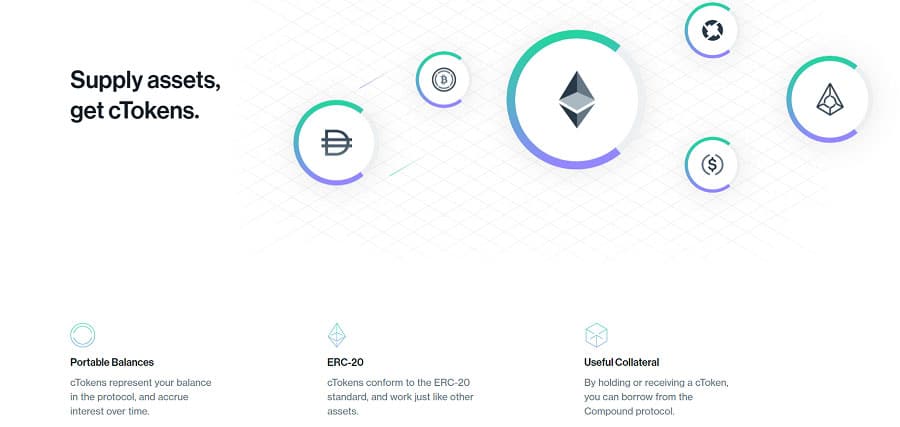

When you lend cryptocurrency on Compound, you received an amount of corresponding cTokens that is generally much larger than the amount of crypto you deposited. cTokens are ERC-20 tokens which represent a fraction of the underlying asset.

For example, at the time of writing, lending 1 DAI would give you almost 49 cDAI in Compound. cTokens exist to allow users to earn interest. Over time, users can purchase more of the underlying asset they deposited with the same fixed about of cToken they received.

Compound cTokens explained: Image via Compound Finance

Compound cTokens explained: Image via Compound FinanceIn contrast to legacy borrowing services, interest rates are neither fixed nor agreed upon by the two parties involved in the transaction. Instead, the interest rate is determined by supply and demand and constantly updated by a complex algorithm.

As a rule of thumb, the greater the demand there is for an asset, the higher the interest rates will be for both lenders and borrowers. This gives incentive to lenders to lend and deters borrowers from over-borrowing. Lenders can also withdraw their assets at any time.

If a user has borrowed more than what they were permitted due to a drop in the price of the asset they provided as collateral, they risk the liquidation of that collateral. Holders of the borrowed asset can choose to liquidate the collateral and purchase it at a discounted price. Alternatively, borrowers can pay back a portion of their debt to increase their borrowing capacity above the threshold of liquidation and carry on as usual.

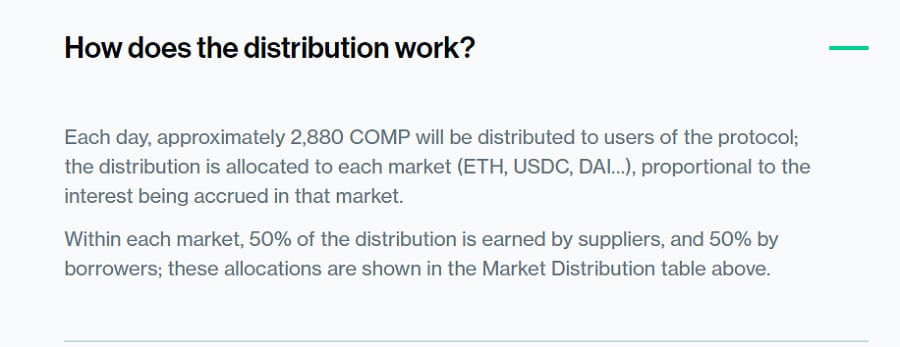

Compound Liquidity Mining

The main idea behind liquidity mining is to give incentives to both lenders and borrowers to use the Compound protocol. The reasoning is that failure to do this would result in a gradual decline of the platform as lenders and borrowers gradually drop off or move to similar protocols in the DeFi space. To ensure a consistently high level of liquidity and participation, Compound rewards both lenders and borrowers in COMP tokens.

Compound liquidity mining explained: Image Source

Compound liquidity mining explained: Image SourceThis is done using a smart contract and the distribution COMP rewards are based on a handful of factors including the interest rates of an asset’s lending pool and the amount of people interacting with the lending pool. 2880 COMP tokens are distributed daily with half going to borrowers and the other half to lenders.

What does the COMP token do?

In addition to being the carrot on the stick that motivates users to use Compound, the COMP token gives users governance over the protocol. This allows users to have a say in the future of Compound. 1 COMP token is required to cast a vote, and votes can be delegated to other users of the protocol without needing to actually transfer the token to them.

Compound governance token: Image via Compound

Compound governance token: Image via CompoundAll proposals made in Compound consist of executable code. A user must have 1% of the total COMP supply on hand or delegated from other users to table a proposal. Once submitted, there is a 3-day voting period wherein a minimum of 400 000 votes must be cast. If more than 400 000 votes affirm the proposal, the new change implemented after a 2-day waiting period.

The COMP ICO

There was no initial coin offering (ICO) for the COMP token. Instead, nearly 60% of the 10 million token supply was allocated to investors, founders, current team members, future team members, and community growth.

Specifically, just under 2.4 million COMP tokens were given to shareholders of Compound Labs Inc., just over 2.2 million were given to the Compound founders and team, just under 400 000 have been saved for future team members, and just under 800 000 have been allocated for community initiatives.

The distribution of COMP tokens: Image via Compound

The distribution of COMP tokens: Image via CompoundThe remaining 4.2 million tokens will be distributed to the users of the protocol over a 4-year period (assuming a consistent daily distribution of 2880). It is worth noting that the 2.2 million COMP tokens given to Compound’s founders and team members is apparently temporary and will be ‘returned’ after a 4-year period. This is to allow for a transition period wherein the founders and team can still guide the protocol via voting as it gradually becomes “fully” autonomous / community driven.

Cryptocurrency Yield Farming

Although the philosophical reasons for DeFi’s existence are all well and good, what really has people rushing to platforms like Compound right now is the ability to leverage smart contracts within and between various DeFi protocols to receive impossibly high interest rates.

In the cryptocurrency community this is known as yield farming and fundamentally involves a mind-bending mix of borrowing, lending, and trading that would put the Federal Reserve to shame.

Cryptocurrency yield farming profits: Image Source

Cryptocurrency yield farming profits: Image SourceYield farming is extremely risky, and many consider it to be a variation of leverage trading. This is because it makes it possible for users to trade sums of crypto much larger than the underlying amount they have actually put down.

You can think of it as your own personal pyramid scheme with the pyramid flipped upside down. The entire structure is reliant on a single asset which must either increase in price or stay the same or else everything comes crashing down.

The specifics of how yield farming works depends primarily on the asset you are trying to accumulate. In terms of Compound, yield farming involves maximizing your return in COMP tokens for participating in the ecosystem as BOTH a lender and borrower.

This effectively allows users to make money from borrowing cryptocurrency in Compound. This is done using a platform called InstaDapp, a dashboard that lets you interact with multiple DeFi apps from a single point of reference.

Compound Yield Farming

InstaDapp offers a feature called “Maximize $COMP mining” which can give you a more than 40x increased return in COMP tokens. The short of it is that the USD amount of COMP tokens you receive outweighs the USD value of the interest you owe on the money you have borrowed. How this works was detailed quite nicely in this YouTube video but if you do not have 30 minutes to watch it, we will break it down for you in a single paragraph.

Suppose you have 100 DAI. You deposit the 100 DAI into Compound. Since Compound allows you to use those funds even though they are “locked”, you use the 100 DAI with the “Flash Loan” feature in InstaDapp to borrow 200 USDT from Compound.

Yield farming with Compound: Image Source

Yield farming with Compound: Image SourceYou then convert the 200 USDT into (roughly) 200 DAI and put the 200 DAI back into compound as a lender. You are now lending 300 DAI and owe 200 USDT. This gives you a return in COMP which gives you an annual interest rate in USD that can easily exceed 100% even after accounting for the interest rate you pay for borrowing the 200 USDT.

Magic, right?

As mentioned earlier, the success of this scheme is dependent on the stability or growth of the underlying asset. For example, even though DAI is technically a stablecoin, it can still fluctuate by a fraction that is large enough to soak the sandcastle and bring it down. This tends to happen to stablecoins when the rest of the market fluctuates and traders rush to hedge their losses using fiat-pegged tokens.

The Compound Roadmap

Unlike many cryptocurrency projects, Compound does not really have a roadmap. In the words of Compound Labs Inc. CEO Robert Leshner “Compound was designed as an experiment”.

Compound development goals: Image via Compound Blog

Compound development goals: Image via Compound BlogThis quote is taken from a Medium post from March of 2019 which appears to be the closest thing to a roadmap you can find from Compound. It details 3 goals the project wished to achieve: enabling support for multiple assets, allowing each asset to have its own collateral factor, and becoming a DAO.

In the months that followed, Compound posted regular development updates to Medium. The most recent post was earlier this month and its subtitle states the following: “Our core work on the Compound protocol is done. It’s time for the community to take charge.” Considering the development team seems to have successfully achieved the 3 goals it outlined just over a year ago, it seems that Compound may be one of the few “finished” cryptocurrency projects.

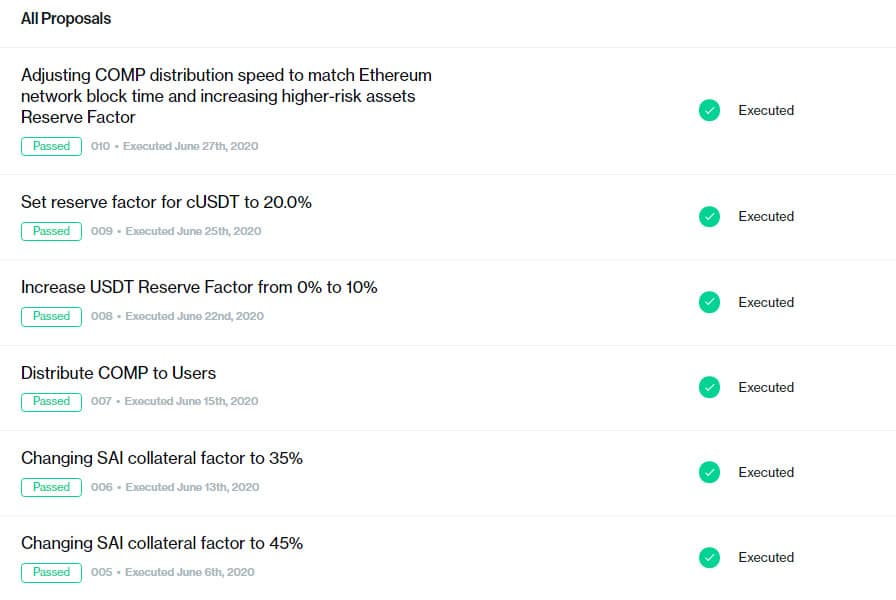

Compound development proposals: Image via Compound

Compound development proposals: Image via CompoundIn reality, the future of Compound will be determined by its community. Based on the publicly viewable Governance Proposals within compound, most appear to involve adjusting reserve factors and collateral factors for supported assets.

In short, reserve factors are a small portion of the interest paid on loans by borrowers which are set aside as a “liquidity cushion” in the event of low liquidity. A reserve factor is the percentage of the collateral you can borrow as a borrower. It is also likely that more assets will be added to Compound as time goes on.

Compound Finance vs. MakerDAO

Up until Compound rushed the stage, MakerDAO was the most popular DeFi project on Ethereum. For those unfamiliar, MakerDAO also allows users to borrow cryptocurrency using Ethereum, BAT or wBTC as collateral.

However, the cryptocurrency you can borrow is not “just another” Ethereum-based asset, but an ERC-20 stablecoin called DAI which is ‘soft-pegged’ to the US dollar. Unlike USDT or USDC which are backed by centralized assets held in custody, DAI is fully decentralized and backed by crypto.

Compound Finance vs. MakerDao

Compound Finance vs. MakerDaoAs in Compound, MakerDAO does not let you borrow the full amount of the Ethereum collateral you deposited in DAI. Instead, you can only borrow 66.6% of the USD value of the Ethereum you have put down as collateral. This means that if you deposited 100$ worth of Ethereum as collateral, you would be able to withdraw roughly 66 DAI as a loan. In contrast to Compound, this reserve factor is not subject to change and DAI is the only asset which can be borrowed on the platform.

Both MakerDAO and Compound have been used to yield farm. Funny enough, Compound users were borrowing DAI on MakerDAO to lend it in Compound when it had the highest interest rate. MakerDAO also gives users the option to lock up their DAI in return for interest.

MakerDAO’s focus on DAI. Image via MakerDao

MakerDAO’s focus on DAI. Image via MakerDaoWhile there are many differences between the two DeFi giants, the two most notable are 1) that the goal of MakerDAO is fundamentally to support the DAI stablecoin and 2) that Compound gives users additional incentive beyond interest rates (COMP) to participate in the protocol.

How it is that Compound overtook MakerDAO so quickly is quite easy to understand when you put the two protocols side by side. In addition to greater incentives for participation, Compound also supports substantially more assets for lending and borrowing. This gives it the advantage when it comes to yield farming, which is arguably the driving factor behind these kinds of DeFi protocols.

Furthermore, Compound is much easier to understand and use than MakerDAO, which has elaborate borrowing fees and protocols that exist primarily to ensure the stability of DAI. You can see how that works here.

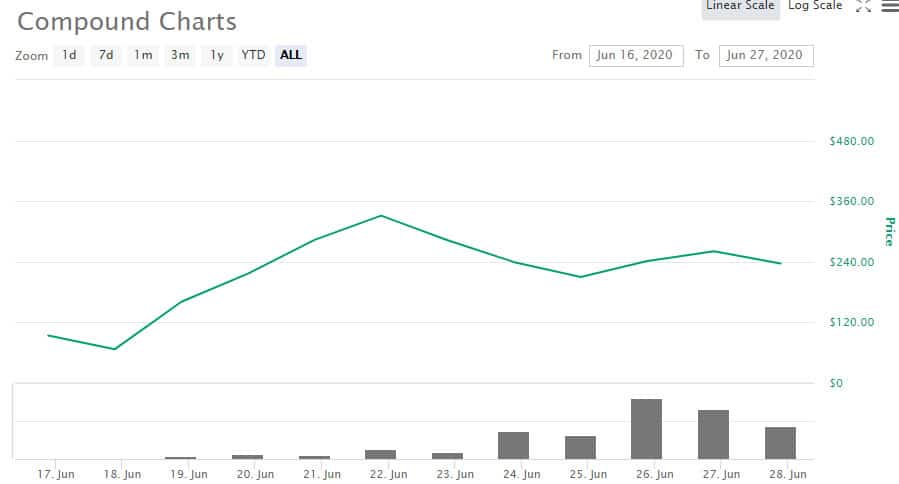

COMP Price Analysis

The price history for COMP is quite limited considering it has only been on the markets for 2 weeks. During this time, it went from a price of around 60$USD to over 350$USD in a matter of days. It has since pulled back around 30% but remains steady as cryptocurrency markets slip into negative percent changes.

COMP Price Performance: Image Source

COMP Price Performance: Image SourceOddly enough, it seems that Compound is also keeping BAT in positive percentage territory since it is currently the asset with the highest interest rate on the platform (around 25%).

At the time of writing, COMP is once again rallying up by over 10 percent following an announcement from Coinbase that the token has officially been listed for trading. Whether successive listings by large exchanges is what is keeping the asset closer to the moon than the Earth cannot as of yet be said with certainty.

Considering its appeal over similar protocols such as MakerDAO, it does not seem likely that this asset will retrace back to 60$USD without another black swan event (not financial advice!).

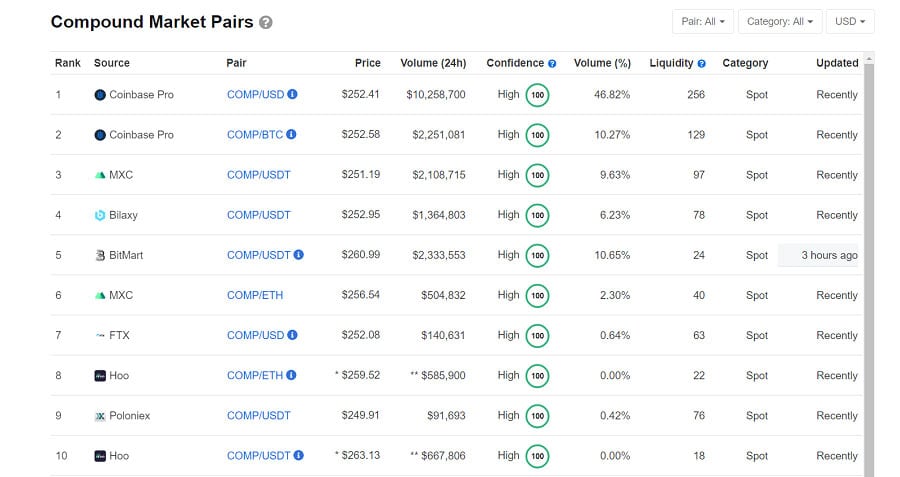

Where to get COMP Cryptocurrency

At the time of writing, you can buy COMP on about a dozen exchanges including Coinbase, Binance, and Poloniex. Oddly enough, the Binance pairings are not yet listed on CoinMarketCap but include BTC, USDT, BNB, and BUSD.

COMP Markets & Trading Pairs: Image Source

COMP Markets & Trading Pairs: Image SourceWhen combined, the 24-hour volume on Binance is on par with Coinbase Pro. The total 24-hour volume is quite low given its market cap but if you are looking to get your hands on COMP there is absolutely no shortage of liquidity on Binance and Coinbase Pro for the time being.

COMP Cryptocurrency Wallets

Since COMP is an ERC-20 token, it can be stored on just about any wallet which supports Ethereum. The list is long but includes the likes of Exodus wallet, Trust Wallet, Atomic Wallet, Ledger and Trezor physical wallets, and browser wallets such as MetaMask.

If you are using Compound and do not intend on voting, make sure to regularly transfer your accumulated COMP tokens to your own wallet from time to time. Just keep in mind that you must have at least 0.001 COMP accumulated if you want to withdraw it.

What we think about Compound

While we are stoked about Compound, there are a few peculiarities that have surprisingly not attracted much attention. The first is the exceptionally high allocation of COMP tokens to stakeholders, founders, and team members. As mentioned previously, this accounts for around 60% of COMP’s total supply.

If this were any other token, traders and investors would run to the hills. When the founders and backers of a cryptocurrency project have the lion’s share of the asset, this leaves other token holders open to a pump and dump scheme reminiscent of the ICO craze in 2017-2018.

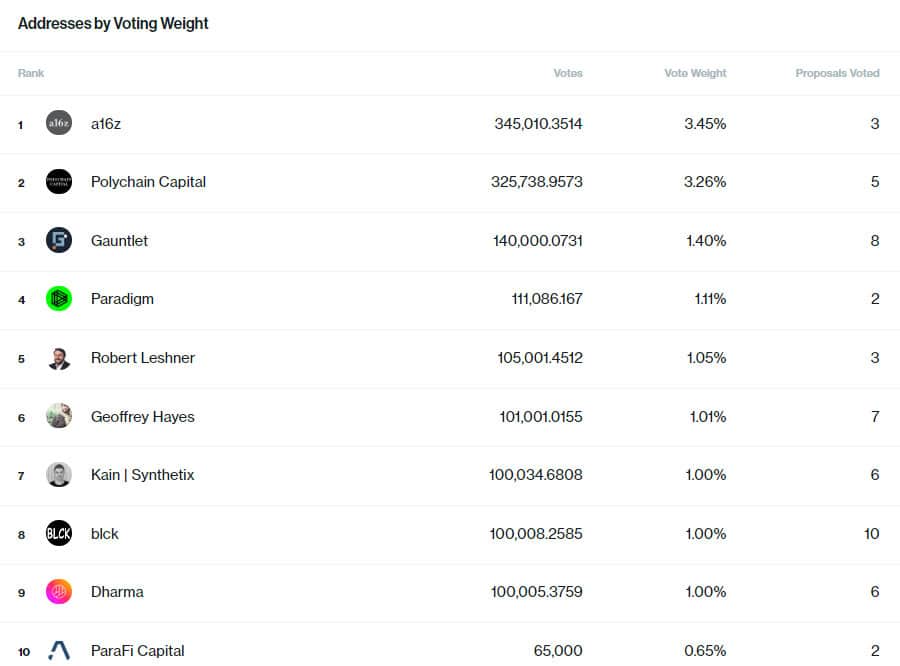

Who holds the most COMP cryptocurrency?: Image via Compound Finance

Who holds the most COMP cryptocurrency?: Image via Compound FinanceSecond, it appears as if the founding members and investors which backed Compound Labs Inc. are very involved in Compound’s community governance. The publicly viewable “Top Addresses by Voting Weight” shows that nearly all of the top 50 COMP token holders consist of people involved in Compound Labs Inc.

Interestingly enough, yield farming provider InstaDapp is also in the top 10. This means that despite being community driven, Compound is still very much in the hands of its original stock.

Third, it is hard to see how lending protocols such as Compound could have any practical use in the real world. This is primarily because it is somewhat pointless to borrow an amount of an asset that is less than what you currently hold.

Lenders and borrowers on Compound: Image via Exodus

Lenders and borrowers on Compound: Image via ExodusFor the time being, very few DeFi protocols allow you to borrow more than you own. This is not an issue for those interested in yield farming, but in the real world being able to borrow more than you own is the central value proposition of having lending services in the first place.

While it is true that the prospect of saving your money with a DAO would be more profitable (and perhaps even more secure) than doing so though a bank, it seems hard to imagine how those high APY rates would remain if there was a sudden surge in lending supply by retail investors.

Compound’s own algorithm would lower the interest rate to a level that might be comparable to a bank. This is because it is doubtful whether there would be an equivalent surge in people wanting to borrow less than they currently own.

Black Swan Events

Our final concern with Compound is how it could handle a black swan event. For those unfamiliar, a black swan event is an unforeseen external circumstance which disrupts markets. The current pandemic is an example of a black swan event as it sent stocks and cryptocurrencies into a freefall in March of this year.

Whereas centralized institutions have some wiggle room in terms of responding to these sorts of market fluctuations, DAOs operating off pre-programmed smart contracts do not.

Cryptocurrency market crash March 2020: Image Source

Cryptocurrency market crash March 2020: Image SourceUnderstanding why this is a problem can be best understood by examining what happened to MakerDAO during the March flash crash. As mentioned earlier, the purpose of MakerDAO is ultimately to uphold the stability of the DAI token. Simply put, this involves maintaining a balance between the USD value of DAI in circulation and the USD value of the collateral which backs it. This is done by minting and burning DAI against the existing collateral in various contexts.

When the March black swan spread its wings causing a sharp drop in cryptocurrency prices, this triggered a significant number of borrowers’ “vaults” to have their collateral liquidated. Why? Because the amount of DAI they had borrowed was suddenly more than the 66.6% reserve threshold they need to stay below to avoid liquidation.

MakerDAO collateral vault auctions: Image Source

MakerDAO collateral vault auctions: Image SourceAs you can imagine, the other users in the system which would normally buy the liquidated collateral at a discount were hesitant to do so, meaning there was nobody to buy it and bring equilibrium to the protocol (since DAI is used to buy the collateral and is burned when doing so).

When you remember that networks can become extremely congested in times of volatility, this effectively meant that the ratio of “vaults” containing collateral being auctioned to the amount of users willing and able to buy was easily in the neighbourhood of 100-1.

This allowed some users to buy the collateral funds at near-zero prices in the absence of any actual auction participants. Although this was great for the users who decided to buy the cheap collateral, MakerDAO’s ecosystem was thrown off balance.

MakerDAO liquidation 2020: Image Source

MakerDAO liquidation 2020: Image SourceWhile Compound has had the fortune of not going through the March flash crash in its current ‘DAO’ state, the fact of the matter is that we are still very much in volatile times when it comes to both cryptocurrency markets and legacy markets.

It may very well face an issue identical to MakerDAO, where a sudden drop in price causes the collateral of borrowing users to be liquidated without enough buyers available to bring financial stability and liquidity to the protocol.

Conclusion

Despite these concerns, we believe that the Compound protocol hold some serious promise. After all, it seems that Compound is one of the rare and recent instances of a fully functioning DeFi project on par with the likes of Ren’s RenVM, which allows for decentralized, secure, and private cryptocurrency swaps between blockchains.

Furthermore, assuming the operation of the Compound protocol is actually handed over to the community, it will hopefully be able to refine the platform into something that will be used outside the fences of crypto yield farmers with a dollar-green thumb.

Make no mistake, what we are seeing is the beginning of a new era of finance. MakerDAO, Kyber Network, Uniswap, and Compound are in truth the first steps on a much longer journey to a world where finance is decentralized, transparent yet private, secure, and accessible to virtually everyone on the planet.

Here is to hoping that Bitcoin will cause people to inadvertently FOMO into the some of the most exciting technologies to date.