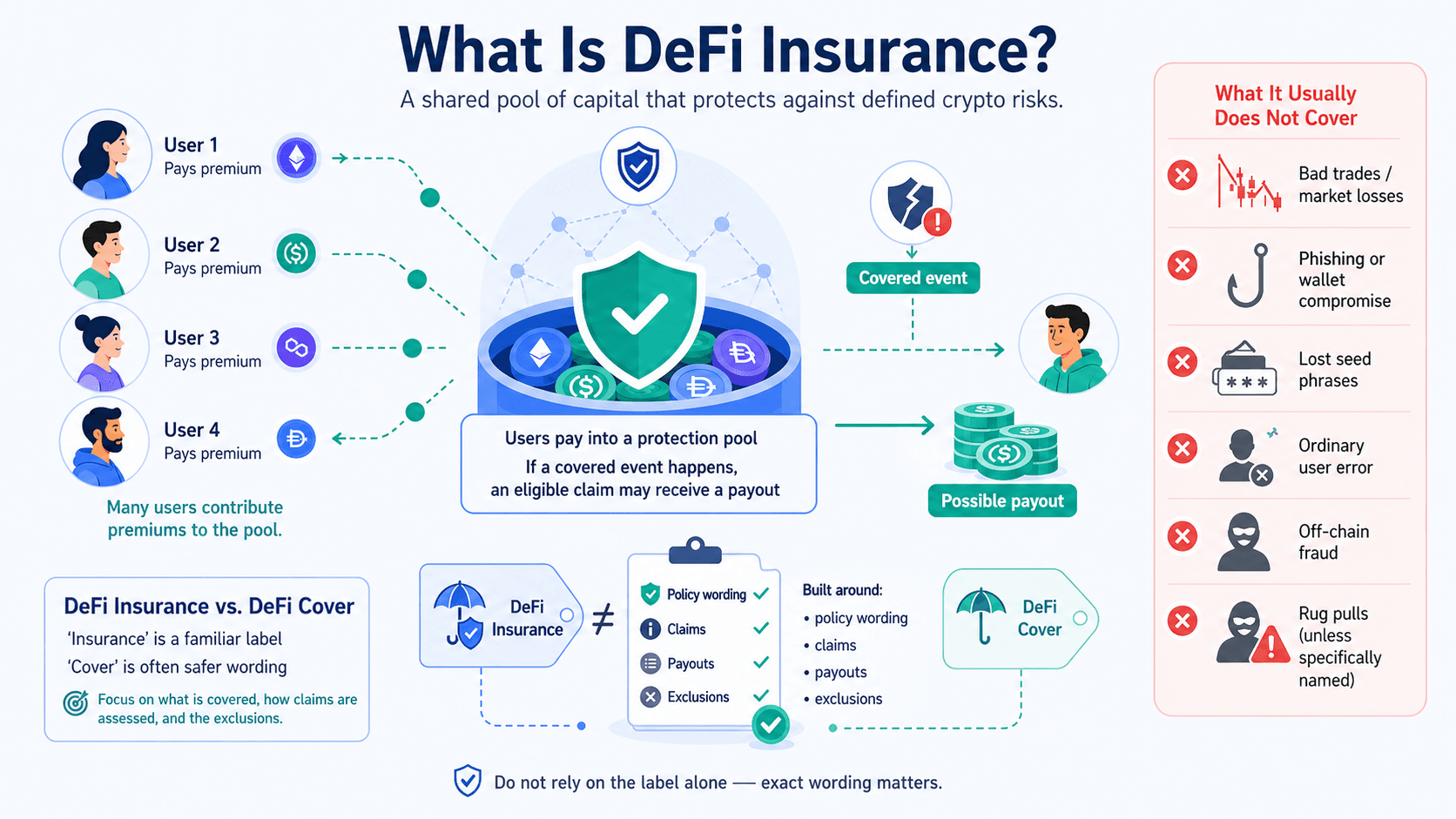

DeFi insurance is blockchain-based cover that helps protect crypto users from losses caused by smart contract exploits, protocol hacks, stablecoin depegging, and validator slashing. Because DeFi runs through code instead of traditional intermediaries, this protection is often called DeFi cover rather than insurance.

Traditional insurance usually refers to a regulated product with established policy and claims rules, while many on-chain protection products rely on shared pools, code, and community governance.

This guide is for users who hold assets in DeFi and want to understand what these products can and cannot do. The key point is simple: DeFi insurance can reduce certain technical risks, but it does not protect against bad trades, normal market losses, or every kind of wallet mistake.

Editor's Note (May 1, 2026): We fully updated this guide in May 2026 to reflect the current DeFi insurance and on-chain cover landscape. The refresh includes a clearer distinction between “DeFi insurance” and “DeFi cover,” expanded coverage of smart contract exploits, stablecoin depegging, validator slashing, bridge risk, oracle risk, and liquidity provision risk, plus updated provider sections for Nexus Mutual, InsurAce, OpenCover, Etherisc, and Subsea. We also added real-world claims examples, pricing context, policy exclusions, and a stronger risk-management framework so readers can better understand what DeFi cover can and cannot protect against.

What Is DeFi Insurance?

DeFi insurance is a way to transfer a defined crypto risk to a shared pool of capital. In plain English, it works like a group safety fund: many users pay for protection, and if a covered event happens, an eligible claimant can request a payout from that pool. Like any other risk product, it is built around policy wording, claims, payouts, and exclusions rather than blanket protection from every possible loss.

DeFi Insurance is a Way to Transfer a Defined Crypto Risk to a Shared Pool of Capital

DeFi Insurance is a Way to Transfer a Defined Crypto Risk to a Shared Pool of CapitalDeFi Insurance vs. DeFi Cover

The phrase DeFi insurance is widely used because it is familiar to readers, but DeFi cover is often the safer description. That is because the word insurance usually suggests a regulated legal product, while crypto users may have more limited legal or consumer protection depending on the structure of the product and the jurisdiction involved. The practical takeaway is simple: do not rely on the label alone. Focus on what event is covered, how claims are assessed, and what the exclusions say.

What DeFi Insurance Usually Does Not Cover

As a rule, users should not assume cover for:

- Bad trades or normal market losses

- Phishing or wallet compromise

- Lost seed phrases

- Ordinary user error

- Off-chain fraud

- Rug pulls unless specifically named

Think of it like phone insurance: a manufacturing fault may be covered, but dropping the phone in a lake may not be. That is why the exact wording matters.

DeFi Insurance vs. Traditional Insurance

At a high level, traditional insurance is usually issued by a licensed insurer under a legal contract and supervised by insurance regulators, while DeFi insurance is typically arranged through smart contracts, blockchain-based pools, or DAO-style governance. That difference affects how claims are reviewed, how transparent the system is, and what kind of legal protection a user may have.

Smart contracts can enforce rules automatically, while DAOs can use member or token-holder voting to make decisions. Traditional insurance, by contrast, sits inside a regulated framework built around licensing, solvency oversight, and consumer protection.

Let's break it down:

Feature | DeFi Insurance | Traditional Insurance |

|---|---|---|

Provider model | Protocol, DAO, or on-chain pool | Licensed insurer |

Claims process | Code, assessors, or community vote | Manual claims adjustment |

Transparency | Often publicly visible on-chain | Mostly private |

Coverage focus | Crypto-native risks | Property, health, life, liability |

Governance | Token holders or members | Corporate and regulated entities |

Legal recourse | Often more limited | Usually stronger contractual protection |

Payout speed | Can be faster | Often slower |

Premiums | Market-driven | Actuarial and regulated |

In short, DeFi cover can be faster and more transparent, but traditional insurance usually offers clearer legal backing and stronger consumer safeguards.

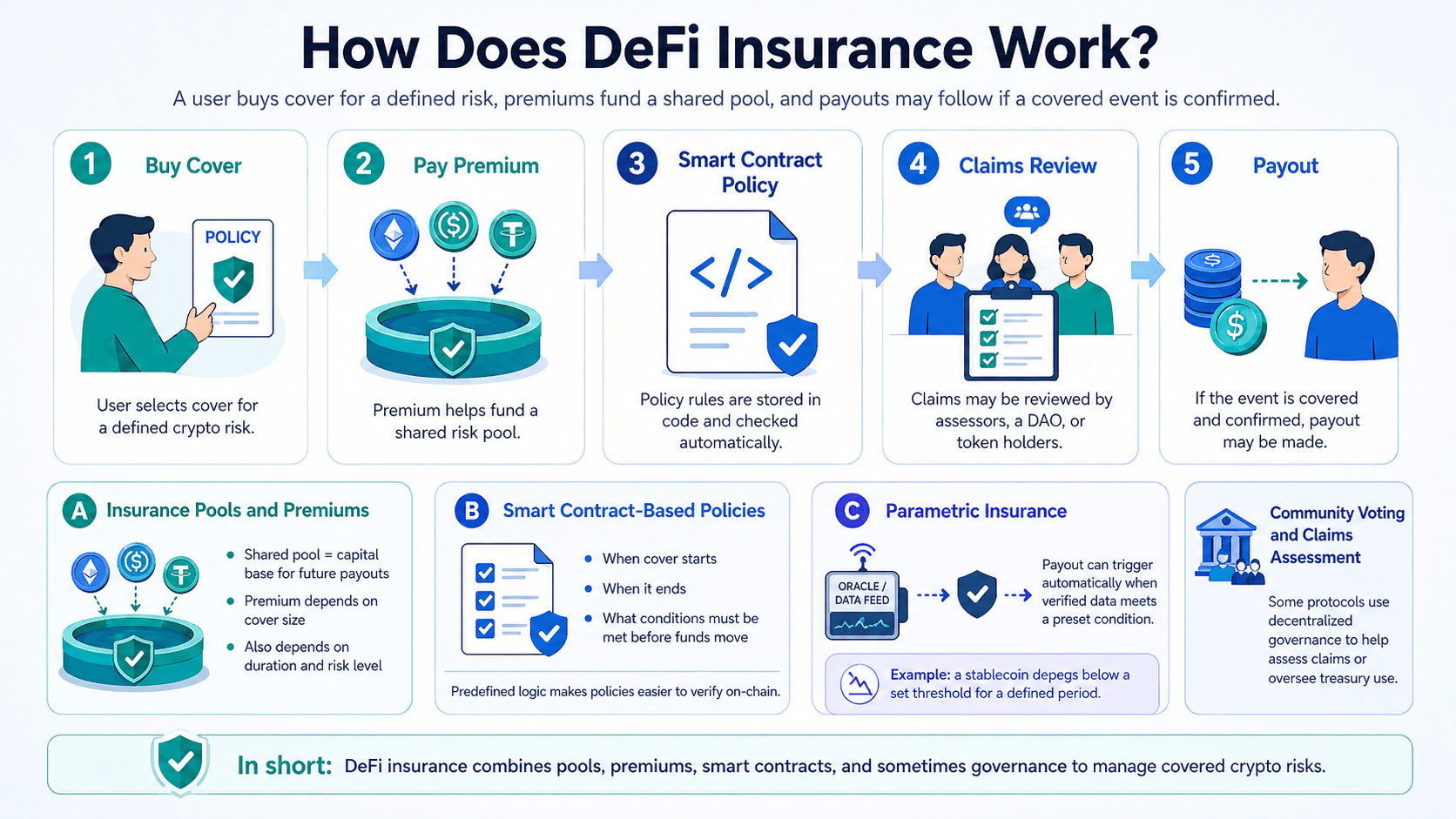

How Does DeFi Insurance Work?

At a basic level, DeFi insurance follows a simple flow: a user buys cover for a defined risk, that payment helps fund a shared pool, and a payout may be made if a covered event is later confirmed. Because these products are built with smart contracts, parts of the process can run automatically according to code rather than relying entirely on manual administration.

Most DeFi Cover Starts with a Risk Pool

Most DeFi Cover Starts with a Risk PoolInsurance Pools and Premiums

Most DeFi cover starts with a risk pool. Users pay a premium for a set amount of protection and a fixed coverage period, while the pool acts as the capital base that may fund future payouts. You can think of it like a neighborhood emergency fund: many people contribute, but only those who suffer a covered loss draw from it. Premiums usually vary with the size of the cover, the duration, and how risky the insured activity appears to be.

Smart Contract-Based Policies

A smart contract can store the policy rules, such as:

When cover starts

When it ends

What conditions must be met before funds move.

Since smart contracts follow predefined logic, they can make the process more consistent and easier to verify on-chain.

Community Voting and Claims Assessment

Some DeFi systems also use DAOs or other decentralized governance models, where members or token holders help review proposals and decisions. In insurance-like products, that governance layer may be involved in evaluating claims or overseeing how treasury funds are used.

Parametric Insurance: Automated Payouts Without Manual Claims

Parametric insurance works differently. Instead of investigating every claim in a traditional way, it pays when a predefined event is verified by data. That data often comes through oracles, which connect smart contracts to outside information. A simple example is a policy that pays automatically if a stablecoin falls below a set threshold for a defined period.

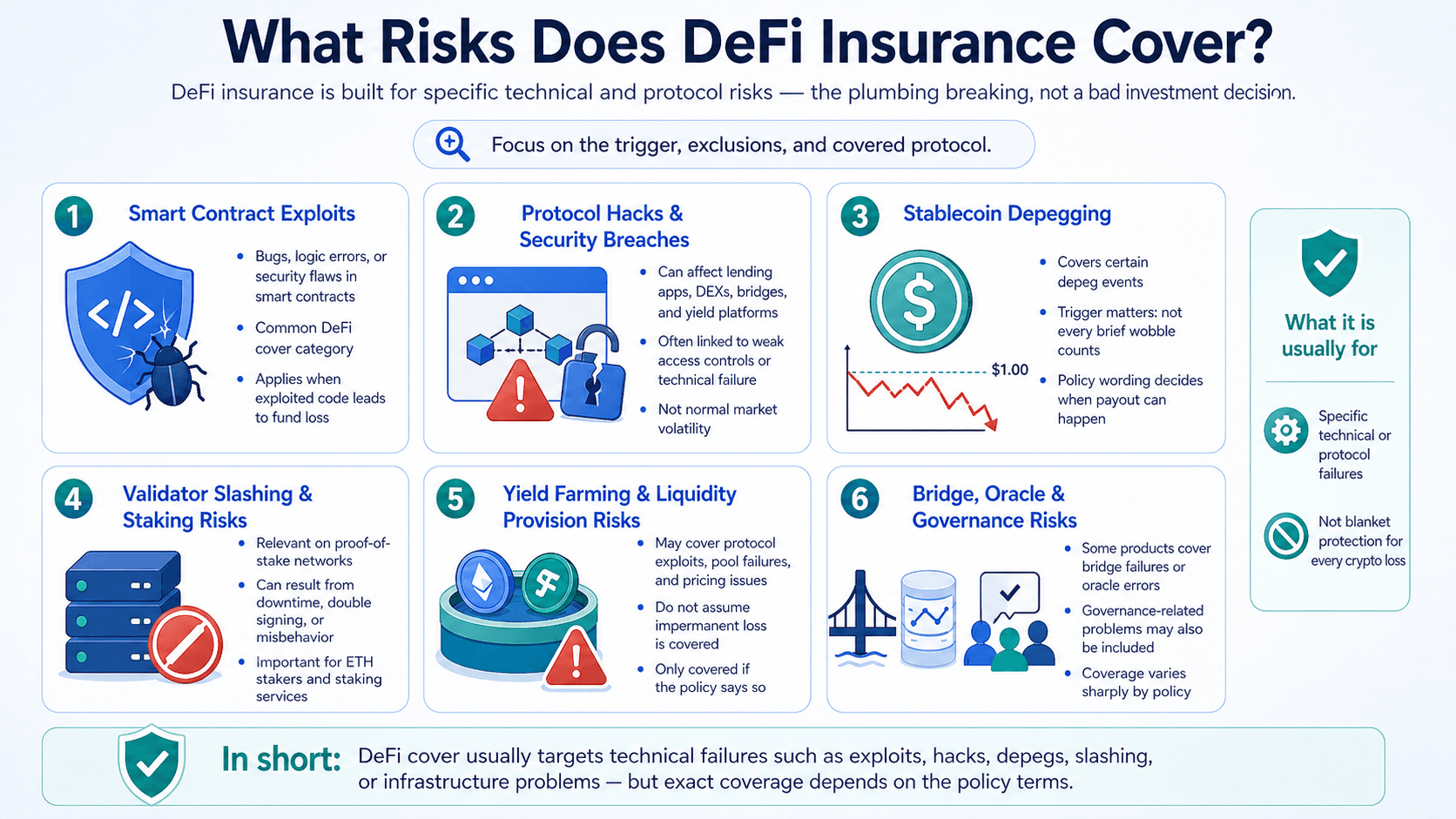

What Risks Does DeFi Insurance Cover?

DeFi insurance is usually designed for specific technical or protocol risks, not for every loss a crypto user might face. The easiest way to think about it is this: it is meant to protect against the plumbing breaking, not against a bad investment decision. That is why the exact trigger, exclusions, and covered protocol matter so much.

DeFi Insurance is usually Designed for Specific Technical or Protocol Risks, not for every Loss a Crypto User might Face

DeFi Insurance is usually Designed for Specific Technical or Protocol Risks, not for every Loss a Crypto User might FaceSmart Contract Exploits

Many DeFi applications run on smart contracts, and those contracts can contain bugs, logic errors, or security flaws. If an attacker exploits that code and funds are lost, this is one of the most common risks that DeFi cover is built around. The need for strong smart contract security is a reminder that code can fail just like any other software.

Protocol Hacks and Security Breaches

Cover may also apply to hacks affecting lending protocols, DEXs, bridges, and yield platforms. In practice, these incidents often still trace back to contract weaknesses, poor access controls, or other technical failures rather than normal market volatility.

Stablecoin Depegging

A stablecoin depeg happens when a coin that is meant to track a reference asset, such as the US dollar, loses that price stability. Some policies cover this, but the trigger matters a lot, because not every temporary price wobble counts as a covered event.

Validator Slashing and Staking Risks

On proof-of-stake networks, validators can be penalized for downtime, double signing, or other forms of misbehavior. That makes validator slashing a real risk for ETH stakers, staking services, and some liquid staking users.

Yield Farming and Liquidity Provision Risks

Liquidity providers face protocol exploits, pool failures, and pricing issues. They may also face impermanent loss, which is a normal AMM risk when token prices move. Importantly, users should not assume impermanent loss is covered unless the policy clearly says so.

Bridge, Oracle, and Governance Risks

Some products also extend to bridge failures, oracle errors, or governance-related problems in DAO systems. These are more specialized risks, and coverage can vary sharply from one policy to another.

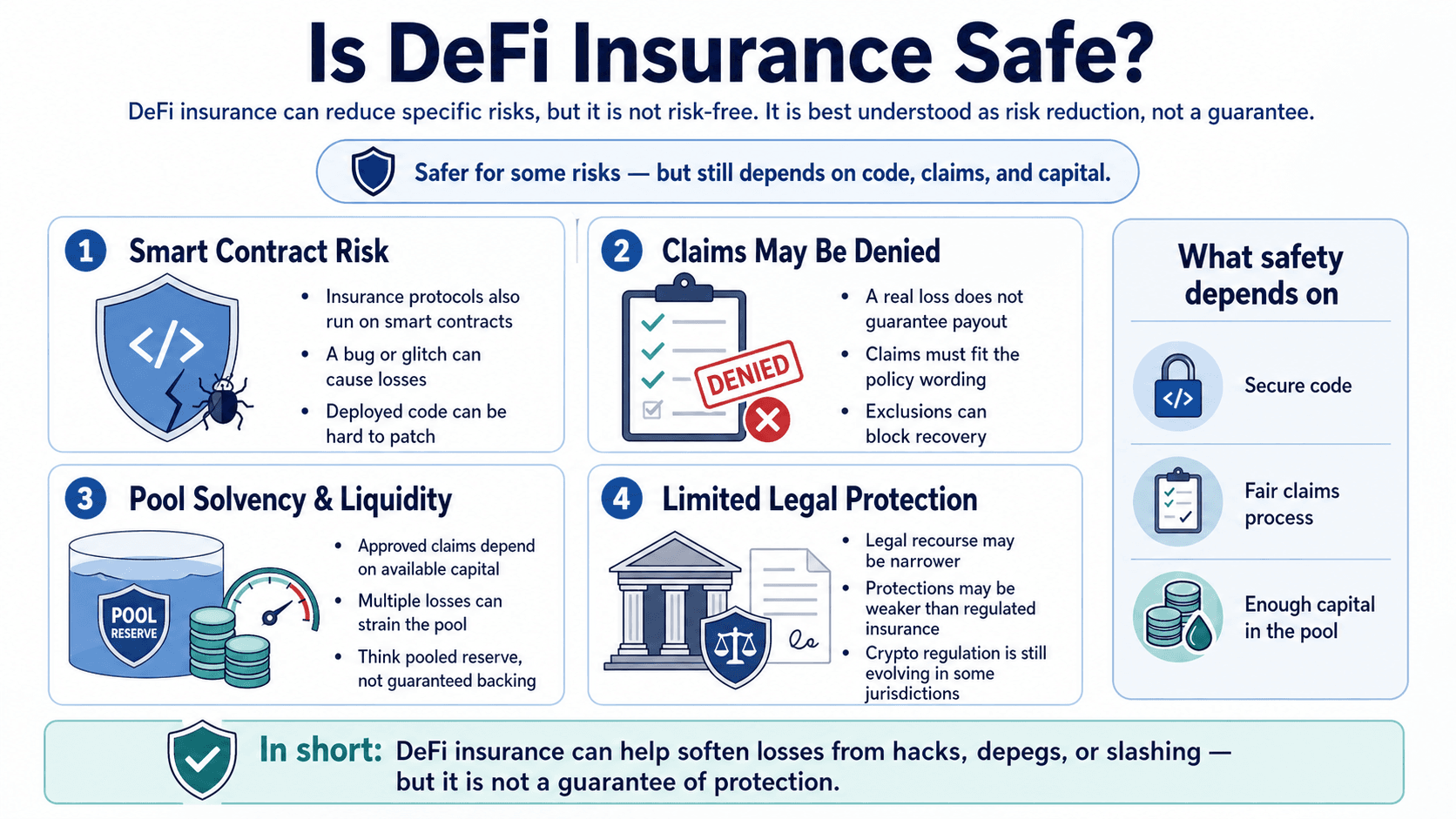

Is DeFi Insurance Safe?

DeFi insurance can reduce specific DeFi risks, but it is not risk-free. A policy may help soften the impact of a hack, depeg, or slashing event, yet users still depend on the security of the code, the fairness of the claims process, and the amount of capital available in the pool. In other words, it is better viewed as risk reduction, not a guarantee.

DeFi Insurance can Reduce Specific DeFi Risks, but it is not Risk-Free

DeFi Insurance can Reduce Specific DeFi Risks, but it is not Risk-FreeSmart Contract Risk in Insurance Protocols

The first risk is the insurance protocol itself. DeFi products run on smart contracts, and that deployed code can be hard to patch and that losses from smart contract defects have been significant; all coming down to a simple bug or glitch.

Claims May Be Denied

Even when a loss is real, a payout is not automatic. In insurance terms, a claim is only payable when the loss is covered under the policy agreement, which is why wording and exclusions matter so much.

Pool Solvency and Liquidity Risk

Users also rely on the pool having enough capital to meet approved claims. If many losses hit at once, available liquidity becomes part of the safety picture. This is less like a government-backed guarantee and more like a pooled reserve.

Limited Legal Protection

Legal protection may also be narrower than with regulated insurance. For example, the UK’s dedicated cryptoasset regime is still being rolled out, which shows that crypto products do not always sit inside the same mature regulatory framework as traditional insurance.

Benefits of DeFi Insurance

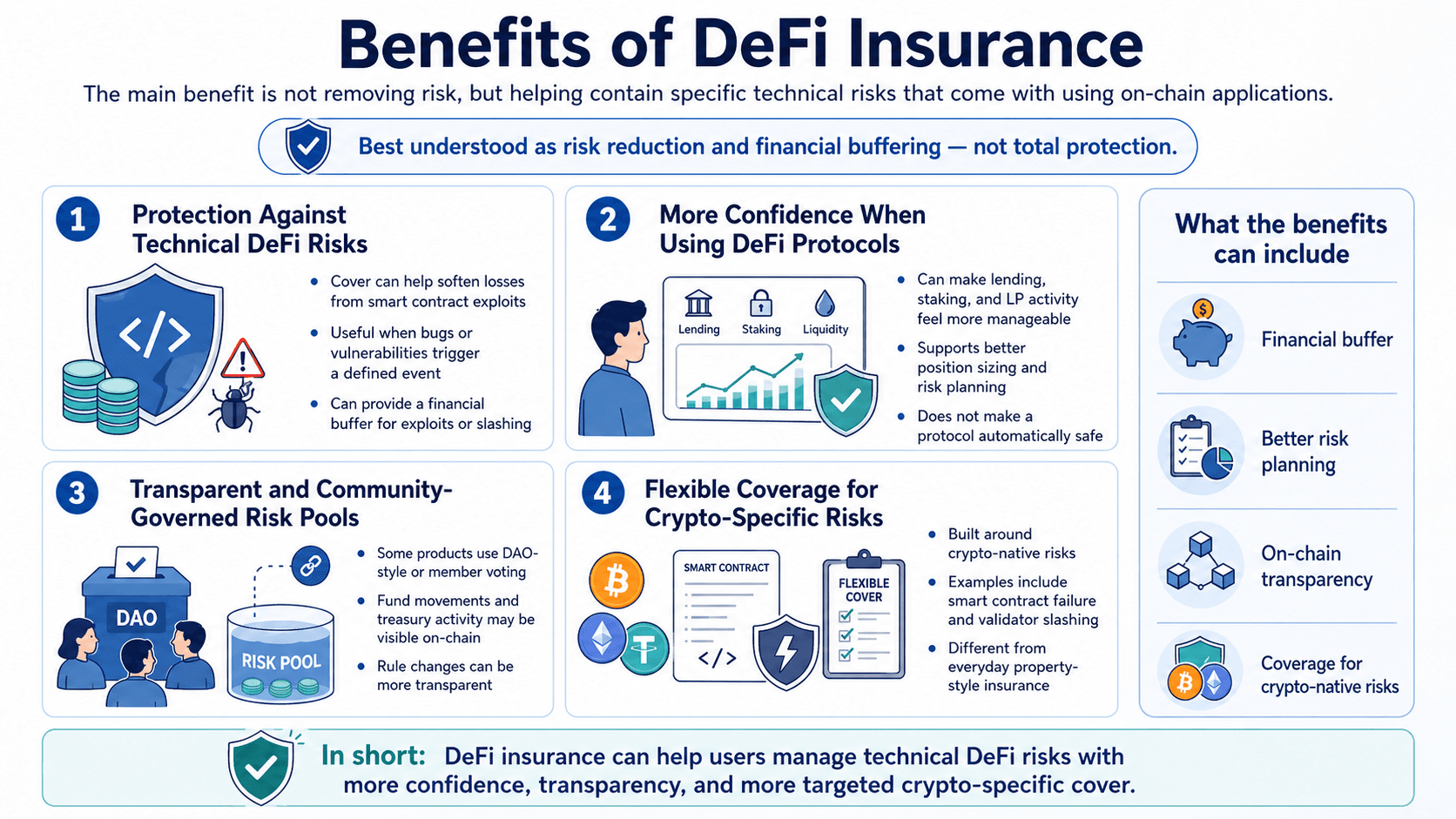

The main benefit of DeFi insurance is not that it removes risk, but that it can help contain some of the technical risks that come with using on-chain applications.

DeFi Insurance does not Remove Risk, but it can Help Contain some of the Technical Risks

DeFi Insurance does not Remove Risk, but it can Help Contain some of the Technical RisksProtection Against Technical DeFi Risks

Smart contract security is serious because bugs and vulnerabilities can lead to major losses. For users exposed to contract exploits or slashing, cover can act as a financial buffer when a defined event occurs.

More Confidence When Using DeFi Protocols

Knowing that one specific risk has been covered can make lending, staking, or liquidity provision feel more manageable. It does not make a protocol safe, but it can help users approach position sizing and risk planning more carefully.

Transparent and Community-Governed Risk Pools

Where a product uses DAO-style governance, key decisions can be made by member voting rather than a single company. That can make decentralized capital pools more transparent, because fund movements, treasury activity, and rule changes may be visible on-chain.

Flexible Coverage for Crypto-Specific Risks

DeFi cover can also be useful because it is built around crypto-native risks, such as smart contract failure or validator slashing, rather than everyday risks like damage to property.

Best DeFi Insurance Platforms in 2026

The best DeFi insurance platforms in 2026 depend on the type of risk you want to cover. Some are stronger on protocol cover, others on stablecoin depeg cover, ETH slashing cover, or parametric insurance.

Platform | Best For | Main Coverage Types | Governance / Claims Model |

|---|---|---|---|

Nexus Mutual | Broad DeFi cover | Protocol cover, custody cover, depeg cover, ETH slashing cover | Member-based mutual, NXM |

Multi-chain users | Smart contract cover, stablecoin depeg cover, slashing cover, bridge cover | DAO-style governance with advisory review | |

OpenCover | Comparing on-chain cover products | Protocol cover, depeg cover, multi-protocol risk | Coverage marketplace / underwritten products |

Etherisc | Parametric insurance | Flight delay, crop, weather, depeg-related products | Smart contract and oracle-based models |

Risk Harbor | Automated DeFi protection | Stablecoin and yield-token style protection | Algorithmic / parametric claims model |

Nexus Mutual

- One of the earliest and best-known DeFi cover platforms, with official governance docs describing it as an onchain discretionary mutual governed by its members.

- Uses the NXM token for governance, staking, and underwriting.

- It lists protection for smart contract hacks, custody failure, slashing, and depeg.

- Best for users who want broad and relatively established DeFi cover.

InsurAce

- A practical choice for multi-chain users, because its buy-cover guide lists support across multiple chains and risk types.

- Its cover product docs include smart contract cover, while separate pages cover stablecoin depeg, Ethereum slashing, and bridge cover.

- Its claims materials show an Advisory Board and Claim Assessors participating in investigation, voting, appeals, and payout decisions.

OpenCover

- Best understood as a coverage marketplace rather than a single insurer-like protocol.

- Users can get cover against smart contract hacks, stablecoin depegs, and more from vetted onchain underwriters.

- Best for users who want a more structured way to compare on-chain cover products.

Etherisc

- A useful example of parametric insurance, built around the Generic Insurance Framework.

- Its official materials highlight flight delay, crop, and weather-related products, while its docs explain that parametric cover uses predefined events and deterministic payouts.

- Best for users who want to understand how automated insurance can work beyond core DeFi protocol hacks.

Subsea (formerly Risk Harbor)

- Known for an automated claims model. It is now rebranded to Subsea, which describes a risk-management marketplace built around instant payouts and objective, transparent event assessments.

- The current OpenCover profile for Risk Harbor still describes stablecoin depeg cover and yield token cover, with claims assessed automatically using on-chain data.

- Best for users interested in faster, rule-based, parametric-style DeFi protection, though its present market status is less straightforward than some of the larger names above.

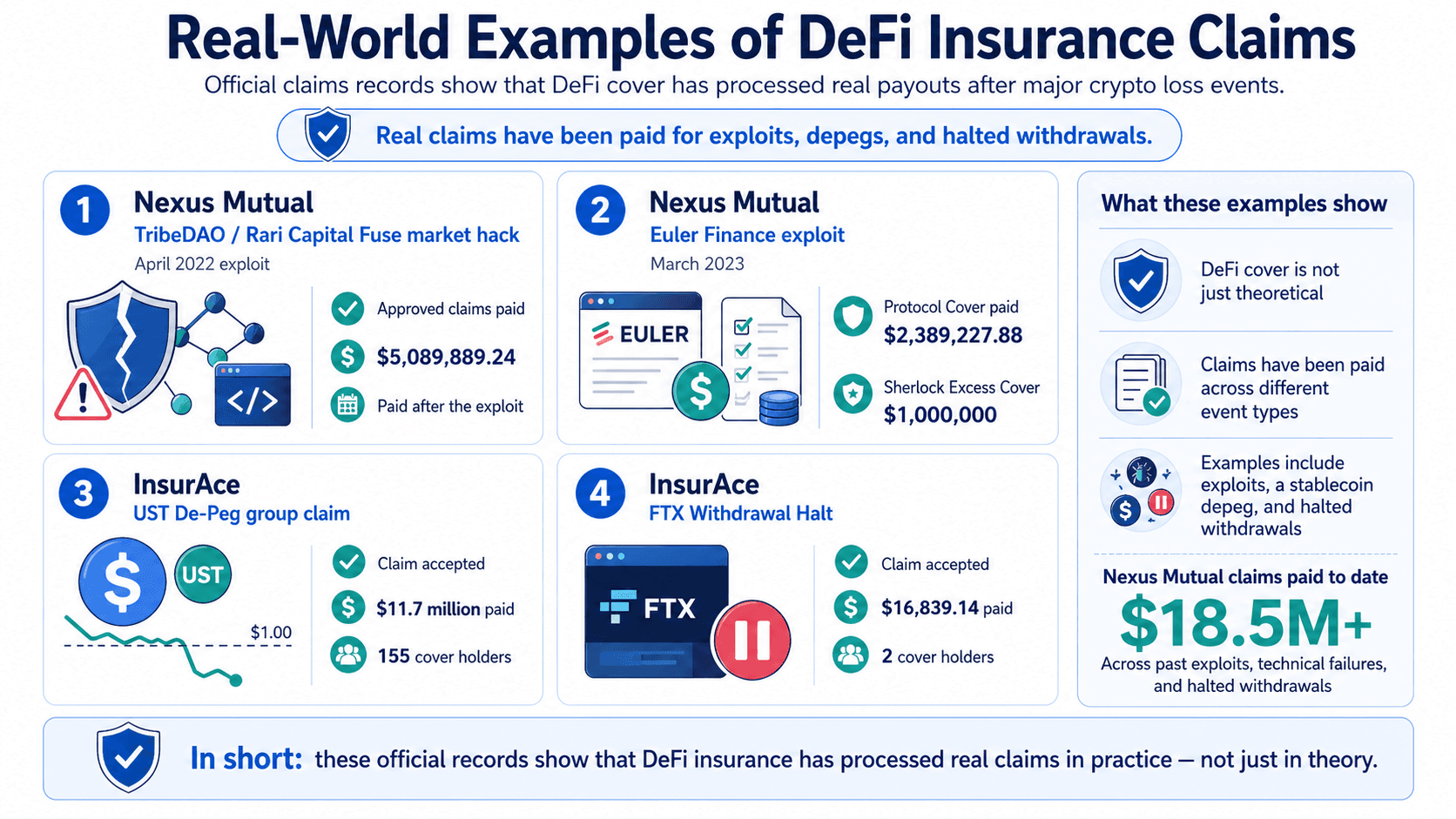

Real-World Examples of DeFi Insurance Claims

DeFi insurance claims are not just theoretical. Official claims records show that some cover products have paid out after major crypto loss events, which is useful because it proves the model can work in practice.

Official Claims Records Show that some Cover Products have Paid out after Major Crypto Loss Events

Official Claims Records Show that some Cover Products have Paid out after Major Crypto Loss Events- In the TribeDAO / Rari Capital Fuse market hack claims history, Nexus Mutual says a total of $5,089,889.24 was paid out for approved claims after the April 2022 exploit.

- In the Euler Finance exploit claims history, Nexus Mutual says $2,389,227.88 was paid for approved Euler Finance Protocol Cover claims, plus $1 million for an approved Sherlock Excess Cover claim linked to the same event.

- On its official Claim Records page, InsurAce says the UST De-Peg group claim was accepted, with $11.7 million paid to 155 cover holders. The same page says the FTX Withdrawal Halt claim was also accepted, with $16,839.14 paid to 2 cover holders.

- More broadly, Nexus Mutual’s claims history overview says members have paid out more than $18.5 million to cover holders across past exploits, technical failures, and halted withdrawals.

Taken together, these examples show that DeFi cover has processed real claims across different types of crypto failures, including a stablecoin depeg, a withdrawal halt, and a protocol exploit.

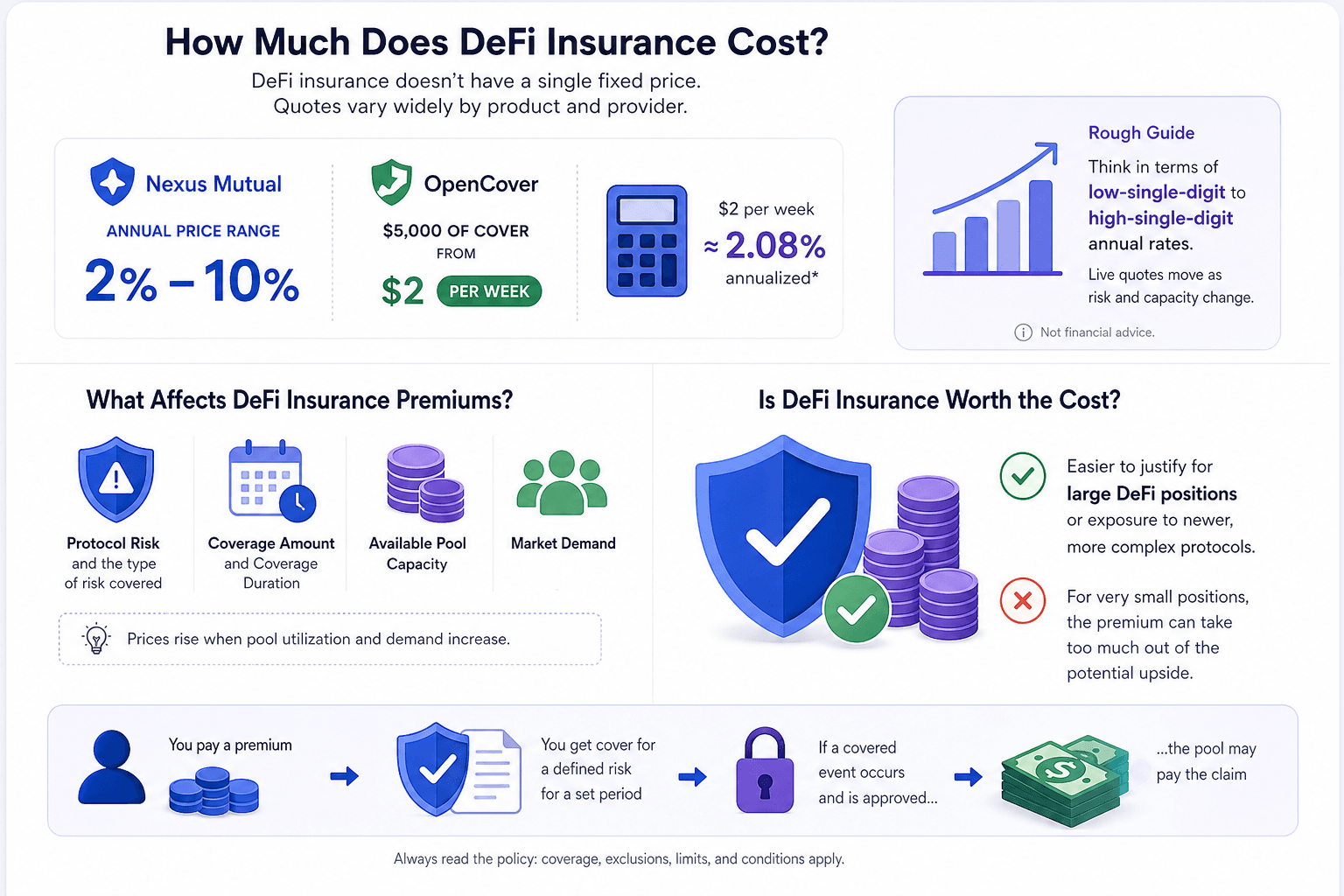

How Much Does DeFi Insurance Cost?

DeFi insurance does not have a single fixed price. Official pricing pages show that quotes can vary widely by product and provider.

DeFi Insurance does not have a Single Fixed Price

DeFi Insurance does not have a Single Fixed PriceFor example, Nexus Mutual’s cover-buyer docs list annual prices between 2% and 10%, while OpenCover advertises $5,000 of cover from $2 per week, which works out to about 2.08% annualized at that example price. As a rough guide, users can think in terms of low-single-digit to high-single-digit annual rates, with live quotes moving as risk and capacity change.

What Affects DeFi Insurance Premiums?

Pricing usually moves with:

- Protocol risk and the type of risk covered

- Coverage amount and coverage duration

- Available pool capacity

- Market demand

For example, Nexus Mutual’s pricing docs say cover prices rise when pool utilization and demand increase, while InsurAce’s buy-cover flow shows that the quote also depends on the amount and period selected.

Is DeFi Insurance Worth the Cost?

Cover is often easier to justify for large DeFi positions or exposure to newer, more complex protocols. For very small positions, the premium can take too much out of the potential upside.

Do I Need DeFi Insurance?

Not every crypto user needs DeFi insurance. It is most relevant when losses could come from smart contract failures, stablecoin depegs, validator slashing, or bridge problems rather than normal market swings.

DeFi Insurance May Make Sense If…

- You keep meaningful funds in DeFi protocols and could not comfortably absorb a total loss.

- You use lending, staking, bridges, or yield-bearing strategies.

- You hold stablecoins that could depeg, or stake ETH where slashing is a real risk.

DeFi Insurance May Not Be Necessary If…

- You mainly hold assets in self-custody and are not using DeFi protocols.

- Your positions are small enough that premiums may outweigh the benefit.

- Your main risk is market volatility, not protocol failure.

- The policy excludes the exact event you care about.

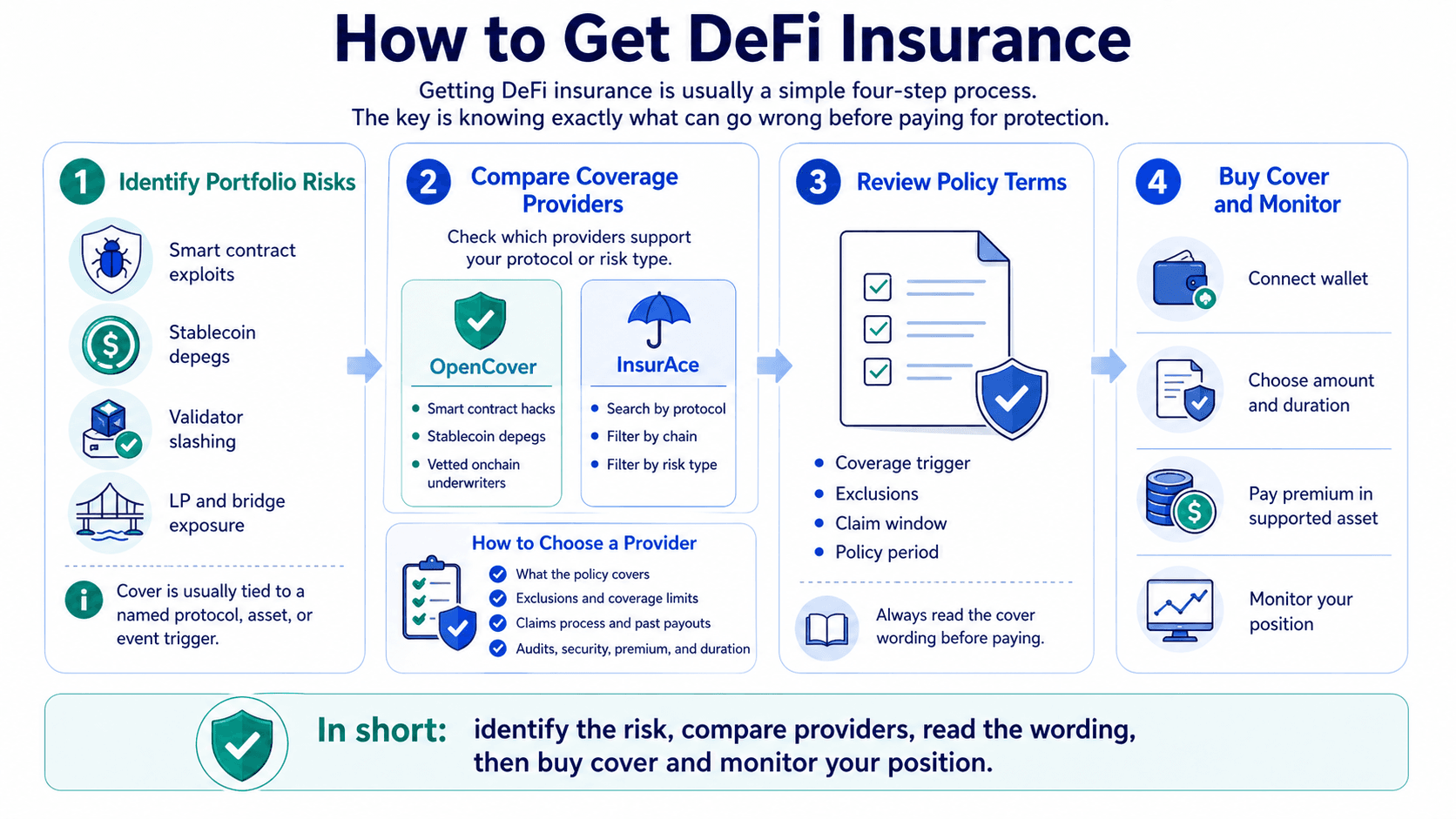

How to Get DeFi Insurance

Getting DeFi insurance is usually a simple four-step process. The process is not very different from buying travel insurance: the key is knowing exactly what can go wrong before paying for protection.

Getting DeFi Insurance is Usually a Simple Four-Step Process

Getting DeFi Insurance is Usually a Simple Four-Step ProcessStep 1: Identify the DeFi Risks in Your Portfolio

Start by listing where losses could come from. For most users, that means exposure to smart contract exploits, stablecoin depegs, validator slashing, LP positions, and bridge use. This step matters because DeFi cover is usually tied to a named protocol, asset, or event trigger.

Step 2: Compare Coverage Providers

Next, compare which providers actually support the protocol or risk in question. As we mentioned earlier, OpenCover users can get protection against smart contract hacks, stablecoin depegs, and more from vetted onchain underwriters, while InsurAce’s buy-cover guide shows users searching and filtering by protocol, chain, and risk type.

Step 3: Review Policy Terms Before Buying

Always read the cover wording. Users should check the coverage trigger, exclusions, claim window, and policy period before paying.

Step 4: Buy Coverage and Monitor Your Position

Once satisfied, connect a wallet, choose the cover amount and duration, and pay the premium in the supported asset.

How to Choose a DeFi Insurance Provider

Before buying, check:

- What the policy actually covers,

- The exclusions and coverage limits,

- The claims process and past payouts,

- Audits, security, premium, and duration.

Final Thoughts: Is DeFi Insurance Worth It in 2026?

For many users, DeFi insurance is worth considering in 2026, but only with realistic expectations. It can help reduce exposure to specific risks such as smart contract exploits, stablecoin depegs, and validator slashing. What it does not do is protect against every crypto loss, every bad trade, or every policy dispute.

That makes DeFi cover less like a magic shield and more like an extra layer of risk management for users with meaningful capital in DeFi. It is often most useful for larger positions, newer protocols, or strategies with several technical points of failure.

Before buying, users should compare coverage terms, claims history, and exclusions carefully. The goal is not to eliminate risk altogether, but to understand which risks are being transferred and which ones still stay on the user.