Most crypto products still assume users want to buy, hold, and wait. RedotPay takes a more practical route, focusing on what happens when people want to actually use stablecoins in everyday life rather than just watch them sit in a wallet.

That shift is what makes RedotPay interesting. It is not trying to be another trading-first platform dressed up with a card on the side. It is trying to turn crypto into something spendable, transferable, and useful in the real world, which makes it a very different kind of product to review.

RedotPay Review: Quick Verdict

RedotPay stands out most when you treat it as a stablecoin-powered payments app rather than just a crypto card. The card is the visible front end, but the platform’s real value comes from the wider stack around it, including bank and e-wallet transfers, internal user transfers, wallet funding, swaps, credit, P2P access, and Earn. That broader setup gives RedotPay more practical utility than many simpler card products, though it also means more fees, more moving parts, and more dependence on regional availability and platform controls.

Our take: RedotPay is one of the more useful crypto payments products for users who want spending, transfers, and balance management in one app, but it is less appealing for anyone who wants the simplest card experience, the strongest mainstream brand, or the lowest-friction fee structure.

Scorecard

-

1Product Depth 4.7/5 RedotPay feels broader than a typical crypto card because it combines spending, transfers, credit, swaps, P2P access, and Earn inside one ecosystem.

-

2Card Utility 4.4/5 The virtual and physical card setup is practical, with online spending, mobile wallet support, in-store use, and ATM access through the physical card.

-

3Payments and Transfers 4.8/5 Bank and e-wallet payouts, plus instant internal transfers, make RedotPay feel more like a real payments bridge than a card bolted onto crypto balances.

-

4Wallet and Funding Flexibility 4.5/5 The multi-currency wallet, crypto deposits, card purchases, and Binance Pay support give users several ways to fund and move value through the app.

-

5Fees and Cost Efficiency 4/5 Costs stay manageable when usage is simple, but physical card fees, top-up costs, cross-currency spending, ATM withdrawals, and selected-merchant charges can add friction fast.

-

6User Experience and Controls 4.5/5 The app looks modern and offers strong card controls, though onboarding, KYC, merchant restrictions, and payment-setting errors can make the experience less smooth than it first appears.

-

8Overall Score 4.6/5 A strong choice for users who want a crypto-powered payments app with real transfer utility, but less compelling for users who mainly want a cheap, simple, low-maintenance card.

Best For

- Users who want more than a crypto card and value a broader payments app experience

- People who need bank or e-wallet payouts alongside card spending

- Users comfortable managing balances, settings, and multiple product layers inside one app

- Crypto holders who like the idea of spending, swapping, sending, and parking assets in one ecosystem

Not Ideal For

- Users who want the simplest possible card product with minimal setup friction

- People sensitive to layered fees, cross-currency costs, or ATM charges

- Users in unsupported or restricted regions

- Anyone who prefers a fully non-custodial setup over a managed platform model

RedotPay At A Glance

| Category | Details |

|---|---|

| Core Identity | Stablecoin-based payments platform with a card built into a wider financial app |

| Main Product Stack | Card, bank and e-wallet transfers, RedotPay user transfers, credit, Earn, swaps, and P2P marketplace |

| Card Types | Virtual card and physical card |

| Wallet Structure | Multi-currency wallet supporting crypto and local-currency balances inside the app |

| Funding Routes | On-chain deposits, card-based crypto purchases, Binance Pay, and held in-app balances |

| Transfer Utility | Internal user transfers plus bank-account and e-wallet payouts in local currency |

| Main Trade-Off | Useful breadth and flexibility, but with more fees, more settings, and more platform dependence than a simpler card-only product |

Disclosure and Methodology

Some links in this article may be affiliate links. If you choose to use a service through these links, we may earn a commission at no additional cost to you.

For this review, we evaluated RedotPay across seven main categories: product depth, card utility, payments and transfers, wallet and funding flexibility, fees and cost efficiency, user experience and controls. We looked at how the platform works as a broader payments ecosystem rather than judging it only as a crypto card. That included the wallet structure, funding routes, virtual and physical card utility, bank and e-wallet transfers, internal user transfers, swap and P2P functionality, RedotPay Credit, Earn, app controls, and regional access limits. We also weighed the trade-offs carefully, including custodial reliance, feature complexity, identity verification requirements, payment-setting friction, and the fact that cost efficiency depends heavily on how the product is actually used day to day.

What Is RedotPay?

RedotPay is a stablecoin-based payments platform with a card built into a wider financial app. Rather than acting as a one-feature spending tool, it combines several services that help users hold, move, convert, and use digital assets inside one ecosystem.

RedotPay is Best Described as a Stablecoin-based Payments Platform with a Card Built into a Wider Financial App. Image via RedotPay

RedotPay is Best Described as a Stablecoin-based Payments Platform with a Card Built into a Wider Financial App. Image via RedotPayWhat the Product Actually Is

RedotPay's current consumer-facing product stack includes:

Instead of thinking of RedotPay as only a card, it makes more sense to view it as a digital money app built around stablecoins, with the card acting as one practical spending layer.

RedotPay Card and Everyday Spending Features

The RedotPay Card is the most visible part of the RedotPay experience, and for many users it will be the feature that shapes their first impression of the platform. But to judge how useful it really is, you need to look at both the payment experience and the practical rules around fees, limits, and controls.

The RedotPay Card is Still the Most Visible Part of the RedotPay Experience

The RedotPay Card is Still the Most Visible Part of the RedotPay ExperienceVirtual Card and Physical Card Experience

RedotPay offers both a virtual card and a physical card, and the difference between them is practical rather than cosmetic.

In simple terms:

- The virtual card is the faster option for online spending.

- The physical card adds in-store payments and ATM access.

- The physical card also supports the same online payment functions as the virtual card.

- During production, a physical card can still be used for online purchases, but contactless payments are not available until activation.

Online, In-Store and ATM Usage

In day-to-day use, RedotPay is designed to work across the payment settings most users care about. The virtual card can be used for online purchases and can also be linked to Google Pay and Apple Pay. The physical card expands that further with in-store POS transactions, ATM withdrawals, and contactless functionality after activation.

Card Controls, Limits, and Day-to-Day Usability

Apart from where it works, a strong card product is also about how much control users have when something goes wrong, or when they simply want tighter rules around how the card behaves. RedotPay includes card security settings that let users set per-purchase and daily limits, turn online, offline, and ATM transactions on or off, choose transaction currencies, adjust payment priority, and temporarily freeze a card.

For beginners especially, these controls can make the difference between a card that feels risky and one that feels manageable.

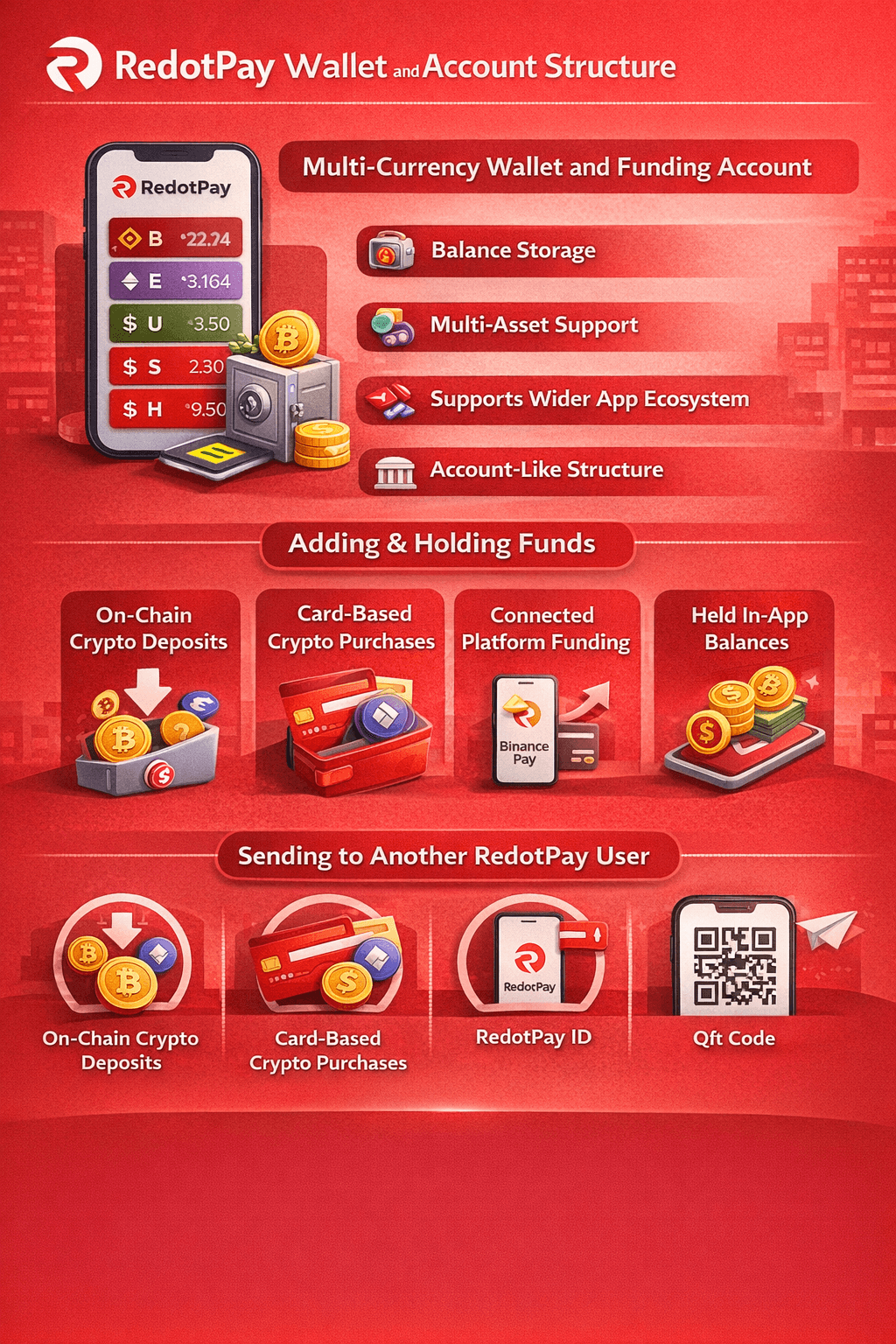

Funding, Wallet and Account Structure

The card may be the part users notice first, but the real foundation sits underneath it. RedotPay’s wallet and account structure is what allows value to be stored, funded, moved, and then routed toward spending, transfers, swaps, or credit.

RedotPay Card may be the Part Users Notice First, but the Real Foundation Sits underneath it

RedotPay Card may be the Part Users Notice First, but the Real Foundation Sits underneath itThe Multi-Currency Wallet and Funding Account

RedotPay’s Multi-Currency Wallet is designed to hold both crypto and local-currency balances inside the same app. It is building an account layer that supports the wider platform.

In practical terms, the wallet works as the base account for the rest of the product:

- Balance Storage: Users can keep value inside the app instead of treating RedotPay as a one-time spending tool.

- Multi-Asset Support: The wallet is meant to support different forms of value, including digital assets and local-currency balances.

- Supports Wider RedotPay App Ecosystem: The wallet sits underneath card usage, transfers, swaps, and credit functions.

- Account-Like Structure: RedotPay presents this setup more like a financial account system than a simple prepaid card balance.

How Users Add and Hold Funds

RedotPay gives users several ways to bring value into the platform and keep it there until they decide how to use it. The easiest way to understand this is to think of the wallet as a central pool of funds that can later be spent, transferred, swapped or pledged.

Common funding routes include:

- On-Chain Crypto Deposits: Users can send digital assets directly into RedotPay through the app’s Deposit function. This is the most direct crypto-native route.

- Card-Based Crypto Purchases: Users can also buy crypto with a credit or debit card, which can be easier for beginners.

- Connected Platform Funding: RedotPay supports deposits through Binance Pay, giving users another route into the app.

- Held In-App Balances: Once funds arrive, they can remain inside RedotPay until the user chooses what to do next.

Send to Another RedotPay User

RedotPay also supports internal transfers between users, and this is one of the features that makes the platform feel more like a payments network than a card attached to a balance. Users can send funds directly inside the app without making an external blockchain transfer.

Transfers can be made using:

- Email Address

- Phone Number

- RedotPay ID

- QR Code through the app’s send function

RedotPay says these transfers are currently free and usually instant, though both users must complete identity verification and completed transfers cannot be reversed.

Send to Bank and E-Wallet: RedotPay as a Payments Tool

RedotPay becomes much more interesting once you look beyond the card. Its send to bank & e-wallet feature is built for a more practical job: helping users move crypto value into familiar payment channels where it can arrive as local currency and be used in everyday life.

RedotPay Offers a Send to Bank & E-Wallet Feature is Designed to Move Money Out into Everyday Financial Channels

RedotPay Offers a Send to Bank & E-Wallet Feature is Designed to Move Money Out into Everyday Financial ChannelsHow the Bank and E-Wallet Transfer Feature Works

At a basic level, this feature lets users turn crypto into local currency and send it straight to bank accounts or e-wallets. That is the key use case: not just spending from a card balance, but converting digital assets into a payout that another person can actually receive in a familiar local format.

In practical terms, the flow is fairly simple:

- Choose the asset and amount you want to send.

- Add or select the recipient’s bank account or e-wallet details.

- Review the payout details before confirming.

- Let RedotPay route the transfer into the recipient’s local currency destination.

RedotPay also says the fee, expected received amount, and estimated arrival time are shown on screen before sending.

Why This Feature Is More Important Than the Card for Some Users

For some users, this may actually be more valuable than the card itself. A card is helpful when you want to pay a merchant directly, but a transfer tool is often more useful when the real goal is remittance services, cross-border support, or sending money to someone who simply needs cash in a bank account or e-wallet rather than crypto on-chain.

That makes RedotPay feel less like a spending outlet and more like a practical bridge between crypto balances and local-money needs.

Real-World Use Cases

In everyday terms, this feature can suit use cases such as:

- Sending money to family in another country.

- Moving funds to your own bank account or e-wallet.

- Paying someone who does not use crypto directly.

- Handling small business-style payouts where the recipient prefers local currency.

RedotPay is not only built for card spending, but also for moving value into everyday payment channels where recipients can actually receive and use local currency.

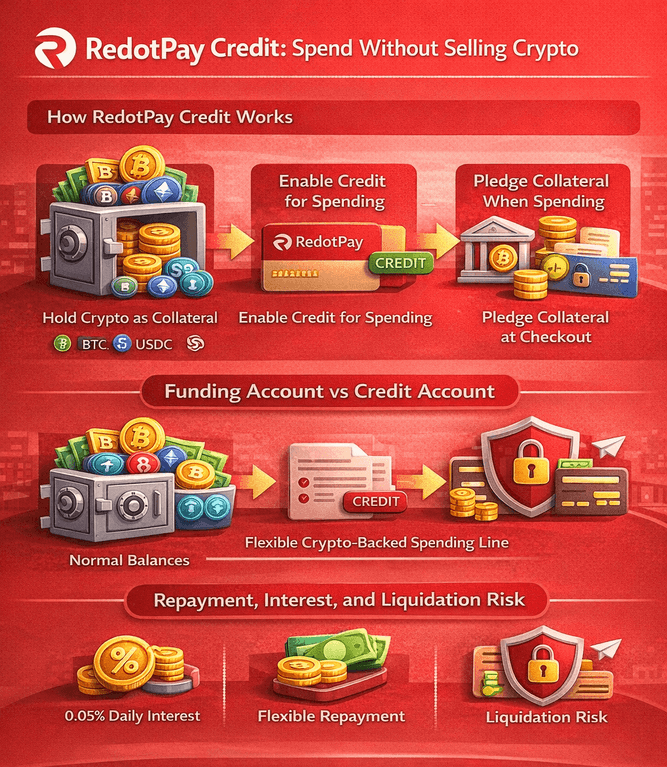

RedotPay Credit: Spend Without Selling Crypto

RedotPay Credit changes the usual crypto spending equation. Instead of selling your holdings first and giving up future upside, it lets you use supported crypto as collateral and unlock spending power while keeping your market exposure in place.

RedotPay Credit Works Like a Crypto-Backed Spending Line

RedotPay Credit Works Like a Crypto-Backed Spending LineHow RedotPay Credit Works

RedotPay Credit works like a crypto-backed spending line. Users can access a flexible credit line backed by their cryptocurrency holdings and use it across the RedotPay ecosystem without selling those assets.

At a high level, the process looks like this:

- Hold Supported Collateral: Your credit limit comes from the value of supported cryptocurrencies in your RedotPay account. Right now, RedotPay says those include BTC, ETH, SOL, TON, TRX, S, XRP, and BNB, while USDT and USDC do not count toward the limit.

- Enable Credit As The Payment Method: Once activated, RedotPay prioritizes the credit line instead of deducting directly from your available balance.

- Pledge Collateral At The Moment of Spending: When you make a payment, part of your crypto is locked as collateral and the transaction amount is added to your credit balance.

If you are familiar with our guide on crypto lending platforms, the idea is similar, but here the product is designed around spending rather than withdrawing a cash loan first.

Funding Account vs Credit Account

RedotPay separates the structure into two parts:

- Funding Account: This is the main balance where deposits arrive and where funds normally sit.

- Credit Account: This is the dedicated account for pledged collateral. Once crypto is moved here and a balance is outstanding, those assets are locked and support a real-time credit limit.

Repayment, Interest and Liquidation Risk

Credit may feel smooth at checkout, but it is still a loan-like product with collateral risk.

RedotPay’s risk management rules highlight three key mechanics:

- Interest: Simple interest is charged at 0.05% per day, with no compounding.

- Repayment Flexibility: There is no fixed repayment date, and users can repay either from balance or collateral.

- Liquidation Risk: If the risk index reaches 0.9 or above, liquidation is triggered.

The same rules also define the in-app risk bands:

- Below 0.6: Safe

- 0.6–0.8: Moderate

- 0.8–0.9: Margin Call

- 0.9 and above: Liquidation

The appeal here is obvious: you can spend without selling. But the trade-off is just as important: if the market moves against your collateral and you do not manage the position, the convenience can quickly turn into forced asset sales.

Swap, P2P and Asset Conversion Features

Swaps and P2P are not side tools, but practical parts of how value moves through the app.

RedotPay is not Built on the Idea that Users will always Arrive with the Exact Asset they Need in the Exact Form they Need it

RedotPay is not Built on the Idea that Users will always Arrive with the Exact Asset they Need in the Exact Form they Need itInstant Swaps Inside the App

RedotPay’s Swap feature is designed to let users convert between digital assets inside the app with a few taps. That matters because most people do not use one asset for every job. They may top up in one token, want to spend in another, or need to rebalance before making a transfer.

In practical terms, in-app swaps help with things like:

- Instantly Add Funds: Useful when you want to top up a more usable balance before spending through the card.

- Convert Between Digital Assets: Helpful for adjusting balances inside the app without moving funds to another platform.

- Send Crypto, Receive Local Currencies: Relevant when the goal is to move value into bank-account or e-wallet transfers rather than keep it in crypto form.

- Use EUR and GBP Balances For Currency Swaps: Adds flexibility by letting local-currency balances convert into supported stablecoins inside the app.

P2P Marketplace and Stablecoin Access

The P2P Marketplace serves a different role. It is best understood as an access layer for buying and selling digital currencies directly with other users, using preferred local currencies, prices, and payment methods. That is useful, especially for users who need more flexibility in how they enter or exit stablecoin positions.

Just as importantly, RedotPay does not frame this as a loose informal marketplace. Its P2P trading flow includes crypto fund escrow, which helps reduce settlement risk during person-to-person trades.

How Conversion Supports the Rest of the Product

Swaps help users reshape balances inside the app, while P2P helps them access digital assets through local payment methods. Together, those features make it easier to fund the wallet, prepare for card spending, support transfers, and keep money moving without unnecessary friction.

Conversion is one of the main reasons the platform works like a payments app rather than just a card attached to a static balance.

RedotPay Earn

With Earn, RedotPay is also trying to keep users inside the app for the quieter part of the money journey too: holding assets, collecting rewards, and deciding when to move those funds back into active use.

RedotPay Earn Lets Users Earn Rewards on Supported Assets Held In-App

RedotPay Earn Lets Users Earn Rewards on Supported Assets Held In-AppHow Earn Works

At a basic level, RedotPay Earn is built around a simple proposition: deposit supported digital assets, keep them in the RedotPay ecosystem, and receive rewards on your digital assets instead of leaving those balances idle.

In practical terms, that means users can:

- Put supported assets into Earn.

- Keep them there for flexible periods of time.

- Collect rewards without moving funds out to a separate yield platform.

It makes Earn feel less like a standalone investment product and more like an extension of the broader RedotPay account experience.

Flexibility, Withdrawals and Practical Utility

The useful part is that Earn is not framed as a locked-away balance that becomes hard to use. RedotPay says the rewards generated can be withdrawn or used for daily expenses, which gives the feature more day-to-day relevance than a passive yield product that sits completely outside spending activity.

For users who already keep funds inside RedotPay, that flexibility can be appealing. Instead of treating every parked balance as dead capital, Earn gives those assets a way to stay productive while still feeling connected to the rest of the app.

Risks and Regional Caveats

That said, Earn is not a risk-free parking spot. RedotPay states that projected returns are estimates only, may vary with market conditions, and that capital is at risk, including the possible loss of part or all of the invested amount.

Availability is also not universal. RedotPay says Earn is only available in selected regions, and its Crypto Earn terms specifically state that the service is not made available to the Hong Kong public. More broadly, RedotPay as a platform itself, is not supported in several markets, including the United States, Mainland China, Russia, and Ukraine.

While Earn does make RedotPay feel broader than a pure spend app, it still needs to be viewed with the right mindset: useful and convenient, but not the same thing as cash in a savings account.

Fees, Limits and Cost Friction

A platform can feel smooth in theory, excellent with its products or services, but the real test is what users actually pay, where friction shows up, and which costs are easy to miss at first glance.

RedotPay can be Cost-Effective, but the Wrong Usage Pattern makes it Expensive Fast

RedotPay can be Cost-Effective, but the Wrong Usage Pattern makes it Expensive FastCard Fees and Usage Costs

The clearest place to start is the card itself. With RedotPay’s current card limitations and fees and selected merchant transaction fee rules, the main card-side costs and limits look like this:

Category | Virtual Card | Physical Card |

|---|---|---|

Card Setup Fee | $10 application fee | $100 application fee; mailing waived |

Transaction Fee | 1.00% | 1.00% |

Non-Default Currency Transaction Fee | 1.20% | 1.20% |

Selected Merchant Transaction Fee | 1.5% minimum $0.50; up to 3 fee waivers per month on eligible transactions | 1.5% minimum $0.50; up to 3 fee waivers per month on eligible transactions |

ATM Withdrawal Fee | Not applicable | HKD card: 2.00%; USD card: 2% up to $10,000 monthly, then 3% above $10,000 monthly |

Maintenance Fee | Waived | Waived |

Card Cancellation Fee | $2 per card | $2 per card |

Per-Transaction Spending Limit | $100,000 | 100,000 |

Daily Spending Limit | $1,000,000 | $1,000,000 |

ATM Withdrawal Frequency Limit | Not applicable | 3 per day / 30 per month |

Transfer, Conversion and Hidden-Cost Considerations

The less obvious friction sits outside the card itself. International transfer fees vary by currency and receiving method, which means the true cost depends on the payout route rather than a single flat schedule. Users will see both the fee and the amount the recipient will get before confirming.

There are also entry and conversion costs that some users may underestimate. Mainstream credit and debit card top-ups carry a standard 3% fee with a 1 USD minimum, while RedotPay’s Swap materials emphasize transparent, low fees rather than publishing one simple universal rate card.

Is RedotPay Cheap Enough for Everyday Use?

For users who stay mostly digital, spend in the default currency, and avoid unnecessary cash withdrawals, RedotPay can be reasonably efficient. But once you add a physical card, ATM use, cross-currency spending, selected-merchant charges, or card-funded top-ups, the cost picture becomes less lightweight.

RedotPay is not especially expensive across the board, but it is also not the kind of product you can treat carelessly. It rewards users who understand the fee map before they start using it like an everyday spending tool.

User Experience, App Controls and Onboarding

RedotPay’s feature list may be broad, but that only matters if the app is usable in practice. The good news is that the experience looks more like a modern fintech app than a clunky crypto wallet, though there is still some friction once verification, card settings, and regional restrictions enter the picture.

RedotPay’s Feature List is Broad, but that only Matters if the App is Usable in Practice

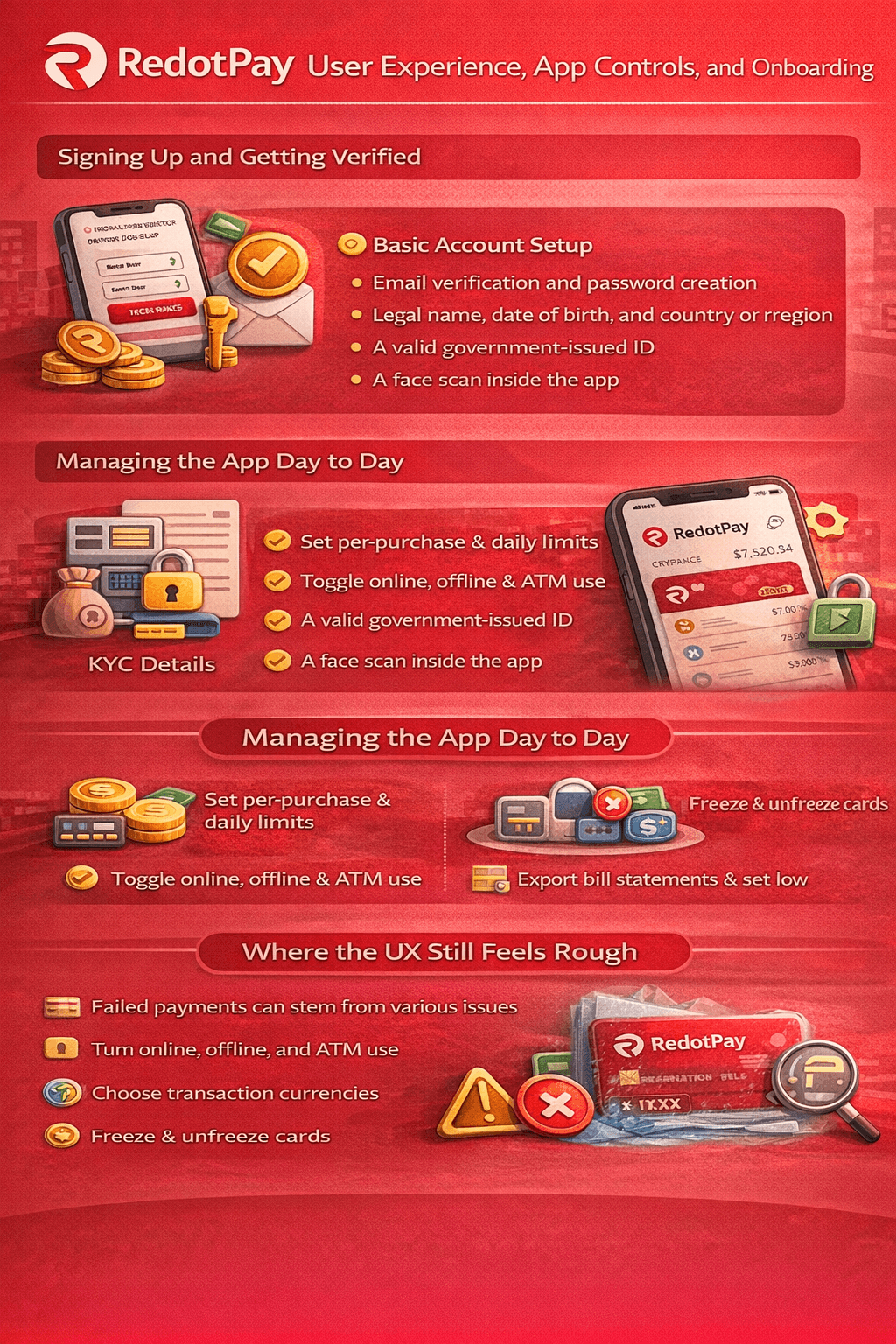

RedotPay’s Feature List is Broad, but that only Matters if the App is Usable in PracticeSigning Up and Getting Verified

The initial account registration and setup is fairly simple: sign up in the mobile app, verify your email, and create a password. The bigger step is identity verification, which requires personal details, a photo of your ID, a face scan, and, in some cases, a personal statement.

The onboarding flow includes:

- Basic Account Setup: Email verification and password creation.

- KYC Details: Legal name, date of birth, and country or region.

- Document Checks: A valid government-issued ID.

- Biometric Verification: A face scan inside the app.

This will feel easy enough for users already used to fintech onboarding, but more annoying for anyone who wants a low-friction sign-up. It also becomes a non-starter in unsupported countries and regions, where access to the app is blocked altogether.

Managing the App Day to Day

Once inside, the app gives users a decent amount of control. Through card security settings, users can:

- Set per-purchase and daily card limits.

- Turn online, offline, and ATM transactions on or off.

- Choose transaction currencies.

- Reorder payment priority and spending currency priority.

- Freeze and unfreeze a card.

For routine visibility, users can also export bill statements, while low balance alerts add a useful reminder layer for everyday spending.

Where the UX Still Feels Rough

The rough edges show up when settings, security rules, and merchant behavior collide. RedotPay’s own payment rejection guidance makes clear that failed payments can come from frozen cards, insufficient balance, disabled currencies, incorrect payment settings, or merchant-specific restrictions. On top of that, a card can be temporarily frozen after repeated mistakes such as entering the wrong ATM PIN or CVV too many times.

The overall experience is usable and fairly well controlled, but it is not frictionless. RedotPay works best for users who are comfortable managing settings carefully rather than assuming the app will handle every edge case in the background.

Is RedotPay Safe and Legit in 2026?

RedotPay looks polished, but trust here depends on more than the card itself. The real question is whether the broader app ecosystem shows enough structure, controls, and compliance signals to feel credible.

RedotPay Looks Polished, but Trust Depends on more than the Card itself

RedotPay Looks Polished, but Trust Depends on more than the Card itselfSecurity, Compliance, and Platform Trust Signals

RedotPay operates under several recognised regulatory frameworks, including VASP authorisation in Argentina, MSB registration in Canada, a FinCEN-registered MSB status in the United States, and Money Lender and TCSP licences in Hong Kong. It has also said it obtained VASP registration from Lithuania’s Financial Crime Investigation Service, which adds another formal compliance signal to the platform’s trust profile.

Card and Transaction Safety Features

On the user-control side, RedotPay gives cardholders several built-in protections through its card security settings. Users can:

- Set per-purchase and daily limits.

- Switch online, offline, and ATM transactions on or off.

- Choose settlement currencies.

- Freeze and unfreeze the card when needed.

There are also automated controls. A card can be temporarily frozen after repeated incorrect PIN, CVV, or expiry-date entries.

Which Features May Vary by Region

Even in supported markets, feature access is not always identical. A few examples stand out:

- Earn is only available in selected regions.

- P2P availability depends on local regulations and supported payment methods.

- Physical card delivery is unavailable in some countries and regions, even where the broader platform may still be accessible.

The Main Risk Trade-Offs

The main trade-off is straightforward: When you use RedotPay, you are trusting a managed payments ecosystem, not just a card. That includes wallet balances, transfers, spending rules, and compliance boundaries, which is why unsupported regions matter so much.

RedotPay appears legitimate and structured. But the trust model is still custodial and platform-dependent, which means convenience comes with reliance on RedotPay’s own systems and controls.

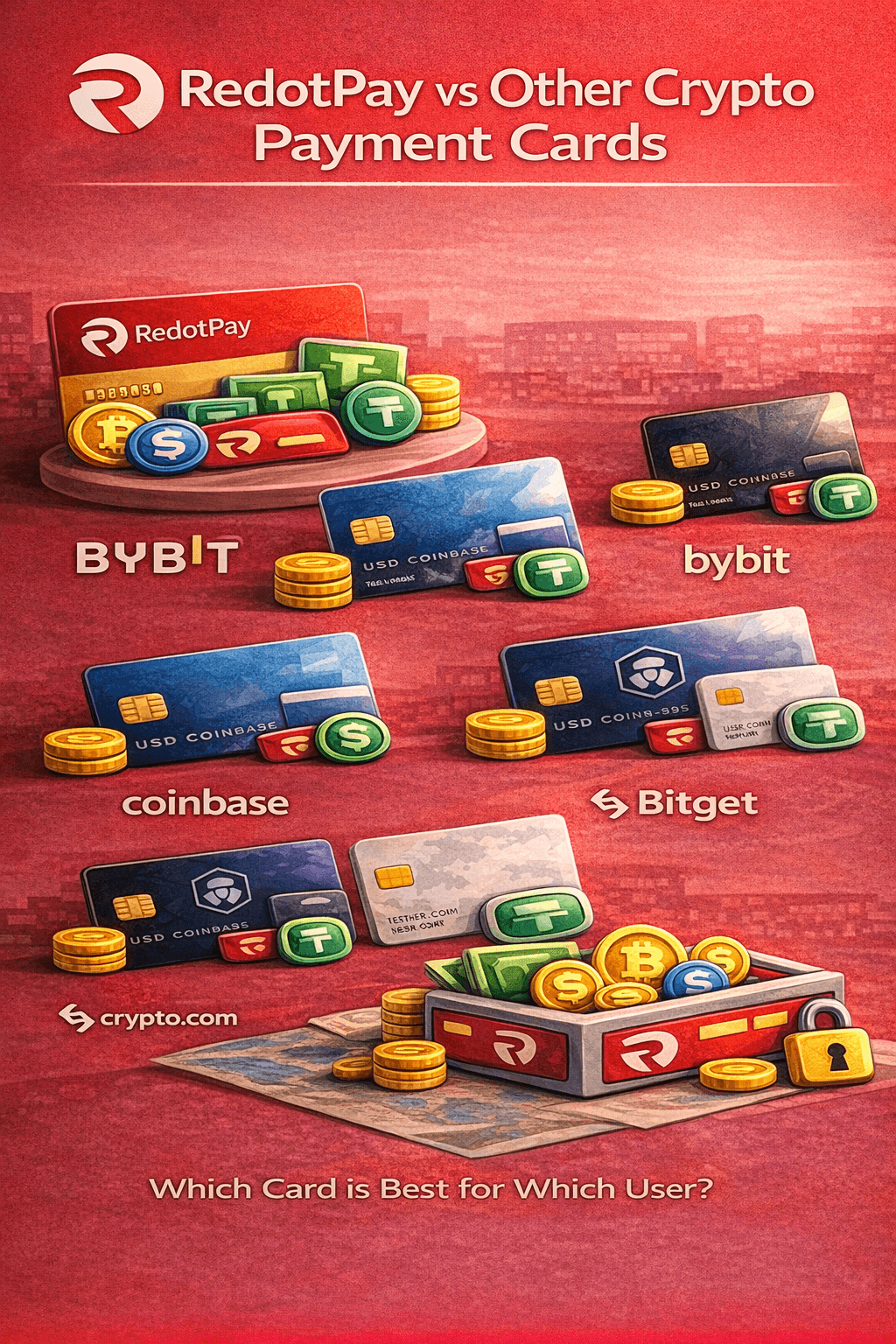

RedotPay vs Other Crypto Payment Cards

Not all crypto payment cards are trying to solve the same problem. Some are mainly rewards products, some are exchange extensions, and some, like RedotPay, are trying to act more like full payments apps with a card attached.

Not All Crypto Payment Cards are Trying to Solve the Same Problem

Not All Crypto Payment Cards are Trying to Solve the Same ProblemRedotPay vs Other Crypto Payment Cards

Platform | Best For | What Stands Out | Main Trade-Off |

|---|---|---|---|

RedotPay | Users who want a payments-first app, not just a spending card | Built around bank and e-wallet transfers as well as card use | Broader feature depth also means more moving parts to understand |

| Existing Bybit users who want spending plus exchange-linked perks | Offers up to 10% cashback and a card experience tied closely to the Bybit ecosystem | Best fit depends heavily on the specific regional card program | |

| Mainstream users who want a simpler card from a better-known brand | Emphasises zero spending fees and everyday crypto rewards | Feels more like a card extension than a broader payments toolkit | |

| Rewards-focused users who are comfortable with a tiered ecosystem | Pushes a stronger loyalty angle with up to 5% back and tier-based perks | The structure is more layered, with benefits shaped by plan or staking level | |

| Users who want a travel-friendly exchange card with strong rewards marketing | Focuses on USDC spending in 180+ countries and regions and headline cashback | Still looks earlier-stage in rollout and availability than some larger rivals |

Which Card Is Best for Which User?

- Choose RedotPay if you want more than a card and like the idea of spending, transfers, and Credit sitting inside one app.

- Choose Bybit Card if you are already inside the Bybit ecosystem and value support for Apple Pay, Google Pay, and Samsung Pay alongside card rewards.

- Choose Coinbase Card if you want a cleaner mainstream feel and live in a supported market such as the US, where the card is available in all states except Hawaii.

- Choose Crypto.com Card if your priority is card perks and ecosystem rewards, especially if you are comfortable with the Level Up style of tier-based benefits.

- Choose Bitget Card if you are a Bitget user in its current rollout zone, since the card is available only in select APAC jurisdictions at launch.

The practical takeaway is simple: RedotPay looks strongest when judged as a flexible payments app with a card on top, while several rivals look stronger when judged mainly as crypto rewards cards tied to their own exchange ecosystems.

Final Verdict: Is RedotPay Worth It in 2026?

RedotPay is at its best when you treat it as a crypto-powered payments app, not just another card. It does a strong job combining spending, transfers, wallet functions, credit, and asset conversion in one place, which makes it far more useful than many simpler crypto card products.

It feels weaker where access, fees, and feature complexity start to stack up. RedotPay is worth serious consideration for users who want practical everyday crypto utility, especially across payments and transfers. But if you want the strongest mainstream brand, the richest card perks, or the simplest experience possible, a competitor may fit better. At the end of the day, knowledge, research and due diligence is always needed to improve the quality of your choices that align with your own trading ambitions.