Years Operating

Since 2018.

You open a crypto app, tap “Earn,” and suddenly your idle coins are working for you. That’s the promise, and it’s a tempting one. But the real question isn’t whether the interface looks polished or the rates look attractive. It’s whether you understand what’s happening behind the scenes when you deposit, borrow, or try to withdraw during a stressful market move.

Nexo sits in that familiar CeFi middle ground: more convenient than self custody, less protected than traditional finance. So “Is Nexo safe?” is really shorthand for a few sharper questions: Who holds the keys? What happens if markets move fast? What protections exist if something breaks, gets frozen, or simply goes quiet? This guide breaks those questions down into plain English, so you can separate strong safeguards from comforting assumptions.

This section explains how the Nexo Safety Score is built, which categories matter most, and what kinds of evidence can move the score up or down.

A 4.7 out of 5 reflects a platform with meaningful security controls and some transparency, but with unavoidable CeFi risks that users cannot “turn off,” especially counterparty risk and regulatory access risk. This score is a structured risk snapshot, not a guarantee, and it is not comparable to bank style protections such as FDIC insurance.

Category | Weight | What we look at |

|---|---|---|

Security infrastructure | 25% | Custody stack such as Ledger and Fireblocks, account controls, security programs. |

Regulatory compliance | 20% | Jurisdiction specific licenses and registrations and major regulatory outcomes such as the SEC settlement. |

Financial stability and counterparty risk | 20% | Collateral model framing in the business model, plus what remains unverified about balance sheet and counterparties. |

User protection | 15% | Controls such as whitelisting and practical safety features users can enable. |

Technical reliability | 10% | Incident visibility through the status page and user reported patterns on Trustpilot. |

Transparency | 10% | Reserves attestation framework and clarity of disclosures such as insurance. |

This review treats “safe” as a checklist: Where funds sit, how accounts are protected, what regulators say, and how the platform behaves under stress.

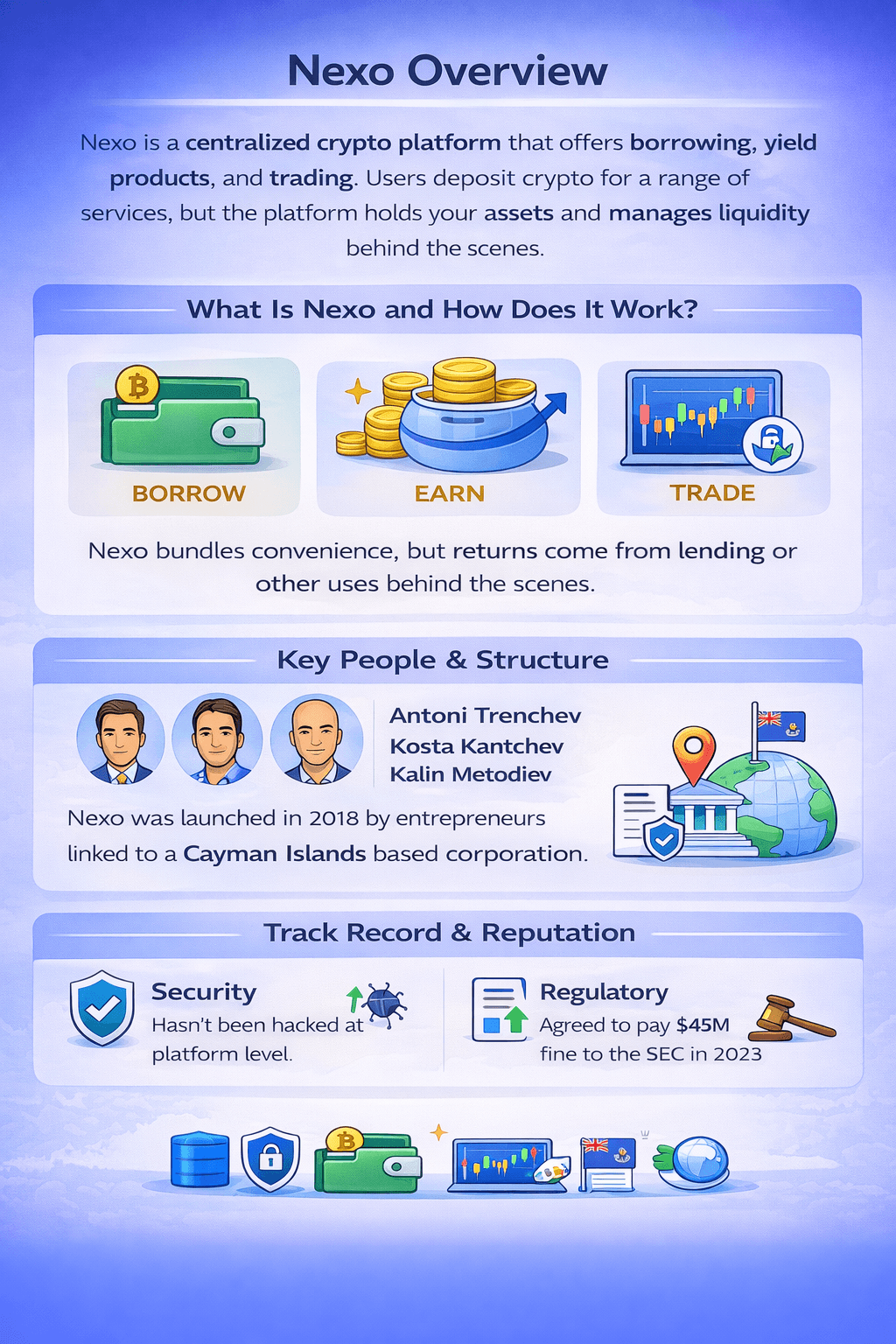

Nexo is a centralized crypto platform that bundles yield-style accounts, crypto-backed borrowing, and trading. That convenience can be useful, but it also changes the risk profile: instead of holding your own keys, you rely on the platform’s custody setup, liquidity management, and the legal protections that apply in your region.

Nexo is a Centralized Crypto Platform that Bundles Yield-Style Accounts, Crypto-backed Borrowing, and Trading

Nexo is a Centralized Crypto Platform that Bundles Yield-Style Accounts, Crypto-backed Borrowing, and TradingNexo launched in 2018 and offers crypto-backed borrowing through Borrow, yield-style products through Earn, and spending features via the Nexo Card. For trading, it provides an Exchange experience and a separate interface in Nexo Pro.

On centralized platforms, “yield” typically depends on how customer assets are deployed behind the scenes, such as lending and other balance-sheet activity. The practical takeaway is simple: when returns depend on counterparties, your risk is tied to the platform’s risk management, not just your personal account security.

Nexo has been publicly associated with founders and executives including Antoni Trenchev, Kosta Kantchev, and Kalin Metodiev. Corporate structure also matters because consumer protections vary by jurisdiction. Nexo has been described as a Cayman Islands corporation, which is one reason access and compliance rules can differ across major markets.

When platforms say they’ve had “no major hacks,” it helps to define terms. Here, a “major hack” means a platform-level breach impacting custody or core systems, rather than individual account takeovers caused by phishing or weak passwords.

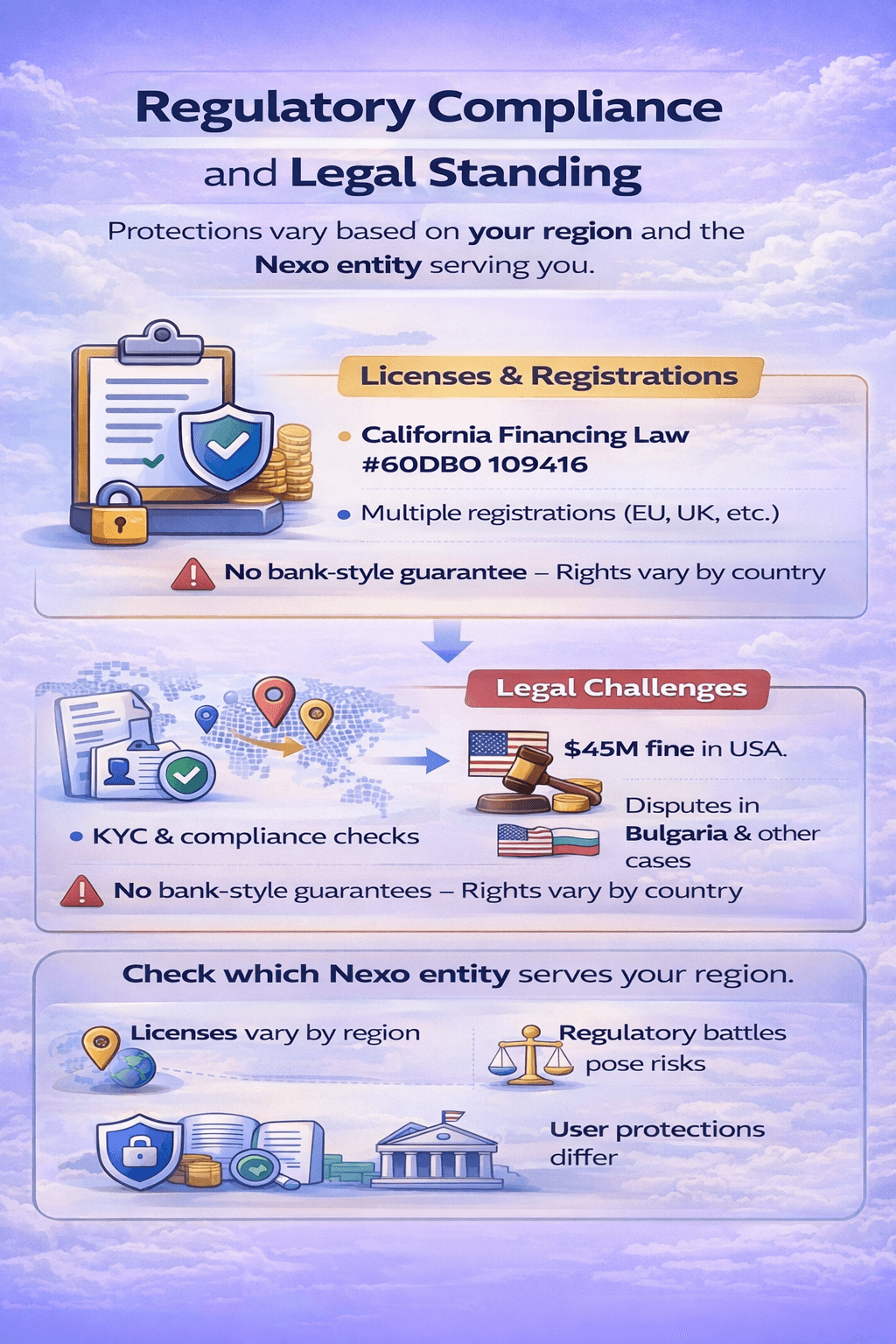

On the regulatory side, a January 2023 SEC announcement referenced in the table above, said Nexo agreed to pay $45 million and stop offering its crypto asset lending product to U.S. investors. In Europe, Bulgarian prosecutors said they closed their investigation in December 2023, citing no evidence of criminal activity.

For more, head over to our full Nexo review.

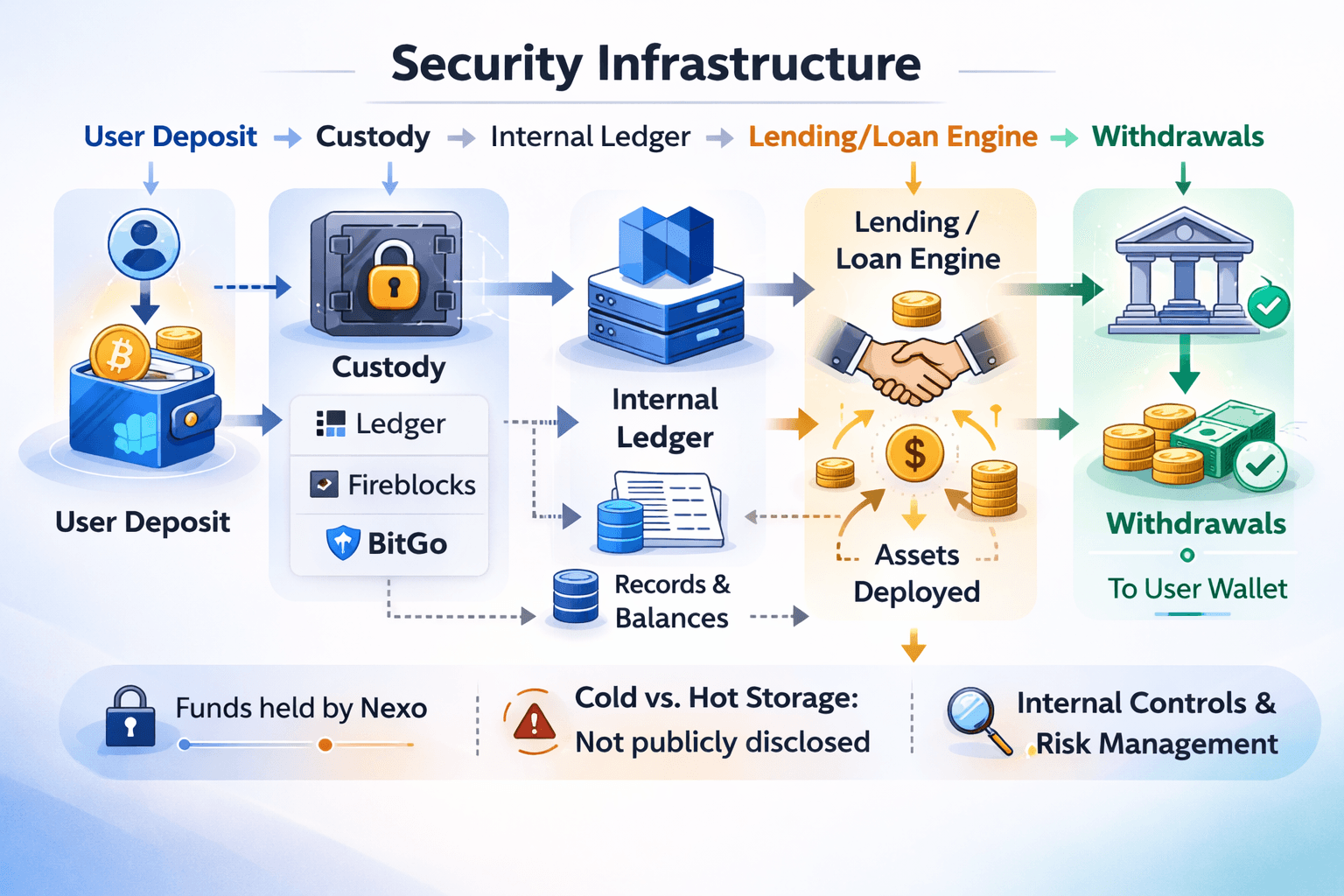

Centralized platform security is a layered system: part “vault,” part “alarm system,” and part “front-desk rules.” With Nexo, those layers include institutional custody tooling, in-app protections you can turn on, and a transparency layer that matters for platform-level risk.

Centralized Platform Security is a Layered System

Centralized Platform Security is a Layered SystemNexo lists Ledger and Fireblocks in its security stack, and it has integrations with Ledger Vault and BitGo. Nexo does not disclose a consistent cold-vs-hot storage allocation. The practical implication is simple: users can’t independently gauge how much value is kept offline versus online, so they’re trusting the platform’s overall controls and operating discipline.

Nexo supports app-based 2FA and an email anti-phishing code, and it offers address whitelisting to limit withdrawals to saved destinations. Whitelisting is like a “pre-approved payee” list at a bank: even if an attacker logs in, sending funds to a new address becomes harder. Nexo also promotes an always-on Anti-scam Engine that can flag or pause suspicious withdrawals; users can see prompts and pauses, but can’t verify how effective the detection is across edge cases.

Nexo's security page claims ISO/IEC 27001:2022 along with other security certificates. It also runs a public security disclosure program that is explicitly non-bounty. Nexo AES 256-bit SSL for data protection in transit, which is useful, but doesn’t, on its own, explain private-key storage.

Nexo has published a reserves attestation framework (referenced in the table earlier) intended to compare certain assets and liabilities. Even when available, attestations aren’t full audits and typically don’t reveal borrower quality, concentration risk, or off-platform exposures.

Nexo offers credible user-level safeguards, but the most important unknowns remain platform-level: storage allocation detail and counterparty risk that users can’t directly verify.

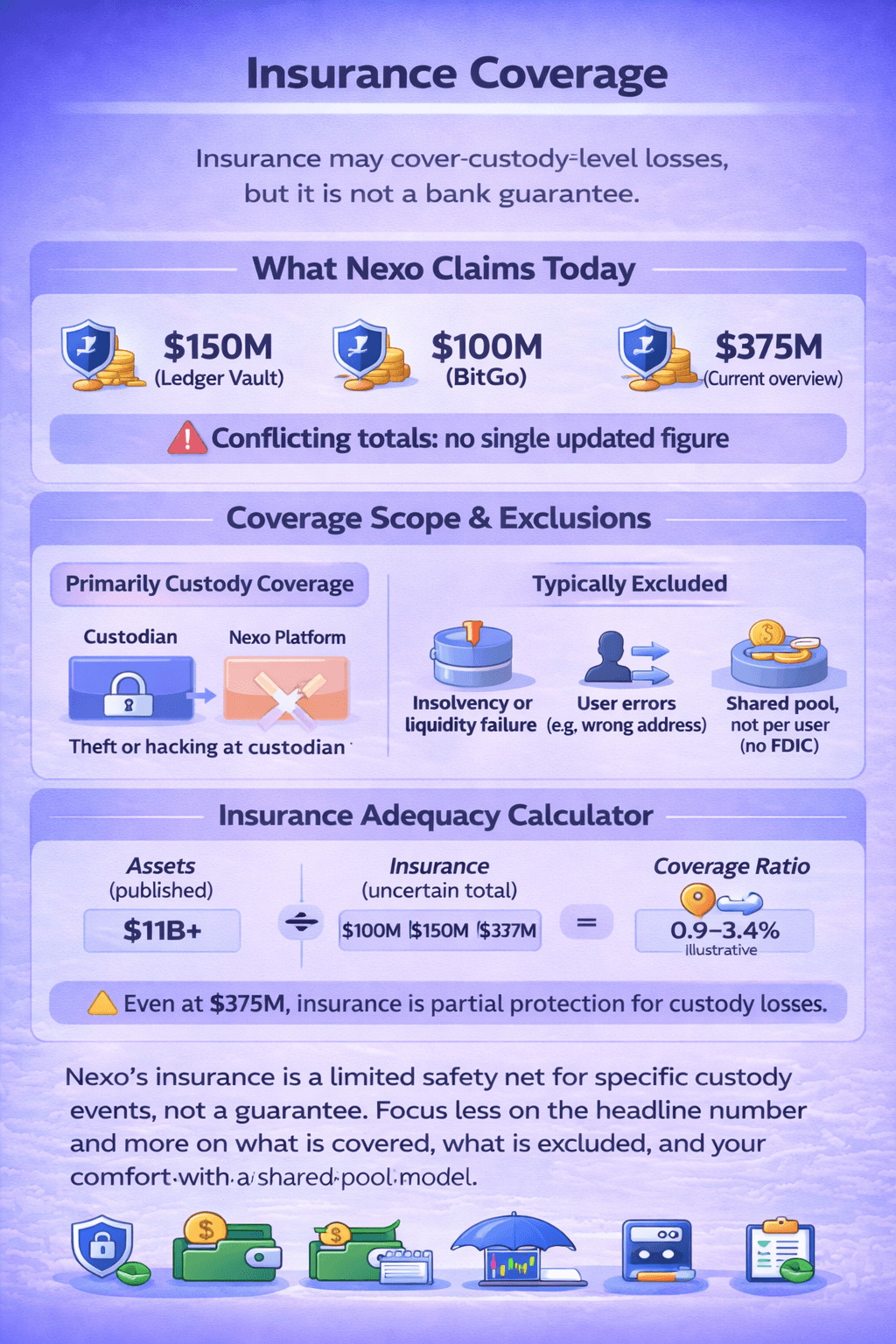

Insurance can help in a narrow set of loss scenarios, but it is not the same thing as a bank style guarantee. With Nexo, the most important question is what layer is insured and what events are actually covered.

Insurance in Crypto is not the same Thing as a Bank Style Guarantee

Insurance in Crypto is not the same Thing as a Bank Style GuaranteeA detailed insurance overview lists $375 million in coverage tied to custody arrangements. A separate post tied to the Ledger Vault integration highlights $150 million..

These figures conflict because they come from different outdated resources, different custody contexts, and there is no single consistently updated public number that reconciles them.

The insurance described for Nexo is primarily custody level coverage. That means it is designed to respond to losses at the custodian layer, not platform level losses such as insolvency or liquidity failure. In simple terms, theft or hacking at the custody layer is treated differently from insolvency risk, and user error like sending funds to the wrong address is typically outside scope. Coverage is also a shared pool, not per user protection like FDIC deposit insurance.

An $11 billion plus assets figure appears on the security page, but the insurance total is not presented as a single current, verifiable number. Even at $375 million, insurance is best viewed as partial protection for defined custody incidents, not a promise of full repayment during mass withdrawals or insolvency.

Nexo’s insurance is best treated as a limited safety net for specific custody loss events, not a guarantee that user funds are protected in every scenario. If insurance is a deciding factor, the most practical takeaway is to focus less on the headline number and more on what it actually covers, what it excludes, and how much of your exposure you are comfortable placing under a shared pool model.

Regulation is rarely one universal approval that covers every product worldwide. What matters is which Nexo entity serves your region, what registrations apply there, and what protections you actually get if something goes wrong.

Know which Nexo Entity Serves Your Region, what Registrations Apply there, and what Protections You actually Get

Know which Nexo Entity Serves Your Region, what Registrations Apply there, and what Protections You actually GetNexo holds a patchwork of registrations across jurisdictions, such as a California Financing Law license shown under 60DBO 109416, plus other market specific licenses and registrations listed on the security page. Identity verification and compliance checks are part of normal access. A license can signal oversight, but it does not guarantee bank style protections, and consumer rights vary widely by country and by product.

January 2023, SEC settlement and NASAA settlement - High Impact

July 2023, Nexo Capital Inc v Shulev - Low Impact

Cress v Nexo in the U.S. Northern District of California (ongoing) - Impact = Medium

Nexo and others v Bulgaria at ICSID (ongoing) - Impact = Medium

Sokol Iankov matter - Impact = Low, unless the posture changes

Nexo operates across multiple jurisdictions and entities, which can create regulatory gaps when products are offered globally but supervised locally. In those cases, user protections depend on the specific Nexo entity serving your region, not the strongest sounding registration elsewhere.

Recourse can be limited if disputes must be handled in a specific venue or under offshore terms, and access can change quickly if regulators impose geo restrictions or ban certain lending and yield products, as noted in the January 2023 SEC settlement.

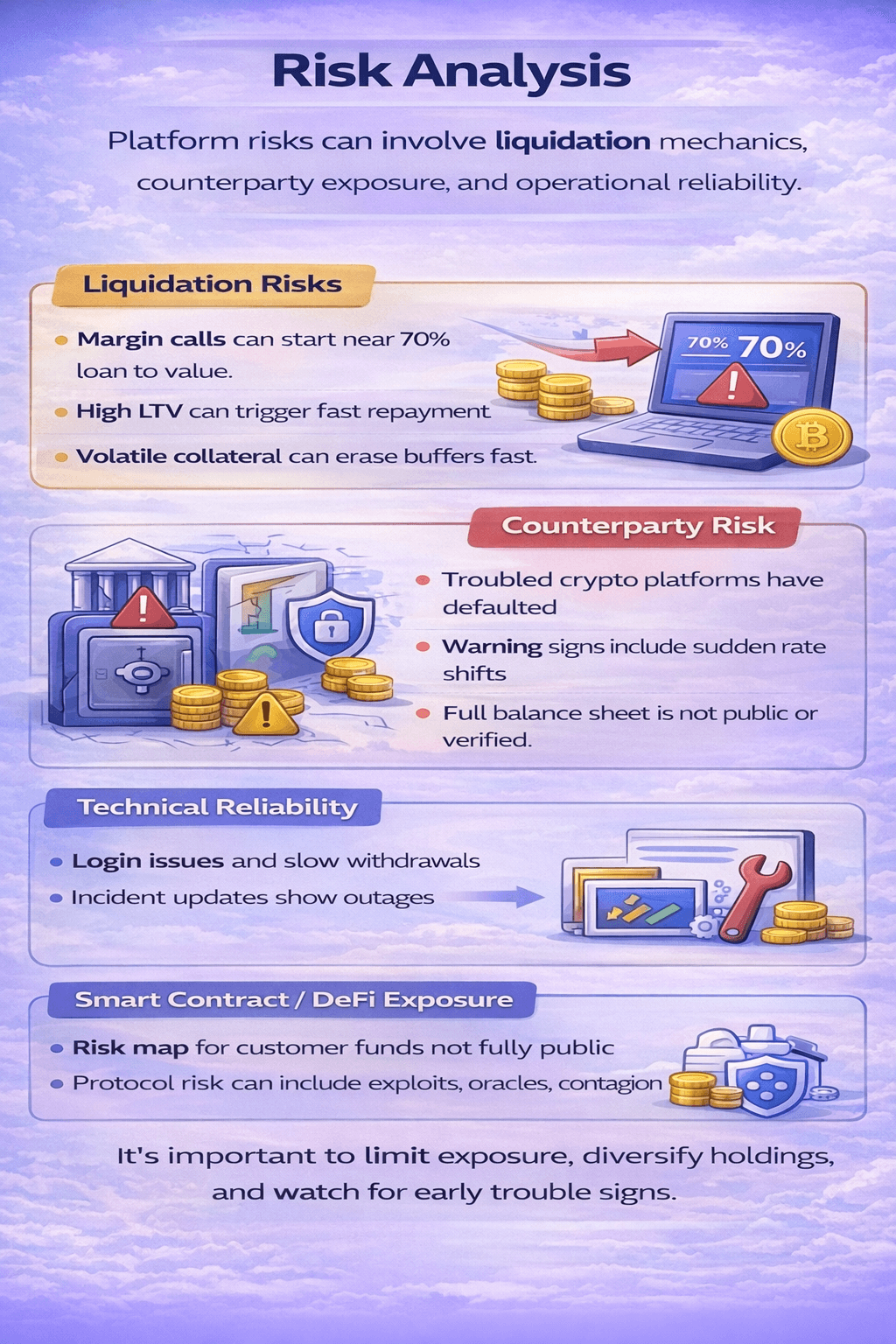

Most risks on centralized platforms fall into borrowing mechanics, platform counterparty risk, and operational reliability. Some can be managed with conservative settings and sizing. Others can only be reduced by limiting exposure.

Most Risks on Centralized Platforms Fall into Borrowing Mechanics, Platform Counterparty Risk, and Operational Reliability

Most Risks on Centralized Platforms Fall into Borrowing Mechanics, Platform Counterparty Risk, and Operational ReliabilityLiquidation risk comes down to loan to value and how fast it shifts when collateral drops.

Key mechanics:

Dated user cases often show the same pattern: borrowing near the limit leaves little time to react. A practical rule is to keep a wide buffer and treat maximum LTV as a ceiling, not a target.

Counterparty risk is the risk that a platform cannot meet obligations because assets are impaired, tied up, or mismatched. The industry has clear failure examples, including Celsius halting withdrawals and insolvencies such as Voyager and BlockFi. Nexo’s business model describes a collateralized approach, but public materials cannot independently prove full balance sheet strength or counterparty quality.

Early warning signs:

Operational risk shows up as login friction, withdrawal delays, and slow support during volatility. Incidents and maintenance updates appear on the status page, while recurring friction themes also surface in patterns on the Trustpilot profile.

Nexo had disclosed a DeFi related strategic investment, but a protocol level map showing whether and when customer funds route through DeFi is not consistently public.

What to take from that:

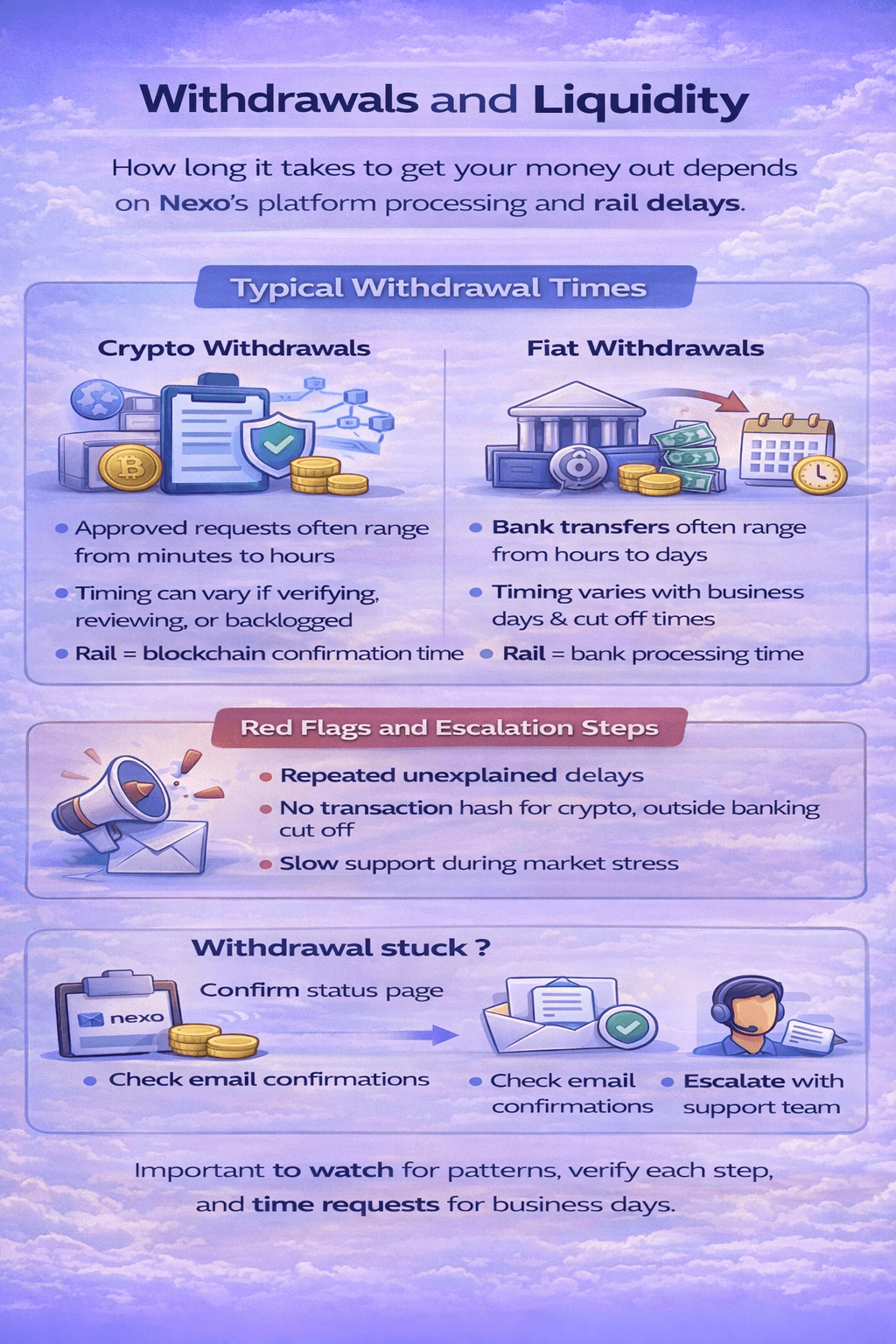

Withdrawals are where “safety” becomes real. On Nexo, the time it takes to get funds out depends on two separate steps: Nexo’s internal processing and the rail that moves the money, meaning blockchain confirmations for crypto and banking networks for fiat.

Withdrawals are where “Safety” becomes Real

Withdrawals are where “Safety” becomes RealCrypto Withdrawals

For crypto withdrawals, the most common experience is that once a withdrawal is approved and broadcast, the remaining time is mostly a blockchain question. In normal conditions, users often report minutes to a couple of hours, while longer waits usually fall into two buckets: network congestion that slows confirmations, or platform-side processing that delays broadcast. Situations that can push timing out include additional verification checks, manual review triggers, or wider platform incidents reflected in the status page.

Fiat Withdrawals

For fiat withdrawals, timing is generally less predictable because banks do not run on crypto time. Card-based cashouts through withdraw to card can be fast but Nexo doesn't offer that, while bank transfers are constrained by business days, cut off times, and intermediary bank processing.

When withdrawals take significantly longer than usual, the likely causes tend to be platform incidents, verification friction, or processing checks. Dated user reports on the Nexo Trustpilot profile include complaints about withdrawal delays and support response time during stressful market periods, which is useful as a signal of worst-case experience even when individual claims cannot be fully verified.

Practical escalation steps if a withdrawal is stuck:

Red flags are repeated unexplained delays, sudden withdrawal friction that affects many users at once, or a noticeable drop in communication clarity during incidents.

Withdrawal expectations differ by platform type.

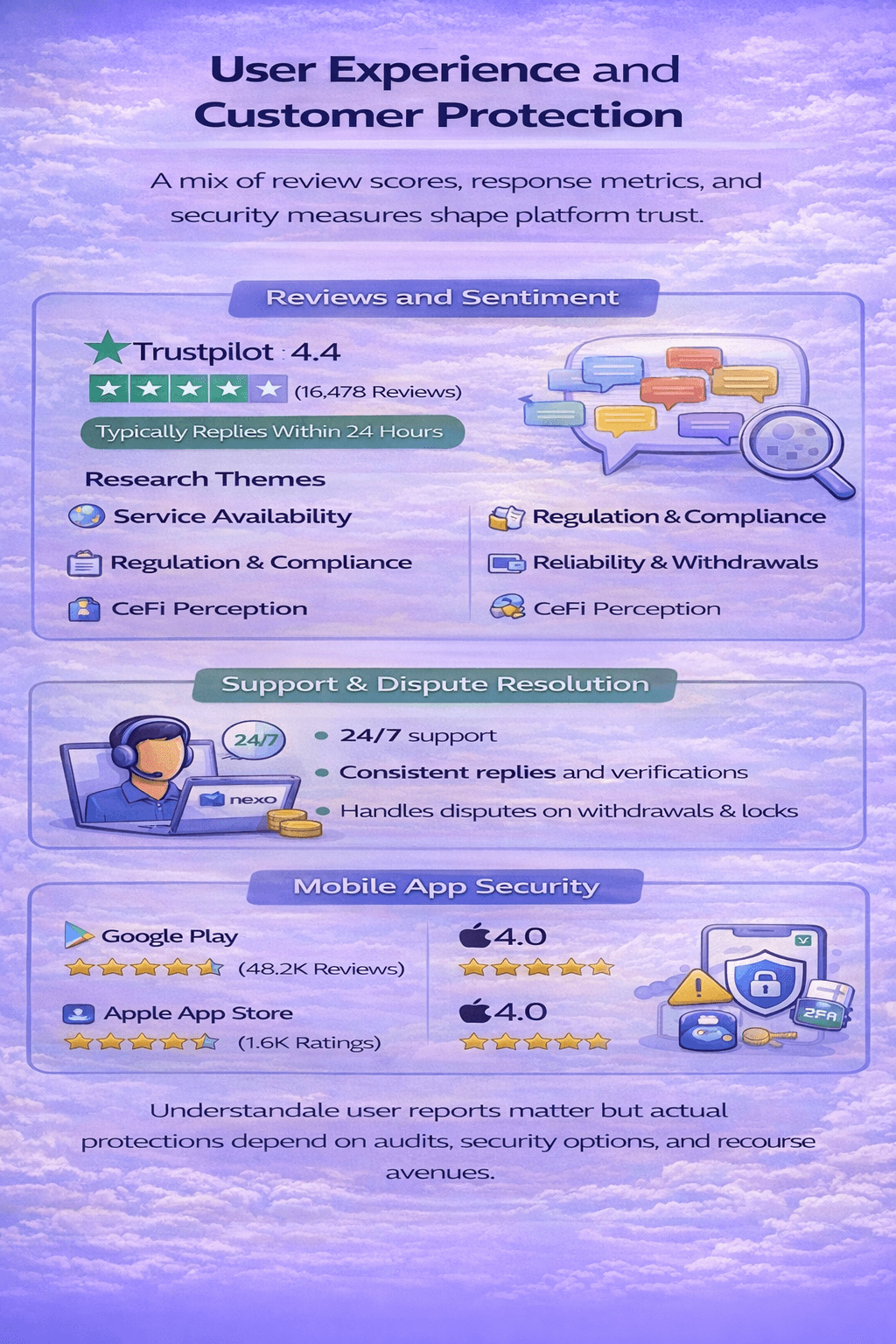

Nexo Offers 24/7 Client Care through in App Chat and Support Tickets, with a Public Help Center

Nexo Offers 24/7 Client Care through in App Chat and Support Tickets, with a Public Help CenterAs of Feb 18, 2026, Nexo holds a 4.4 TrustScore from 16,478 reviews, with Trustpilot also showing the platform typically replies within 24 hours and responds to essentially all negative reviews.

On community forums, themes tend to cluster around a few repeat topics rather than one single recurring complaint:

To reduce noise, we weight signals that are harder to fake and easier to compare over time:

Nexo offers 24/7 client care through in app chat and support tickets, with a public help center for common issues. A practical public benchmark is that Trustpilot currently shows Nexo typically replies within 24 hours, but real response speed can still swing based on queue volume and issue type.

The most common dispute categories surfaced across reviews and threads tend to be:

On mobile, the goal is to reduce the chance that a stolen phone or hijacked number becomes a full account takeover. Nexo supports stronger login options like passkeys, and its help docs note that a password reset signs you out of active sessions and disables biometric authentication on linked devices, which is a useful containment measure if credentials are compromised. Google Play’s data safety section also discloses categories of data the app may collect and share, which matters for users who want tighter privacy defaults.

For app sentiment, Nexo currently shows:

Practical mobile hardening tips that reduce the most common real world failure modes:

Check out our guide on how to avoid common Crypto Scams.

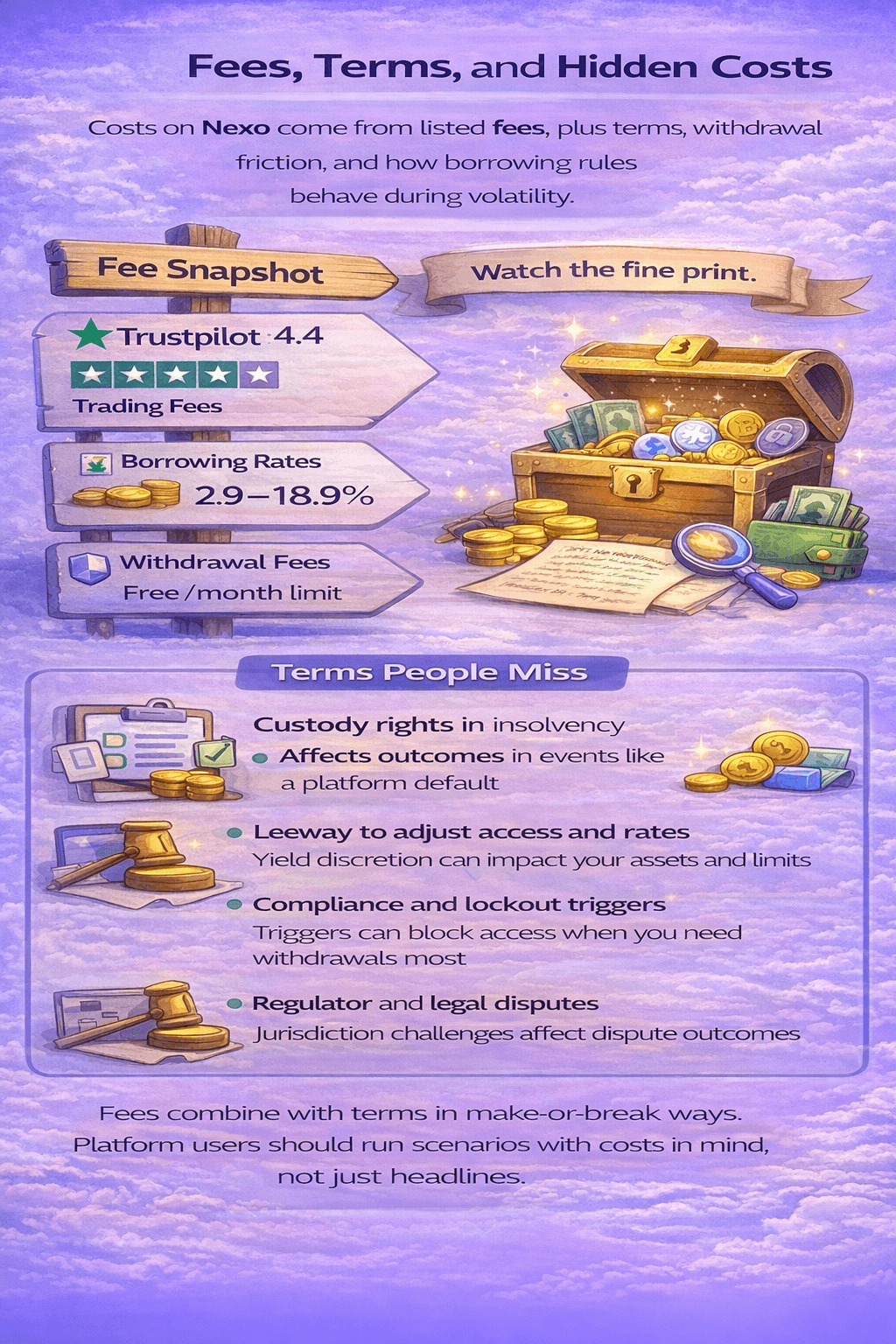

Costs on Nexo are not just “fees.” They also come from terms, withdrawal friction, and how borrowing rules behave during volatility.

Trading Fees on Nexo Pro Use a Tier based Maker Taker Model

Trading Fees on Nexo Pro Use a Tier based Maker Taker ModelExample 1, borrower at safe LTV versus aggressive LTV.

Takeaway: The same market move can be manageable at 50% LTV and catastrophic near 70% LTV.

Example 2, yield chaser versus conservative depositor.

Takeaway: Higher yield can be worth it only if the added return compensates for the extra risk and reduced flexibility.

Loyalty tiers can lower costs and boost rates, but they do not change the fundamental safety question on a centralized platform. The core risks remain custody, liquidity, and counterparty exposure.

Nexo's Loyalty Program, Nexo Wealth, Offers Tiers that are Based on Your Portfolio Allocation to the NEXO Token

Nexo's Loyalty Program, Nexo Wealth, Offers Tiers that are Based on Your Portfolio Allocation to the NEXO TokenNexo structures benefits through its Loyalty Program, now known as Nexo Wealth, with tiers that are based on your portfolio allocation to the NEXO Token.

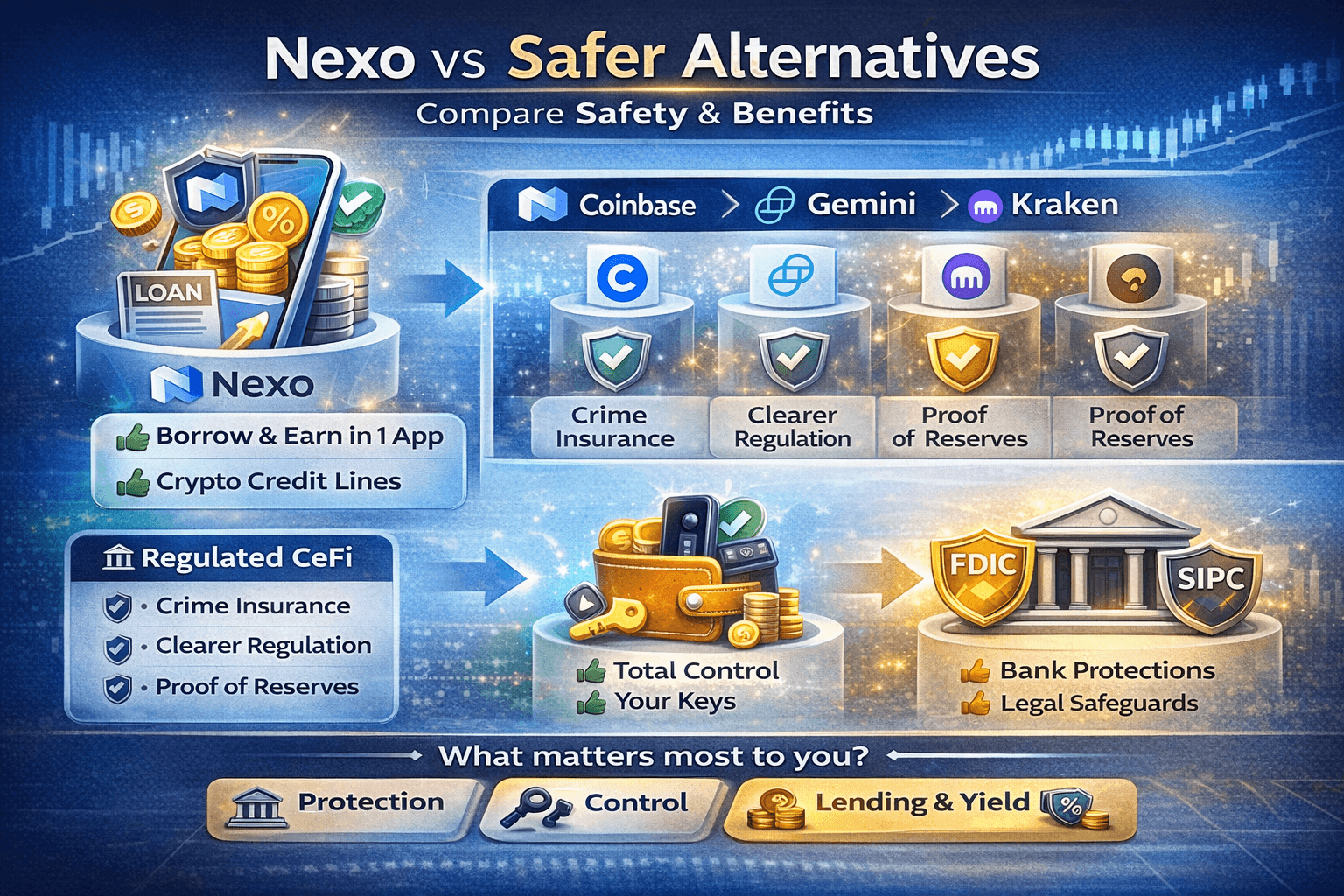

Choosing anoter option depends on what risk you are trying to reduce. This section compares Nexo against three common benchmarks: more regulated CeFi venues, self custody, and traditional finance protections.

Choosing a “Safer” Option Depends on what Risk You are Trying to Reduce

Choosing a “Safer” Option Depends on what Risk You are Trying to ReduceNexo vs Coinbase

Check out our exclusive Coinbase safety review for more details.

Nexo vs Gemini

We have a lot more detail on Gemini for you to read.

Nexo vs Kraken

Read up more on how safe Kraken is for better understanding.

Overall, the “safer” choice depends on your goal: statutory coverage favors TradFi, control favors self custody, and a unified crypto lending workflow favors platforms like Nexo.

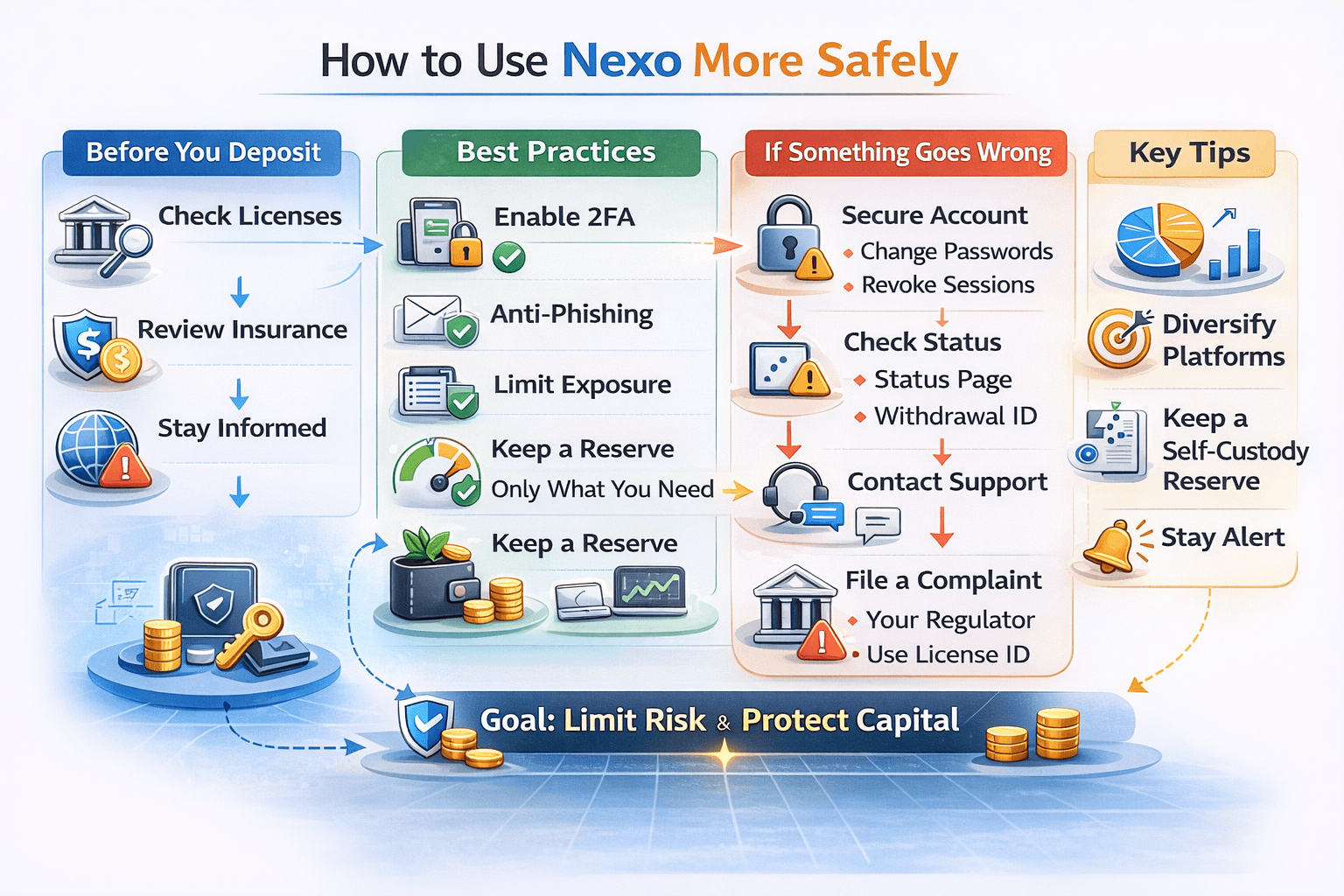

Using Nexo more safely is mostly about reducing blast radius. You cannot remove platform risk completely, but you can limit how much damage a single mistake or adverse event can cause.

You cannot Remove Platform Risk Completely, but You can Limit how much Damage a Single Event can Cause

You cannot Remove Platform Risk Completely, but You can Limit how much Damage a Single Event can CauseYou can also dive into our exclusive guide on mitigating risk in your trading life.

Nexo combines institutional custody tooling with consumer facing lending and yield products. The safety question is less about a single feature and more about whether the platform’s protections and transparency are sufficient for the level of exposure you are taking.

Nexo is acceptable only if you treat it as a convenience layer, not a vault. That means keeping exposure capped to an amount you can afford to have temporarily locked, using strict security settings, staying well below liquidation trigger zones, and maintaining a meaningful self custody reserve. This assessment should be rechecked monthly because legal status, product availability, and platform disclosures can change quickly.

I have over 15 years of experience writing for organizations across multiple industries, with a diverse portfolio that includes articles, blogs, website content, scripts, and slogans.

At The Coin Bureau, I specialize in crypto-focused content, covering exchanges, wallets, trading strategies, security practices, and emerging trends in blockchain. My work ranges from in-depth platform reviews and beginner-friendly guides to advanced analyses of trading bots, DeFi, and regulatory developments.

Beyond crypto, I also write fiction in my spare time and look forward to publishing my first collection of short stories.

Get exclusive access to premium content, member-only tools, and the inside track on everything crypto.