Nexo works like an all-in-one crypto wealth app where users can earn, borrow, trade, and spend from one account. That convenience is the main draw.

That same setup also defines the trade-offs. Nexo’s best perks often depend on the NEXO token, product access changes by region, and users still take on platform risk instead of staying in self-custody. This review looks at where Nexo works well, where it falls short, and who it makes sense for.

Editor's Note (April 2, 2026): We fully updated this review in April 2026 to reflect Nexo’s current product lineup, loyalty structure, borrowing terms, earn products, card features, regional restrictions, and overall user experience. We also rewrote the review to better explain how Nexo works in practice, where its strongest value sits, and which trade-offs matter most for users.

Quick Verdict

Nexo is one of the stronger all-in-one crypto finance platforms for users who want earning, borrowing, trading, and card-based spending to sit inside one centralized account. Its biggest strengths are product integration, crypto-backed borrowing, and a polished account experience. Its biggest trade-offs are token-dependent pricing, regional feature restrictions, and the usual counterparty risk that comes with centralized custody. Nexo works best for users who value convenience and a connected product stack more than self-custody purity or the simplest pricing model.

Our take: Nexo is a strong fit for users who want a managed crypto finance hub with borrowing, earning, and spending in one place, but it is a weaker fit for readers who want self-custody, universal product access, or the best pricing without NEXO token exposure.

Scorecard

-

1Product Range 4.8/5 Few platforms bundle earning, borrowing, trading, card spending, and private client services this tightly in one account.

-

2Borrowing Utility 4.7/5 Crypto-backed credit remains one of Nexo’s clearest strengths, though real costs depend heavily on LTV, tier, and product terms.

-

3Pricing Transparency 4.5/5 Rates and perks can look attractive, but the best version of almost every offer sits behind loyalty tiers and extra conditions.

-

4Trust and Risk Model 4.5/5 Nexo has real infrastructure and custody partners, but users still take on centralized platform risk and regional access limitations.

-

5Ease of Use 4.6/5 The app and web experience are smooth, though newer users may find the loyalty system and advanced products more layered than expected.

-

6Overall Score 4.8/5 A strong all-in-one crypto platform for users who want convenience, borrowing flexibility, and integrated account tools under centralized custody.

Best For

- Users who want earning, borrowing, trading, and spending in one account

- Crypto holders who want to borrow without selling core positions

- People who prefer a polished centralized platform over self-custody complexity

- Users comfortable with loyalty tiers and NEXO-token-linked perks

Not Ideal For

- Users who prioritize self-custody and direct control over assets

- People who want the best rates without token-linked conditions

- Readers in regions where card, futures, or earn access is restricted

- Beginners likely to drift from simple products into leverage or structured products too quickly

Nexo At A Glance

| Category | Details |

|---|---|

| Type | Centralized crypto finance platform |

| Core Use Cases | Earn, borrow, trade, swap, and spend from one account |

| Borrowing Model | Crypto-backed credit lines based on loan-to-value rules |

| Card Model | Nexo Card with Debit Mode and Credit Mode |

| Loyalty Structure | Base, Silver, Gold, and Platinum tiers tied to NEXO token allocation |

| Custody Model | Centralized platform using institutional custody infrastructure and partners |

| Higher-Risk Tools | Perpetual futures, Booster, and Dual Investment |

Disclosure and Methodology

Some links in this Nexo review may be affiliate links. If you choose to use a service through these links, we may earn a commission at no additional cost to you. That does not change how we assess Nexo’s borrowing model, earn products, loyalty structure, card utility, pricing conditions, or overall fit for different types of crypto users.

For this review, we evaluated Nexo across five main categories: product range, borrowing utility, pricing transparency, trust and risk model, and ease of use. We reviewed Nexo’s own product materials and support documentation covering crypto-backed credit, Flexible and Fixed-term Savings, exchange services, loyalty tiers, the Nexo Card, futures access, custody setup, onboarding checks, and regional restrictions. We also weighed how the platform works in practice for users who want one account to manage several crypto-finance tasks, while treating centralized custody risk, token-linked pricing, product conditions, and geographic limitations as core parts of the final score.

What Is Nexo and How Does It Work?

A lot of crypto platforms start with one use case and then keep adding rooms to the house. Nexo did exactly that. It began with crypto-backed credit, then kept building until it turned into a place where users can store assets, earn, borrow, trade, and spend from the same account.

The upside is obvious. You do not need five separate apps to manage five separate jobs. The downside is just as real. Once a platform tries to do this much, clarity becomes more important than marketing. So the real question is not “what features does Nexo list?” It is “how do those features connect when an actual user puts money on the platform?” That is where the mechanics matter.

A Single Platform Turning Crypto Into A Working Account

A Single Platform Turning Crypto Into A Working AccountNexo In One Sentence

Nexo is a centralized crypto platform where users can deposit digital assets, earn on them, borrow against them, trade them, and spend through the Nexo Card from one account.

Nexo is not only about crypto lending anymore. Credit is still one of the pillars, but the platform now leans just as hard on crypto savings, exchange features, and card-based spending. The product mix is the story here.

From Crypto Loans To Wealth Platform

Nexo first built its name around crypto-backed loans. That was the simple pitch: keep your crypto, use it as collateral, and unlock liquidity without selling. Over time, the company expanded that model into something much larger. Today, Nexo positions itself around earn products, the Nexo Exchange, the Nexo Card, crypto-backed credit lines, and higher-risk tools like perpetual futures. It also runs private client services for larger users.

That shift says a lot about who the platform is for. Nexo is aiming at users who want their crypto activity to happen in one place. Someone might top up Bitcoin, move part of it into a savings flow, borrow stablecoins against another part, swap assets within the app, and then use the Nexo Card to spend. That is a very different pitch from a single-purpose lending app. It is closer to a managed crypto finance hub.

Take a look at our top picks for the best crypto lending platforms.

How The Platform Actually Works

In its simplest form, you deposit assets once, then decide whether those assets should earn, support borrowing, fund spending or move through trading tools.

Nexo starts with deposits. Users add supported digital assets to their account, and then choose what role those assets will play. Some assets can sit in a Savings Wallet and earn yield. Some can support a Credit Line as collateral. Some can be swapped, traded, or used for spending flows tied to the card. The point is that the same account acts as the base layer for several different actions.

The borrowing side works through collateral. Instead of selling your crypto, you can use eligible assets to open a crypto-backed credit line. Nexo then lets you draw against that value, subject to the platform’s loan-to-value rules. That setup is one of the main reasons people use services like this in the first place. It gives access to liquidity while keeping market exposure. Of course, that only feels clever while collateral values hold up. When prices swing hard, the same structure can become the source of pressure.

The card follows the same logic. In Credit Mode, purchases are linked to your Credit Line, which means you are spending against collateral rather than directly selling assets. In Debit Mode, you spend selected assets from your balance, and Nexo handles conversion behind the scenes. That dual setup is one of the clearest examples of what the platform is trying to be, which is a place where savings, borrowing, and spending are part of one loop rather than separate products living in separate tabs.

The same pattern carries over to trading. Nexo’s exchange services include standard swaps, recurring buys, and target-price features, while its futures offering adds perpetual futures for users who want leverage and more active positioning. That is useful for users who want convenience. It is also where the platform starts to split into two personalities: one built for passive users who want earning and borrowing, and another built for people willing to take on much more risk.

Is Nexo Safe and Legit?

Yes, Nexo is a legitimate centralized crypto company with real products, real custody partners, and a live support and compliance structure.

But what kind of safety Nexo actually offers, and what kind it does not? With a platform like this, safety is never only about password settings and vault providers. It is also about who controls the assets, what depends on the company, and where access starts to break down by region or product.

The cleanest way to judge Nexo is to split the issue into four parts.

- First, there is the security stack around custody and account protection.

- Second, there is the trade-off between platform risk and self-custody.

- Third, there is regulation and product availability, which are not the same thing.

- Last, there is trust itself, meaning what the user can independently verify and what still rests on the company’s systems, decisions, and disclosures.

- Read: Is Nexo Safe?

Understanding Nexo’s Safety Model, Risks, And Trust Boundaries

Understanding Nexo’s Safety Model, Risks, And Trust BoundariesSecurity Infrastructure

On the custody side, Nexo works with institutional partners including Ledger Vault and Fireblocks, alongside other custodians. This shows Nexo is not presenting itself as a casual wallet app with improvised storage practices. Its support material frames custody around institutional infrastructure, which is the right baseline for a company holding client digital assets at scale.

At the account level, Nexo also points users toward standard protections such as two-factor authentication, anti-phishing tools, and verification of official communication channels. The company says official emails come from the verified nexo.com domain, and it gives users the option to set an Anti-Phishing Code. Those are not flashy features, though they matter more than any glossy security slogan. They reduce the kinds of account-level mistakes that often cause damage long before a custody provider ever enters the story.

Platform Risk vs Self-Custody Risk

Nexo becomes convenient precisely because it asks users to give up a level of direct control. You deposit assets into a centralized environment so the platform can make borrowing, earning, spending, and trading feel smooth from one account. That is the trade. The comfort comes from delegation. The risk comes from the same place.

A self-custody user carries more operational responsibility. They manage keys, security hygiene, and transaction handling themselves. A Nexo user hands more of that burden to the platform, but in return takes on counterparty risk. That means your experience depends on Nexo’s custody setup, compliance framework, internal controls, and business continuity rather than on your own wallet alone. For some users, that is a fair exchange. For others, it is the whole reason to stay away.

That distinction needs to be stated plainly because many reviews blur it. Nexo can be safer than self-custody for a careless user who would mishandle seed phrases or security setup. At the same time, self-custody can be safer than Nexo for a disciplined user who wants to avoid centralized dependency altogether. These are different safety models, not a simple ladder where one sits above the other.

Regulation, Licensing, and Geographic Restrictions

The platform's access model is more limited than a quick skim of its marketing might suggest. The company’s help center states clearly that its services are not available in certain jurisdictions and that restrictions or limitations may apply depending on where the client resides. That means a reader should not assume that “Nexo is available” and “every major Nexo feature is available to me” are the same statement. They are not.

Some of those limits show up at the product level. The Nexo Card is available only to citizens and residents of the EEA and the UK. Futures trading is another clear example of narrower access. Nexo states that Crypto Futures Trading is unavailable in the U.S., Canada, Australia, the UK, and some EEA countries. Even certain loan or earn products carry regional restrictions. For example, Nexo’s loan FAQ says USDT loans are unavailable for residents of EEA countries, and its Fixed-term Savings article notes that earning interest and creating new fixed terms with several assets, including USDT and PAXG, is unavailable for EEA residents.

What this really means is that regulation and compliance are not just some accept all cookies or notes here; they shape the user experience directly. Two people can read the same Nexo review and end up looking at meaningfully different platforms based on where they live. That is one of the most practical things readers should know before they ever compare rates or perks.

Trust Considerations Readers Should Actually Care About

When people ask whether Nexo is safe, they often mean “can I trust it enough to park money there?” That is not just a custody question. It is also a transparency question. While you are on this topic, be sure to scan through the safest and most trusted crypto exchanges researched by experts at The Coin Bureau.

What can the user independently observe, and what do they simply have to accept as company-managed process?

With Nexo, a lot rests on the company's systems:

- How collateral is handled,

- How product availability is enforced,

- How internal risk is managed,

- And how terms change across assets, tiers, and regions.

That does not make Nexo suspect. It makes it centralized in the way readers should care about. If you are comfortable with a platform model where trust is based on operations, partner infrastructure, and compliance controls, Nexo can make sense. If you want something you can verify end-to-end on-chain without leaning on corporate execution, this will always feel like a compromise.

That is the right way to frame the trust question. Not as a dramatic yes-or-no verdict, but as a clear statement of what kind of trust the platform requires from you.

Nexo’s Core Products Explained

Nexo gives users five main things to do with their assets: earn on them, borrow against them, spend through the Nexo Card, trade or swap them, and take on extra risk through products built for more active users.

The strength of the platform is that these pieces sit inside one account and feed into one another. The weakness is that the same setup can make it easy for newer users to drift from simple tools into more complex ones without fully noticing the jump in risk.

So this section is not about listing features for the sake of it. It is about showing what each product actually does, where it helps, and where the fine print starts to matter.

Earn Products

Nexo's Earn Products, Flexible and Fixed Term. Image via Nexo

Nexo's Earn Products, Flexible and Fixed Term. Image via NexoNexo’s earn products start with two familiar buckets: one is Flexible Savings, and the other one is Fixed-term Savings.

Flexible Savings is the liquid option. You keep your assets available and earn daily interest, which suits users who want yield without locking themselves into a term. Fixed-term Savings is the commit-and-earn version. You lock supported assets for a set period, and Nexo offers a higher rate in return, and that structure is not unusual.

The top-end numbers are not automatic. Nexo states that the highest rates depend on factors such as your Loyalty Tier, whether you choose payouts in NEXO Tokens, and whether you use a fixed term instead of a flexible balance.

That means the headline earnings need to be read with both eyes open. A user on a lower loyalty tier with standard payouts may end up far below the number that first caught their attention. This is one of Nexo’s recurring patterns: the base product is simple, but the best version of it often depends on choices that increase platform commitment or NEXO token exposure.

Crypto-Backed Borrowing

Borrowing is still one of Nexo’s core products, and it remains one of the cleanest reasons to use the platform. The basic idea is simple: instead of selling crypto, you use it as collateral and borrow against it. That lets you access liquidity without giving up market exposure. For users sitting on appreciated assets, that can be attractive for tax, timing, or portfolio reasons.

The product runs on Loan-to-Value rules. Nexo assigns borrowing power to eligible assets, and the amount you can borrow depends on the value and type of collateral in your account. The platform also offers different borrowing paths, including low-cost credit lines and a separate zero-interest credit product tied to specific conditions. That sounds appealing, but the keyword is conditions. Rates and eligibility depend on things like your Loyalty Tier, your collateral mix, and the LTV you maintain.

Here’s how the borrowing flow works in practice:

- Deposit eligible collateral into your Nexo account.

- Open a credit line and choose the loan amount and currency.

- Keep your Loan-to-Value within the required range.

- Repay on your own schedule, either partially or in full, using supported fiatx, stablecoins, or crypto.

There is one nuance worth flagging here because it gets missed in lighter reviews. Early repayment is not always as simple as “pay back whenever you want with no consequence.” Nexo’s loan FAQ notes that additional interest generated by making an early repayment is added to the outstanding loan balance, and the loan terms can vary depending on the product used. That is exactly the kind of detail that separates a polished headline from the real borrowing cost.

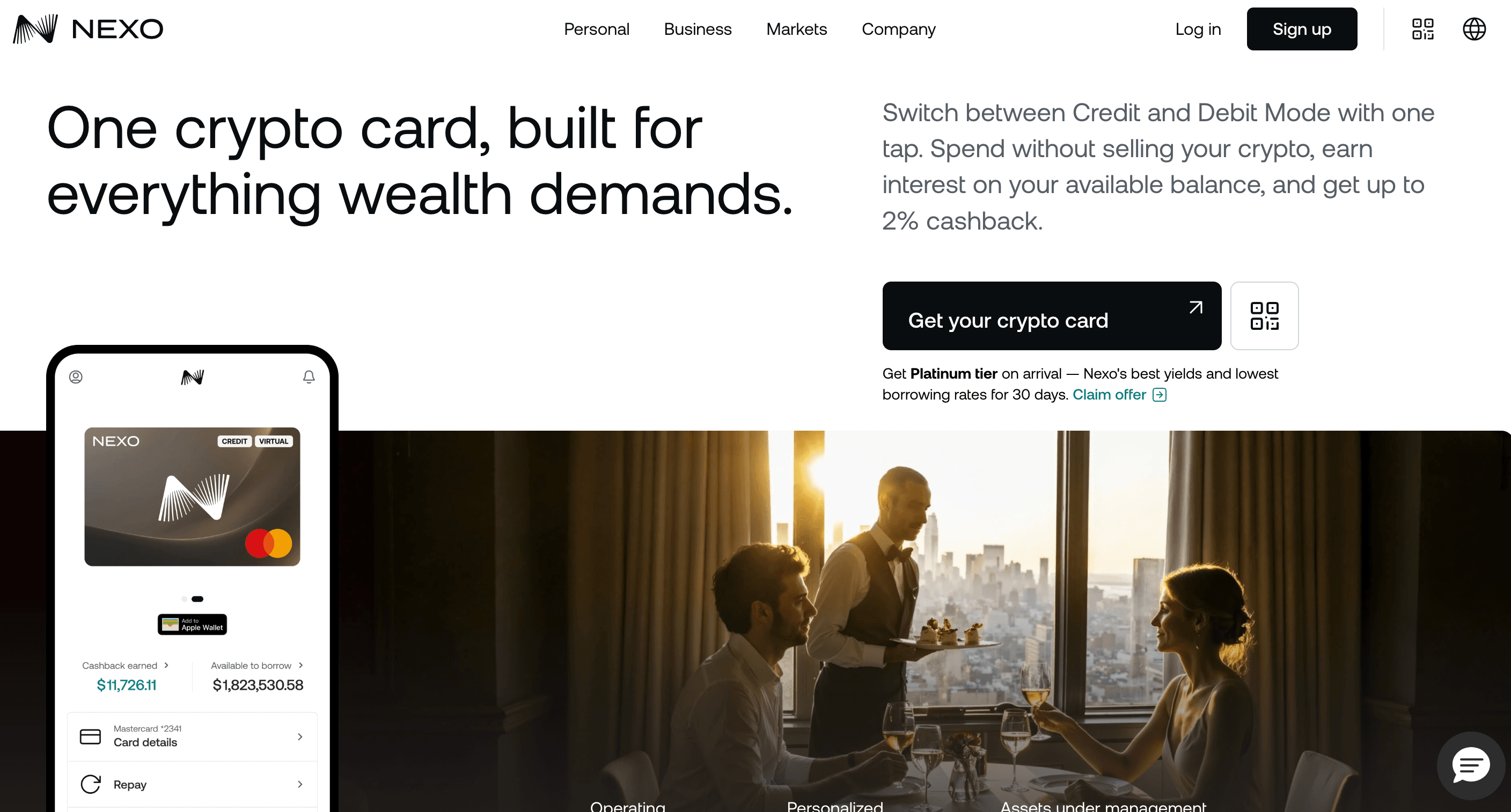

Nexo Card

Borrow Spend and Earn with The Nexo Card. Image via Nexo

Borrow Spend and Earn with The Nexo Card. Image via NexoThe Nexo Card is one of the platform’s best hooks because it ties spending directly into the rest of the account. Nexo describes it as a dual-mode card, which is the right phrase to focus on.

In Debit Mode, you spend selected assets held in your Savings Wallet, including FIATx assets, stablecoins, and cryptocurrencies. In Credit Mode, purchases are linked to your crypto-backed credit line, which means you spend against collateral rather than selling assets on the spot.

That split changes how the card feels in use. Debit Mode is more direct. It behaves like spending from balances you already hold. Credit Mode is more tied to Nexo’s core identity because it turns your portfolio into spending power without requiring a sale. For users who want to keep exposure while unlocking liquidity, that is a clever piece of product design. For users who do not want borrowing woven into day-to-day spending, it may feel like a feature they will barely touch.

Cashback is part of the pitch, but again, the better terms sit higher up the loyalty ladder. Nexo states that Credit Mode purchases can earn between 0.5% and 2% crypto cashback depending on the Loyalty Tier, and separate card support material notes that cashback applies to eligible Credit Mode purchases rather than to everything across both modes. That is useful, though it is also another example of the platform rewarding users who lean deeper into its loyalty system.

And the other caveat, of course, is geography. The Nexo Card is not a universal feature. As covered earlier, it is limited to eligible users in select European markets, so it should be treated as a meaningful perk only if your region actually supports it.

Trading, Swaps, and Recurring Buys

Nexo’s exchange layer is built for users who want convenience more than a trader-terminal experience. The platform’s exchange services include regular swaps at the current price, limit or trigger-price swaps, recurring buys, and larger OTC swaps on select pairs. Nexo also frames this around smart execution and integrated access from the same account, which fits the platform’s all-in-one identity.

This is a useful setup for three types of users. First, people who want to rebalance or swap without moving funds off-platform. Second, users who prefer a recurring buy plan over manual entries. Third, users who want a target price or trigger-based setup rather than chasing the market live. In plain terms, it gives casual and mid-level users enough trading flexibility without forcing them into a more complex interface than they need.

A simple way to think about the exchange side is this:

- Swap now if you want immediate conversion at the current price.

- Use a target or trigger price if you want execution only after the market reaches your chosen level.

- Set recurring buys if you want automated accumulation over time.

- Use OTC swaps if you are moving a very large size on supported pairs.

The real limitation is that convenience trading still has friction. Smart routing does not mean perfect pricing, and it does not remove spread or execution cost. That money-math part belongs in the fees section, but it is worth keeping in mind even here because Nexo’s trading tools are built for ease first, not for squeezing every last basis point out of execution.

Futures and Higher-Risk Products

This is the point where the platform shifts from useful to potentially dangerous, depending on the user. Nexo offers perpetual futures trading, where users can take leveraged positions and then pay or receive periodic funding depending on the contract. That is standard territory for derivatives, but it is not a casual add-on. Once leverage enters the picture, the product stops being a convenience feature and starts becoming a risk amplifier.

Nexo also offers Nexo Booster and Dual Investment, and both need to be framed carefully. Booster lets users enhance exposure using their existing crypto holdings rather than fresh capital. Nexo says it can be used to buy between 1.5x and 3x more of a chosen asset by financing the rest through the platform. That may sound efficient, but it is still leverage in nicer clothes. If the trade moves the wrong way, the downside grows too.

Dual Investment is a different kind of advanced product. Nexo describes it as a way to buy or sell a chosen crypto asset at a predetermined price at a specific future point. That makes it closer to a structured yield-and-execution product than a beginner savings tool. It can appeal to users with a clear market view and comfort with conditional outcomes. It is a poor fit for anyone who still needs simple, transparent mechanics.

Nexo Fees, Rates, and Hidden Friction Points

Where Nexo’s Real Costs Appear Beyond Headline Rates

Where Nexo’s Real Costs Appear Beyond Headline RatesThe cost of using Nexo depends on four moving parts at once: the asset you hold, the product you use, the Loyalty Tier you qualify for, and whether the headline term comes with conditions attached. That is why a casual skim can leave readers with a much cheaper picture than the one they would face in practice.

The pattern repeats across the platform. The top earning rates usually require Platinum status and, in some cases, payouts in NEXO Tokens or a fixed-term lock. The lowest borrowing rates apply only to Gold or Platinum users who also meet low Loan-to-Value conditions. Even perks like free withdrawals and card cashback are tier-shaped rather than flat benefits.

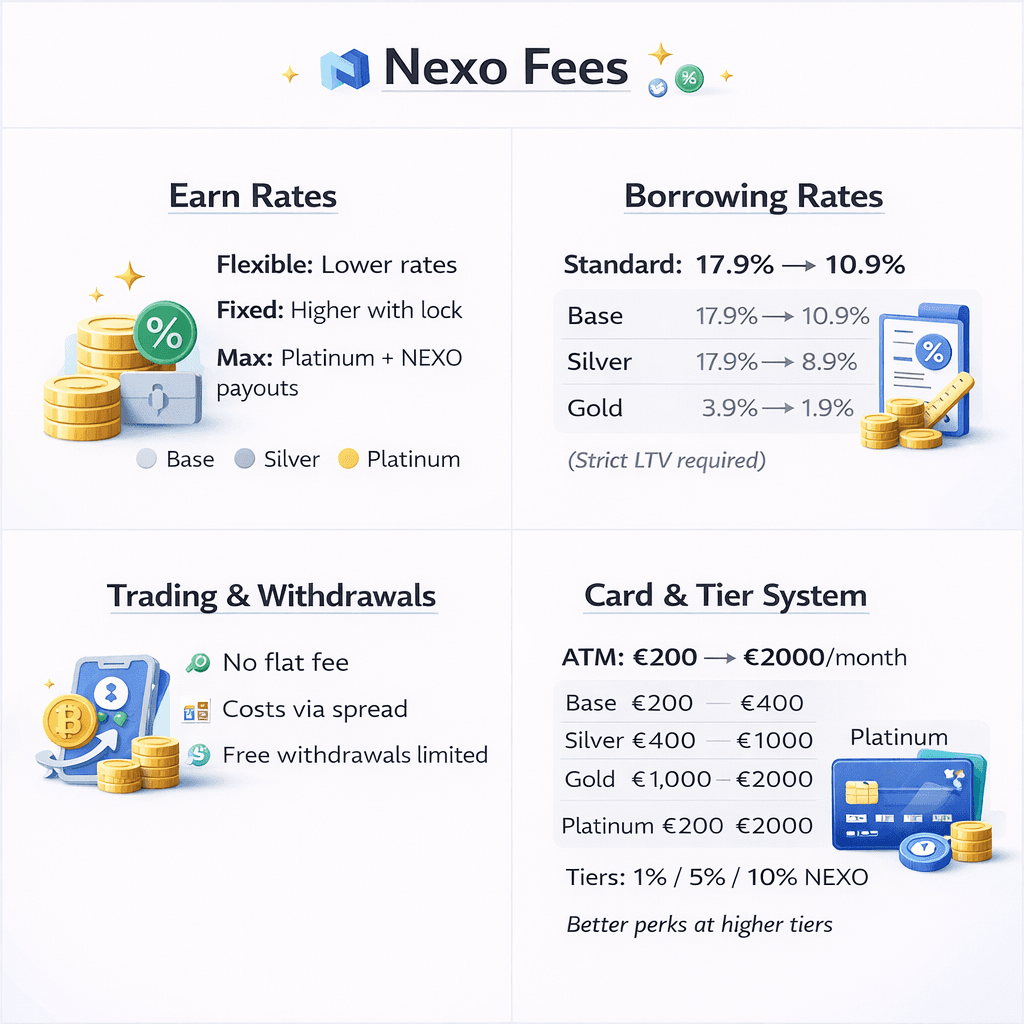

Earn Rates

Nexo’s earn rates are conditional by design. The company says the final rate depends on the asset, whether you use Flexible Savings or Fixed-term Savings, your Loyalty Tier, and sometimes whether you choose to receive payouts in NEXO Tokens. Its Flexible Savings and Fixed-term Savings articles both state that the highest interest rates require Platinum status, which means NEXO Tokens must account for at least 10% of your portfolio balance.

It's important to note that “up to” rates are not the same thing as the base experience. A user keeping assets in Flexible Savings on a lower tier may earn materially less than the top number shown in marketing. A user willing to lock funds in Fixed-term Savings and accept NEXO-linked conditions may get much closer to the headline rate. The platform is not hiding that distinction, but it does mean readers should treat headline annual yields as conditional pricing rather than default pricing.

The easiest way to think about the earn side is this:

- Flexible Savings gives daily interest with liquidity.

- Fixed-term Savings can push the rate higher, but only with a lock-up.

- Platinum status is required for the highest published rates.

- Payout choice matters when Nexo offers a rate lift for rewards taken in NEXO Tokens.

Borrowing Costs

Borrowing costs on Nexo are split into two lanes. The standard Credit Line rates shown in Nexo’s loan FAQ go from 17.9% at Base, to 15.9% at Silver, 13.9% at Gold, and 10.9% at Platinum. Nexo also offers Low-Cost Credit Lines for Gold and Platinum users, with rates as low as 3.9% for Gold and 1.9% for Platinum, but only if the user stays within the required maximum Loan-to-Value.

That distinction is important. A reader sees “as low as 1.9%” and assumes that is the normal borrowing cost. It is not. That number applies only under tighter conditions. If you miss the loyalty threshold or borrow above the required LTV band, your rate moves up fast.

There is also an early repayment catch. Nexo’s loan FAQ says that additional interest generated by making an early repayment is added to the outstanding loan balance, and its Low-Cost Credit Lines example shows that repaying before the end of the relevant period can still trigger extra interest for the remaining days in that 45-day window. That is not unusual in credit products, but it is exactly the kind of detail that users miss when they assume “I can repay anytime” means “I pay only for the days I used.”

To summarize, the total borrowing costs on Nexo are:

- Standard Credit Line rates are tier-based and can run from 17.9% down to 10.9%.

- Low-Cost Credit Lines can fall to 3.9% or 1.9%, but only with Gold or Platinum status and stricter LTV limits.

- Early repayment can still leave you with extra interest, depending on the product terms.

Trading, Swap, and Withdrawal Costs

On the exchange side, Nexo’s own support material makes one thing clear, even when it does not package it dramatically: trading convenience is not the same thing as frictionless execution.

Nexo Exchange Services uses smart routing and supports instant swaps, recurring buys, trigger-price swaps, and other order types. It also offers up to 0.5% crypto cashback for certain swap operations to eligible Silver, Gold, and Platinum users who maintain at least a $5,000 portfolio balance.

Users still face spread and network friction even when no simple flat “swap fee” is front and center. Smart routing can improve execution, but it does not erase effective spread. The platform may feel smooth, yet the cost is still there in the price you get, the network you withdraw on, and the number of free withdrawals your tier actually unlocks.

Withdrawals are a good example. Nexo’s support pages state that Platinum Loyalty Tier users get one additional free withdrawal per calendar month on supported blockchain networks or via bank transfer, and that the Loyalty Program benefits, including the free monthly withdrawal for Platinum users, require at least a $5,000 portfolio balance. So “free withdrawals” exist, but they are limited, tier-based, and conditional. Outside those allowances, network fees still apply.

The Nexo Card has its own fee-style friction, too. Nexo says free ATM withdrawal allowances depend on Loyalty Tier: Base gets €200 / £180 per month, Silver €400/£360, Gold €1,000/£900, and Platinum €2,000/£1,800. Once you move past those limits, the economics change. In other words, the card’s convenience also comes with a tier ladder attached.

READ: Best Crypto Exchanges With The Lowest Fees

The Real Cost of the Loyalty Model

This is the part most readers should pay attention to. Nexo’s Loyalty Program is not a side perk. It is the pricing system underneath the platform. The four tiers are Base, Silver, Gold, and Platinum, and they depend on how much of your portfolio is held in NEXO Tokens. Base requires no NEXO exposure. Silver starts at 1%, Gold at 5%, and Platinum at 10%.

That structure can be valuable. Higher tiers unlock better earn rates, lower borrowing costs, extra withdrawal perks, and stronger cashback on the Nexo Card. But the benefit is not free. To reach those terms, you take on NEXO token exposure and the opportunity cost that comes with it. You are not only comparing Nexo’s rates to another platform’s rates. You are also deciding whether holding a chunk of your portfolio in NEXO is a trade you want to make in the first place.

That is why the loyalty model should be read as both a benefit engine and a hidden cost center. If you already wanted NEXO exposure, the platform gets more attractive. If you did not, then part of Nexo’s best pricing is effectively asking you to buy into an extra bet just to unlock it. That is not a deal-breaker. It is simply the real shape of the offer.

User Experience and App Quality

A platform like Nexo lives or dies on the boring stuff. If the setup is clunky, verification drags, or the app makes simple actions feel buried, the rest of the product stack starts to lose its charm. This matters even more here because Nexo is trying to do several jobs at once. It is not only an earn app or only a borrowing interface. It wants users to move between savings, credit, card use, and trading without friction. So the user experience has to carry more weight than it would on a single-purpose platform.

The good news is that Nexo seems to understand that. Its onboarding flow is built to get users verified and into the platform quickly, and both its mobile app and web platform are positioned as full-service interfaces rather than stripped-down companions. The fine print, as usual, sits in what happens after signup: KYC requirements, extra checks in some jurisdictions, and the difference between standard support and higher-touch client care.

Onboarding and Verification

Nexo requires identity verification before users can access its products. Its support documentation says the verification process is fully automated and usually takes just a few minutes, though additional Know Your Customer checks can apply in some cases. That gives the onboarding flow a fairly clean start for standard users, but it also tells you right away that Nexo is not trying to be a loose sign-up-and-explore app. Access to the useful parts of the platform begins after verification, not before.

That process can get more layered depending on the region and account type. Nexo’s help pages say products are only accessible after identity verification through its provider, Sumsub, and separate documentation shows that users may also face Source of Wealth, Source of Funds, or Source of Crypto checks. In the UK, there is another layer again: Nexo says residents must complete an Investor Categorization and an Appropriateness Assessment to keep access to products in line with FCA rules. So while the base onboarding can be quick, the real experience depends on who you are, where you live, and what level of access you want.

Simple steps for onboarding are:

- Create the account.

- Complete identity verification.

- Pass any extra checks tied to jurisdiction or account profile.

- Fund the account and unlock product access.

Mobile and Web Experience

Nexo presents both the mobile app and the web platform as core interfaces, not as one main product and one backup. Its support content repeatedly refers users to either the app or the web platform for major actions, including verification steps and account updates. This means feature parity is part of the intended experience. Users are not being nudged into a situation where the mobile app is only for checking balances while the real account management happens elsewhere.

In practice, that fits the way Nexo is built. A platform that combines portfolio tracking, savings, credit, card activity, and trading needs a dashboard that keeps these functions close together. Nexo’s own positioning leans on that bundled experience. The homepage highlights funding the account, using the card, earning, borrowing, and loyalty benefits within one environment, which matches the idea of a portfolio-centered dashboard rather than a feature-first layout.

That said, there is a quiet trade-off here. When a platform tries to do many things in one place, the interface can feel efficient to experienced users and slightly overpacked to newer ones. Nexo avoids some of that by grouping products around the account rather than making each tool feel like a separate app.

Still, a beginner who only came for crypto savings may find the presence of credit, futures, and token-tier mechanics more than they bargained for. That is not bad design. It is just the natural result of a platform trying to be a financial control panel instead of a single-use product.

Support and Client Care

Support is one area where Nexo pushes hard on service quality. Its help center mentions the Client Care team is available 24/7, and the main site echoes that by marketing 24/7 personalized client care. For a platform dealing with money movement, verification delays, card use, and credit products, round-the-clock support is more than a nice extra. It is part of the product.

There is also a visible split between standard support and premium handling. Nexo Private is marketed to individual clients and family offices with $100,000 in digital assets, and the company says this tier includes tailored onboarding, a dedicated relationship manager, high-limit OTC trading, bespoke credit, and other exclusive benefits. That means client care is not entirely flat across the platform. Everyone gets access to support, but higher-value users get a more hands-on version of it.

That setup makes sense for the kind of business Nexo wants to run. A casual retail user may only need fast answers and a clean help center. A larger client moving size, using bespoke credit, or relying on OTC execution needs a different level of care. So the support picture here is fairly clear: Nexo offers 24/7 assistance across the platform, but its best service lane is reserved for users who meet the Private threshold.

Loyalty Program and the Role of the NEXO Token

Better Perks Come With A Token Driven Commitment at Nexo. Image via Nexo

Better Perks Come With A Token Driven Commitment at Nexo. Image via NexoThe Loyalty Program is not a little extra tucked onto the side of the app. It affects earn rates, borrowing costs, card cashback, and withdrawal perks, which means it changes the real value of the platform from top to bottom. A user can look at Nexo and see strong pricing, but a lot of that pricing only comes into focus once the NEXO token enters the picture.

On Nexo, the NEXO token is part loyalty key, part pricing lever, and part extra portfolio bet. For some users, that trade works well. For others, it is where the platform starts to lose appeal.

How the Loyalty Tiers Work

Nexo divides the program into four tiers: Base, Silver, Gold, and Platinum. The thresholds are set by how much of your portfolio is held in NEXO Tokens relative to the rest of your balance. Base requires no NEXO allocation. Silver starts at at least 1%, Gold at at least 5%, and Platinum at at least 10%. In plain English, the more NEXO you hold as a share of your account, the better your tier.

That structure is easy to understand on paper, but it has a bigger effect than people expect. The tier is not just a badge inside the app. It shapes what version of Nexo you actually get. A Base-tier user and a Platinum-tier user are using the same platform, but they are not getting the same pricing, the same withdrawal perks, or the same cashback profile.

A clean way to explain the tiers would be:

- Base: no NEXO token requirement

- Silver: at least 1% of the portfolio in NEXO Tokens

- Gold: at least 5% in NEXO Tokens

- Platinum: at least 10% in NEXO Tokens

What You Actually Gain at Higher Tiers

The benefits at higher tiers are real. Nexo’s own materials tie the best earn rates to Platinum status, which means users need at least 10% of their portfolio in NEXO Tokens to reach the highest published rates on Flexible Savings and Fixed-term Savings. That is one of the clearest examples of how the token changes the economics of the platform.

Borrowing is another major example. Standard credit-line rates improve as you move up the ladder, and low-cost credit lines with the sharpest published rates are reserved for Gold and Platinum users who also stay within the required Loan-to-Value conditions. So the token does not just improve passive perks. It also lowers the cost of using one of Nexo’s oldest core products.

Card and withdrawal perks also improve with tier. Credit Mode cashback on the Nexo Card rises with Loyalty status, and eligible users can receive higher crypto cashback at upper tiers. Free ATM withdrawal allowances also step up by tier, from €200 / £180 per month at Base to €2,000 / £1,800 at Platinum. On top of that, Platinum users with at least a $5,000 portfolio balance can make one free monthly withdrawal for either FIATx or crypto.

So the practical benefits of climbing tiers look like this:

- Better earn rates

- Lower borrowing costs

- Stronger cashback on the eligible card and exchange activity

- More generous withdrawal-related perks

The Trade-Off of Holding NEXO

The benefit side is clear. The harder part is saying what it costs. To get those better terms, users must keep a slice of their portfolio in NEXO tokens. That means the loyalty model is asking for token exposure in exchange for improved pricing. The benefit is meaningful, but it is not free.

That creates two layers of risk. First, there is a concentration risk. If you would not otherwise choose to hold NEXO, the platform is nudging you into taking a position just to unlock better conditions. Second, there is an opportunity cost. Money allocated to NEXO cannot be allocated elsewhere, so the user has to decide whether the extra yield, lower APR, or higher cashback is worth that trade. This is not a flaw unique to Nexo, but it is one of the main reasons the platform works far better for some users than for others. The more comfortable you are with the token, the better the platform tends to look.

Nexo vs Other Platforms

Nexo can be compared with almost every large crypto platform, but that usually leads to a bloated section full of weak one-liners. The cleaner way is to keep the comparison tied to the actual user decision. Is Nexo better if you want one place to earn, borrow, card spending, and trading? Often yes. Is it cleaner or simpler than every competitor? Not at all. Its edge comes from how many products sit together in one account. Its weak spot is that the best version of the platform often depends on the NEXO token, regional eligibility, and comfort with centralized custody.

Nexo vs Binance/Coinbase/Crypto.com

Against Binance, Nexo feels more like a managed wealth app and less like a giant exchange that happens to have earn and loan products attached. Binance clearly offers Simple Earn and flexible crypto loans, and it also warns that products may not be available in every region. But Binance’s identity is still exchange-first. Nexo, by contrast, presents borrowing, savings, card use, and loyalty benefits as one connected loop, which makes the experience feel more packaged and less modular.

Against Coinbase, the comparison is more mixed. Coinbase has a cleaner mainstream brand and now offers borrowing against crypto, staking-based earning, and a membership layer through Coinbase One. But the product shape is different. Coinbase leans more toward brokerage, staking, and membership benefits, while Nexo leans harder into collateral-backed borrowing, tier-based pricing, and a tighter earn-borrow-card bundle. If you want a platform that feels more like a crypto finance account than a retail brokerage, Nexo has a sharper identity. If you want a simpler mainstream entry point with less token-linked complexity, Coinbase may feel easier to live with.

Crypto.com is probably the closest comparison in spirit because it also tries to keep spending, rewards, and multiple crypto functions under one roof. Its Visa Card pushes hard on cashback and tiered benefits, with fees and limits that vary by jurisdiction and card tier. That overlap makes the comparison more direct. The difference is that Nexo’s identity still revolves more clearly around crypto-backed borrowing and savings, while Crypto.com spreads its value proposition across app usage, card rewards, exchange activity, and its broader consumer ecosystem. In simple terms, Crypto.com feels more lifestyle-led. Nexo feels more balance-sheet-led.

So if you strip the branding away, the comparison looks like this:

- Binance is stronger if exchange depth is the main priority.

- Coinbase is cleaner for users who want a more mainstream, brokerage-style path.

- Crypto.com competes most closely on card-and-app convenience.

- Nexo stands out when borrowing, earning, card use, and loyalty-based pricing need to live inside one account.

Nexo vs Crypto Lending-Focused Alternatives

Compared with platforms built more narrowly around crypto lending, Nexo’s biggest win is convenience through range. It does not stop at crypto-backed loans. It wraps those loans into a larger account structure that also includes savings, exchange functions, and card-based spending. For users who actually want that connected experience, Nexo is more complete than a plain lending app.

The flip side is that specialization has its own appeal. A more lending-focused platform can feel easier to understand because the product logic stays tighter. Nexo’s model asks users to think about Loyalty Tiers, NEXO token exposure, card modes, earn options, and sometimes advanced products as well. That gives it more ways to be useful, but it also gives it more moving parts than a user may want if the only goal is to borrow against crypto as simply as possible.

That is the real trade-off in this comparison. Nexo wins on integrated experience. It loses on purity. A user who wants one controlled environment for several financial actions may see that as a strength. A user who wants the shortest path from collateral to cash may not.

Where Nexo Stands Out

Nexo stands out because very few platforms package earn + borrow + card + trading + private-client services as tightly as it does. Its homepage and product pages present those features as one system, not as disconnected extras. That is the heart of the platform. You deposit assets once, then decide whether they should earn, support borrowing, fund card activity, or move through trading tools.

That does not mean Nexo is automatically the best choice. It means the platform has a very specific strength. If you want a centralized custody environment with several crypto-finance tools integrated, Nexo has a stronger case than many rivals. If you want universal access, no-token dependency, or the cleanest possible product scope, one of the alternatives may fit better.

Final Verdict: Is Nexo Worth Using in 2026?

Nexo is worth using if you want a centralized crypto lending platform that keeps earning, crypto borrowing, trading, and card spending under one roof. That is still the clearest reason to choose it. Nexo’s platform is built around convenience, and its strongest feature is how these products connect from one account instead of feeling like a pile of separate tools.

That said, the platform is not an automatic yes. Its best version still depends on the Loyalty Program, which means the NEXO token is not optional in any real economic sense if you want the sharpest rates and perks. The company’s offers show that material says the NEXO token sits at the core of the Loyalty Program, and Platinum status requires at least 10% of the portfolio in NEXO Tokens. That makes the value proposition stronger for users who are comfortable with token exposure and weaker for users who want clean pricing without an extra portfolio dependency.

For a user who wants one account to do many jobs, yes. And for a user who wants self-custody, no token dependency, and the fewest moving parts possible, probably not.